Commentary

Drilling into European oil & gas

January 12, 2023

Anyone who’s kept an eye on the markets is aware that the energy sector had a blowout performance in 2022. It started with the war between Russia and Ukraine in February that spiked oil and gas prices, the discussion then shifted to European LNG supply for the following winter, including which countries would be able to absorb Russia’s excess oil supply. Clearly, the energy resurgence in 2022 was a European-driven one.

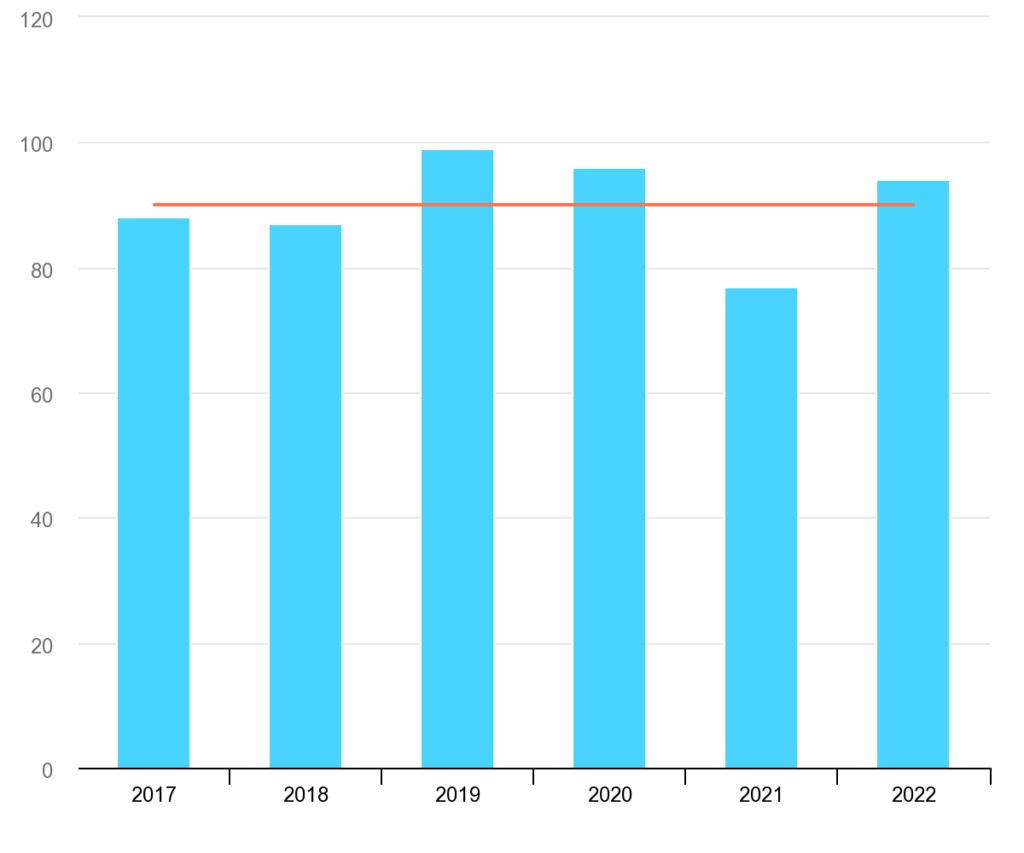

With that in mind, what is the situation going into 2023? It appears that the worst-case scenario for this European winter has been avoided. Natural gas prices are now back at the pre-Ukraine invasion level, EU gas storage is sitting a comfortable 5% above its five-year trend, and winter weather has been lenient so far.

European Union gas storage levels, 2017 – November 2022

Governments are now focusing on planning for next winter, and the data points are more mixed. In 2022, Europe benefitted strongly from having Russian LNG flow for most of the summer and from lower LNG demand from China. Both things are unlikely to repeat in 2023. Indeed, a worst-case scenario, where Russian pipelines stop flowing completely for 2023, would represent a gap of nearly 50% of total gas storage requirements for the winter of 2023/24. And there are not many options for Europe to fill this gap elsewhere. Indeed, China’s 2023 LNG imports are expected to reach 2021 levels, which would capture over 85% of the estimated increase in 2023 LNG global supply, with much of that increase already contracted by China.

The market however does not appear to be discounting this. December 2023 futures contract for LNG is sitting around €70 per MWh, three times pre-2021 levels but well below the peak of €345 seen in August. There are certainly some indicators that support this optimism. Between August and November 2022, EU natural gas consumption dropped 20.1%, well above the government self-imposed target of 15% for the period between August 2022 and March 2023. Finland reduced its consumption by as much as 52%. Many countries capped the price for consumers and businesses. These lower prices should help alleviate the size of deficits generated from these programs, allowing those countries to face next winter with a healthier balance sheet. Furthermore, the weather for the rest of the winter will be a key driver of the requirements for next year, as estimates for gas storage levels at the end of the heating season vary between 5 and 35% of full capacity. Clearly it is too soon to predict a worst-case scenario, and Global Alpha does not expect a worst-case scenario to materialize. But the pain is likely to be felt more than markets currently discount.

At Global Alpha we have historically underweighted energy in our portfolios, not because of any macro views, but instead because the team consistently found better stock picking opportunities elsewhere. Indeed, pure oil and gas stocks are often at odds with Global Alpha’s investment philosophy: the quality of their balance sheet is volatile, they depend on macroeconomic factors to outperform, and as such tend to be more momentum based.

So how does Global Alpha get its energy exposure? An example of a name we have owned for many years is Schoeller Bleckmann Oilfield Equipment AG (SBO VIE). The company is the global market leader for high precision drilling components, providing nonmagnetic drill string components to directional drilling oil field service companies. Headquartered in Austria, more than 80% of its business is done in the U.S. and Europe, with high profile clients such as Schlumberger, Halliburton, and Baker Hughes.

With a healthy balance sheet and key market positioning backed by proprietary technologies, Schoeller-Bleckmann provides an attractive exposure to energy prices without being dependent on a few oil and gas projects. Indeed, its stock price has benefited from the pick-up in rig counts since mid-2021, with the firm boasting a book-to-bill ratio consistently above 1x, while at the same time showing its ability to pass on cost inflation to clients. There have also been discussions of green energy diversification, though the strategy remains unclear for now.

SWOT analysis

Strengths

- +50% market share in most of its products

- Strong balance sheet supported by low net debt

Weaknesses

- Dependence on the big three oil services companies

Opportunities

- Increased geographical diversification

- Opportunistic M&A

Threats

- Technological competition in their key plug market

- Loss of market share in the U.S.

Schoeller-Bleckmann is a perfect example of the type of quality names Global Alpha is looking for in its portfolios: a niche, market leader with global exposure and a clean balance sheet that allows for sustained growth.