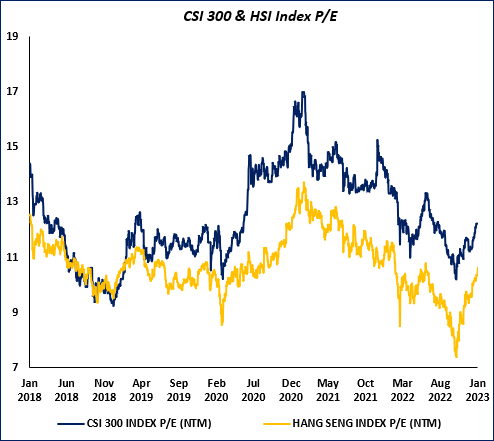

Gulf equity markets rolled over in the fourth quarter and materially underperformed emerging markets. This marks a stark but predictable (as we wrote in our last Q3 letter) reversal in fortunes, with tailwinds of the outperformance in the last 18 months turning to headwinds. We summarize the key drivers of the weakness in Gulf equity markets in the fourth quarter below:

Lower oil price and a different transmission mechanism – Gulf economies are highly levered to oil prices. While a Brent oil price of $80 is healthy for most Gulf economies, surpluses will naturally be lower as prices come down and barrels produced and sold remain static. Moreover, and focusing on Saudi Arabia, the share of oil revenue proceeds going into the banking system has come down considerably as the government allocates an increasing proportion of oil revenue to its sovereign wealth fund where the trickle down to economic activity is seemingly less visible (for now).

Higher interest rates – Gulf currencies are effectively pegged to the U.S. dollar and central banks have had to adjust to the Fed’s four rate hikes of 75 basis points in 2022. The relative attraction of owning equities with three months SIBOR rates reported at 5.59% is understandably low. Gulf investors have more alternatives than ever before to invest their money, with the recent Al Rajhi Bank Sukuk proving to be particularly popular among retail investors. Higher rates are also putting pressure on the net interest margins of banks as they compete to attract deposits. This phenomenon is likely to be especially acute in Saudi Arabia, where the liquidity environment has tightened n the fourth quarter of 2022. Saudi banks represent ~23% of most MENA indices and so the aforementioned profit margin compression has a material impact on the market’s aggregate EPS growth expectations for 2023. In other Gulf markets like the UAE and Qatar, state and quasi-state companies have been pre-paying debt at a rapid pace to avoid higher interest rates, leading to anemic corporate loan growth and further pressure on profitability.

Weaker USD – Gulf equities are effectively US dollar-denominated assets and are generally more attractive for global investors when the U.S. dollar is appreciating. This relationship has become stronger since Gulf equity markets became a large component of emerging market indices. Active Global Emerging Market (GEM) investors are not incremental buyers of Gulf equities in a weaker USD environment and their current underweight exposure to the region suggests they prefer to own assets denominated in non-pegged currencies.

Valuations – Gulf equity markets are coming off excessive valuation levels that reflected over-optimism on the degree and timing of the impact of reform program announcements, and robust foreign inflows following the deletion of Russia from the emerging market universe in March 2022, which we discussed in our second quarter letter.

A wall of offerings – 2022 was a record year for capital raised through primary and secondary transactions and the number of deals closed in the region with 47 listings raising a total of $26.5 billion. A large number of deals and the prospect of share sales by government and quasi-government shareholders took the air out of the market. We think it is wise for government funds to reduce or float their stakes in strategically listed companies given the level of ownership is far above what is required to retain control. However, this is likely to weigh on the share prices of many of the large-cap companies in the market where those entities are key shareholders. On a lighter note, overexcited bankers salivating at the prospect of fees from investment banking deals continue to be a reliable indicator of negative future market performance.

As for the strategy, we managed – to a large extent— to avoid the significant drawdown that the region experienced in the fourth quarter. Three factors helped us achieve this outperformance:

Sticking to high conviction portfolio companies like Saudi Dairy and Food Co. (SADAFCO) where management execution and weaker competition are leading to significant earnings growth that the market has been behind on for a few quarters now.

Adding to high conviction portfolio conviction companies that we believe are likely to experience an improvement in an operating environment like the National Company for Learning & Education (NCLE). NCLE’s eleven K-12 schools are experiencing a noticeable increase in utilization as students return to in-person learning in Saudi Arabia and management’s various initiatives (which focus primarily on quality of education in existing schools, M&A and greenfield for new schools) bear fruit.

Reducing or exiting portfolio companies we believe have reached valuation levels that are no longer attractive. A good example of this is Saudi Tadawul Group (STG), the country’s stock exchange which we exited at nearly peak average daily traded value. Over 60% of STG’s revenue is linked to traded values on the stock exchange and our exit decision reflected an understanding that traded values cannot just continue to go up, a view that the market is only getting around now as traded values have dropped 50% y-o-y in recent months.

We continue to see a strong opportunity for the strategy as the market begins to reflect the “bad news” in the price of assets we like, and as investments in companies we’ve made in the last 6-12 months or earlier continue to deliver.

While we acknowledge that the environment has been favourable for the strategy, and decisions we made have on the whole been good ones, we are not resting on our laurels and will endeavor to continue delivering differentiated value-added returns for our clients looking to access the growing investable opportunity in the MENA region.

Vergent Asset Management LLP

As this quarter marks the final letter for the year 2022, we thought it will be helpful to reflect on the key events that shaped the performance of the strategy in the year.

Economics

The war in Ukraine, and the resulting spillover into higher energy and food prices, exposed structural imbalances that resulted in spiraling inflation and currency depreciation across most markets. Our focus on African and Asian companies and through-the-cycle underwriting process put us at a disadvantage as food and oil prices experienced sharp and sustained inflation.

The consumer basket in our markets is over-indexed to those basic commodities, and the fiscal and balance of payment dynamics of most developing countries (where we exclusively invest) are inversely correlated to commodity prices. In response, we identified the most vulnerable countries in the portfolio and made decisions to exit two companies in Egypt and one in Pakistan, and selectively reduce exposure to Kenya. We highlighted in our third quarter letter that our portfolio companies experience a net positive carry in a higher rate environment, as most hold more cash than debt. Where there is debt, it is mostly in local currency or otherwise matched with foreign currency income. Of the top ten companies in the portfolio, seven enjoy a net cash position.

Despite active portfolio management that reduced exposure to the most vulnerable countries, and defensive portfolio attributes, returns were still dramatically overwhelmed by the impact of currency moves. Around 47% of the strategy’s returns in the year can be explained by foreign currency depreciation against the US dollar, with notable currency devaluation in the Egyptian pound, Pakistani rupee, and the Ghanaian cedi.

Politics

The strategy experienced volatility from the onset as political unrest in Kazakhstan in January led to a meaningful drawdown in the share price of Kaspi.Kz, a fairly sizable position for the strategy. Since then, Kazakhstan’s political outlook has materially improved. On the domestic front, Kassym-Jomart Tokayev secured a second term in a snap election held in November, cementing his position against political rivals from the previous regime. On the foreign policy front, Tokayev seems to have navigated the Russian-Ukraine crisis as well as anyone expected, striking a neutral position that preserved his country’s deep-rooted ties to Russia, while constructively increasing diplomatic and economic engagement with the West and China. Our team visited Kazakhstan in May where we visited with Kaspi.Kz management, their main bank competitor, and other relevant stakeholders. Our visit was instrumental in reinforcing our constructive thesis on Kaspi.Kz, which we then translated into opportunistic buying of the shares at what we deemed to be deeply discounted valuations. Fortunately, this helped turn a 38% drop in the share price of Kaspi.KZ in 2022 to a flat performance contribution to the strategy in the same year.

Kenya and the Philippines, key markets for the strategy, also held presidential elections this year. In Kenya, a peaceful election held in September saw power seamlessly transition to President-elect William Ruto, a testament to the democratic process, and the strength of institutions, in the East African country. President Ruto’s policy priority to reduce debt and improve Kenya’s fiscal position is negative for near-term growth but essential for sustainable long-term economic growth. His pro-trade stance, and his visit to neighbouring Addis Ababa for the national launch of Safaricom’s operations in Ethiopia, signal a commitment to preserving and expanding Kenya’s role as an economic and diplomatic hub for the region. It is worth noting that this political progress has not had the hoped-for effect on Kenyan equities, where weak macroeconomic conditions and dwindling stock market liquidity are prevailing. In the Philippines, Ferdinand Marcos Jr., the namesake son of the late dictator, was elected President in an election held in May. While many Filipinos are skeptical of Macros Jr.’s abilities and are understandably wary of his family’s history, his appointment of well-regarded technocrats in key economic roles has been a bright spot. While policy under Marcos, just like his predecessor Rodrigo Duterte, is probably going to remain uninspiring, it is fair to conclude that a Marcos presidency is, on the whole, positive for Filipino equities.

Earnings vs. Valuations

Reassuringly, earnings from key portfolio companies remained resilient in the year, reflecting elements of quality we expected when we underwrote those investments. We calculate that the strategy’s top 10 holdings experienced an average of 17% growth in revenue and earnings per share in the first nine months of 2022, compared to the same period in 2021. Even when there were setbacks in earnings, operating metrics were exceptionally strong for certain portfolio companies. Take Safaricom as an example; while EBITDA and EBIT were down 4% and 11% year-on-year respectively, the company’s M-Pesa ecosystem continued to grow from strength to strength, producing 32% growth in transaction volumes and signalling continued adoption by Kenyan consumers of M-Pesa in their daily lives. More importantly, most portfolio companies are guiding for a better year ahead, which bodes well for earnings visibility in the next six to twelve months.

With earnings being resilient and share prices coming down, multiples on the portfolio have come down to the level of ~10x Price to Cash Flow (P/CF). This multiple should be put in the context of a Return on Equity (ROE) that is well above 30% for the overall portfolio. This undervaluation has not gone unnoticed by the insiders of some portfolio companies; insider buying in the shares of Integrated Diagnostics Holdings in the third quarter, share buybacks from Kaspi.Kz in the last nine months, and a tender offer from Diageo for the minorities in East African Breweries in October (at a 30% premium) are all evidence of value recognition by the ultimate insiders.

Outlook

We are optimistic on the strategy’s performance in 2023. We highlight four key factors we believe can shape the outlook for performance:

With the U.S. dollar appreciation cycle potentially peaking, the pressure on currencies in most of our markets has abated, and we think it is unlikely we will see any meaningful negative contributions from currencies like the Indonesian rupiah, the Filipino peso, and the Moroccan dirham. In vulnerable countries like Egypt and Pakistan – where the strategy does not have much exposure— central banks are doing away with unhealthy currency management and letting market forces be the primary driver of the FX rate. This is a positive move that will open investment opportunities for the strategy in 2023.

Inflationary pressures have abated on food and certain commodities. While prices remain high by historical standards, we believe consumers, businesses, and governments have taken the brunt of the pain in 2022. The normalization of supply chains from the reopening of China should result in lower supply-side inflation and release the pressure on some of our companies to hold larger than normal inventory levels, which will increase cash conversion.

The domestic political picture is fairly stable after a busy 2022. This bodes well for policy visibility in 2023 and beyond. We expect policy to generally be pro-business and positive for equities. Looking forward, we expect the Indonesian general elections in February 2024 to be a positive catalyst for the strategy’s Indonesian portfolio in the second half of 2023.

The starting point for valuations is considerably low relative to the earnings power and visibility of portfolio companies. In other words, there is a fair amount of downside that is priced in. We are seeing insiders act on those valuation levels and consider that to be a strong bullish signal.

Finally, it is worth reminding readers that our objective is to deliver differentiated returns that can be attributed to the skill of investing (alpha) over the directionality of markets (beta). We believe there is an abundant alpha opportunity in frontier and emerging markets, which we choose to express through a concentrated but geographically diverse portfolio of companies with idiosyncratic earnings drivers and share price catalysts. Naturally, this should result in significant deviations from global and emerging market indices in certain periods, but hopefully provide a superior risk-adjusted return profile to investors in the long term.

Vergent Asset Management LLP

Since the World Bank’s International Finance Corporation first coined the term emerging markets in 1981, the characteristics and composition of the markets have evolved significantly. Past concerns regarding the resilience of emerging markets during a crisis led some investors to struggle with the merits of including a direct allocation. However, with the rise of China and its leadership of global economic growth, investors are increasingly considering a dedicated allocation to emerging markets. This article reviews the evolution and the general case for investing in emerging markets.

The key attributes supporting the case for global emerging markets have been evident for some time and include:

Greater growth

In the latest Global Economic Prospects report by The World Bank Group, emerging and developing economies are forecast to grow more than double that of advanced economies in 2023 and 2024.

Drivers of Innovation

Many emerging markets companies have become leaders of innovation in important sectors such as internet-related technologies, electric vehicle battery manufacturing, and computer chip manufacturing.

Household names

Many emerging market companies are household names such as Samsung and Hyundai, while other less recognized companies have acquired well-known global brands.

Rising returns

As emerging markets shift from manufacturing to more value-added industries, there is an expectation for the ability to generate superior returns to rise.

Alpha opportunities

Emerging markets are less researched by the analyst community compared with large cap developed equity markets, which creates opportunities for excess returns from independent research by active managers.

Background

Emerging markets are characterized as countries with growing economies and a growing middle-class population. Many of these markets continue to have high rates of poverty, and often they are still experiencing significant social and political change. But despite such headwinds, the growth prospects of emerging markets can provide a strong base for investors to be rewarded.

The market capitalization of emerging markets was US$ 90,456 billion as of December 31, 2022, representing a little over 11% of the world equity capitalization. Yet many institutional investors have no direct exposure to emerging markets. Instead, investors often rely on their international and global equity managers to selectively invest in emerging markets, which can result in the allocation falling well short of its representation of the world equity market capitalization. With emerging markets representing the highest growth area of global stock markets, there is a case for investors to benefit from at least a market representation.

The MSCI Emerging Markets Index is comprised of over 1,300 stocks in 24 countries. Countries are normally grouped into three regions, Emerging Markets Asia, Emerging Markets Latin America and Emerging Markets Europe, Middle East and Africa, with the Asian region representing almost 80% of the market index.

Evolution

For the longest time emerging markets were considered similar to the Canadian equity market, with a heavy bias to commodities. Today, the combined weighting in energy and materials for emerging markets is less than 13% of the index market capitalization, compared to 30% of the Canadian equity market. Instead, emerging markets have evolved to offer opportunities different to the Canadian equity market. For example, emerging markets have experienced a steady rise in the information technology and health care sector allocations, which together represent over 20% of the market index (Figure 1). Not only that, but within the information technology sector there has also been a radical change in its composition with large and successful companies, such as Alibaba and Tencent making up an important component of the sector.

Figure 1: Index Sector Allocations

Global Industry Classification (GIC) Sector

MSCI Emerging Markets (%)

S&P/TSX Composite (%)

Energy

5.0

18.1

Materials

7.6

12.0

Industrials

19.4

13.3

Consumer Discretionary

12.5

3.7

Consumer Staples

4.7

4.2

Health Care

10.7

0.4

Financials

14.3

30.8

Information Technology

10.8

5.7

Communication Services

2.8

4.9

Utilities

3.2

4.4

Real Estate

8.9

2.6

Source: Thomson Reuters Datastream. Data as of December 31, 2022. Due to rounding, column percentages may not total 100%.

The financial sector represents around 14% of the index and offers a further differentiation versus developed markets, where the loan-to-deposit ratios in emerging market companies are generally lower.

However, the biggest change to the emerging market index has been with respect to country allocation, and the growing dominance of China in the index. It was not long ago that large cap China A shares represented less than 1% of the MSCI Emerging Markets Index. At the end of 2022, China accounted for over 32% of the index (Figure 2).

Figure 2: Region and Larger Country Allocations

Region and Country

MSCI Emerging Markets Index (%)

Emerging Markets Asia

78.3

China

32.3

India

14.4

Taiwan

13.8

Republic of Korea

11.3

Emerging Markets Europe, Middle East & Africa

13.2

Saudi Arabia

4.1

United Arab Emirates

1.4

Qatar

1.0

Kuwait

0.9

South Africa

3.7

Emerging Markets Latin America

8.5

Brazil

5.3

Mexico

2.3

Understanding the Risks

It is important to appreciate risks associated with investing in emerging markets. While active managers can mitigate some of these risks through research and careful selection of individual stocks, investors should recognize the following.

Political and social risk: Political and social changes taking place in emerging market countries can lead to uncertainty due to corruption, regulations not always being rigorously enforced, or governments exhibiting an unwanted influence. The uncertainty contributes to market volatility. For example, Beijing’s actions to limit the influence of Hong Kong-listed technology companies, combined with a real estate sector crisis and the zero-COVID policies that witnessed longer strict pandemic controls relative to most other governments, contributed to a tough and volatile 2021-2022 for emerging market equities.

Information and liquidity risk: Although the quality of data has vastly improved, obtaining good, complete and timely information can still be challenging in emerging markets. Currency controls remaining in a small number of markets also may create liquidity concerns.

Recognizing the potential benefits

While the countries are classified as emerging, nearly all the companies in the MSCI Emerging Markets Index have a market capitalization greater than US$ 1 billion, which compares to 209 Canadian companies with a market value above US$ 1 billion. Increasingly, emerging market companies are becoming household names, whether on their own merits, or through acquisition of global branded companies, such as Samsung, Hyundai Motor and the Indian conglomerate, Tata, which is the owner of brands such as Jaguar, Land Rover and Tetley Tea.

The key benefits offered by emerging markets include:

Growth opportunity: The drivers of growth are wide ranging and include demographics, economic development, technology, innovation, infrastructure development, and capital market developments. While global growth is expected to moderate from 2021 levels, emerging and developing countries are expected to account for a significant component of world gross domestic product (GDP). The World Bank forecasts emerging and developing markets to grow at an average annual rate of 3.4% in 2023 and 4.1% in 2024, compared to expansion of only 0.5% and 1.6%, respectively for advanced (developed) economies.1 A significant proportion of developed market company earnings are also linked to emerging market growth, further underlining its importance.

Drivers of innovation: Innovation in emerging markets has contributed to its evolution, as well as China becoming an important component of the market. Innovation has allowed several emerging market countries to leapfrog the developed world in terms of business models. For example, while many farmers in India have no access to computers and landlines, smart phones have created an information and business environment that allows buyers and sellers to interact, as well as enabling e-payments.

Rerating opportunity: Ordinarily, high-growth assets are priced at a premium. Emerging market stocks have traditionally traded at a discount to developed world valuations, but the economic fundamentals for emerging markets as a whole have improved.

Improving returns: Many emerging market companies are shifting away from manufacturing for Western companies and looking to develop their own identity and growth success. To achieve this they are tapping into higher value-added areas using brands and technology, recognizing that branded firms with loyal followers can achieve more than double the margins of non-brand firms. Return on invested capital (ROIC) should rise for emerging market companies as they develop world-class brands.

Growing universe of opportunities: The growth of China in the emerging market index has also witnessed a growth in the universe of investment opportunities. Today, there are as many China A shares that meet the typical liquidity and market capitalization criteria as there are in the United States (US) equity market. Similarly, the number of opportunities for emerging markets excluding China is not too different from the number of opportunities for the global developed market, excluding the US.

Style offset opportunity: The growing opportunity set has witnessed a growth in systematic (quantitative) fund offerings, where the managers use technology to gain a breadth of understanding on a large universe of companies, compared to the depth of understanding associated with fundamental managers focused on selecting a smaller portfolio of companies. As for other equity markets, investors who can accommodate multiple managers in an asset class can benefit from the complementary approaches of systematic and fundamental styles.

Alpha opportunity: The external analyst community generally undertakes less research of emerging market companies compared to global developed companies. Active managers have been able to benefit from independent research with over 86% of managers in the emerging market equity universe outperforming the MSCI Emerging Market Index over the 10 years ended December 31, 2021 (based on the eVestment database).

Environmental, Social and Governance Considerations (ESG)

Despite the political and social challenges associated with emerging market countries, companies are increasingly recognizing the importance of ESG considerations. Helping this cause has been the expansion of ESG coverage of emerging markets companies by third-party providers. The importance of each ESG component varies from one country, industry or company to another. However, like the developed world, corporate governance tends to be the most material issue, followed by the steps being taken to manage the environmental impact of companies in the emerging markets.

The Case for Emerging Markets

Many investors are underweight emerging markets relative to its representation in world equity markets, yet global growth is expected to be led by emerging and other developing markets.

Canadian investors have historically shied away from emerging markets, partly due to the historical commodity bias. Today, emerging markets offer a very different opportunity set due to innovation that has seen a transformation in the type of companies and opportunities, including a significant growth in the information technology sector.

As emerging market companies shift from manufacturing to higher value-added interests using brands and technology, the number of emerging market household names will increase, and help to grow margins and ultimately the return potential from emerging markets.

1 Source: World Bank Global Economic Prospects, January 2023

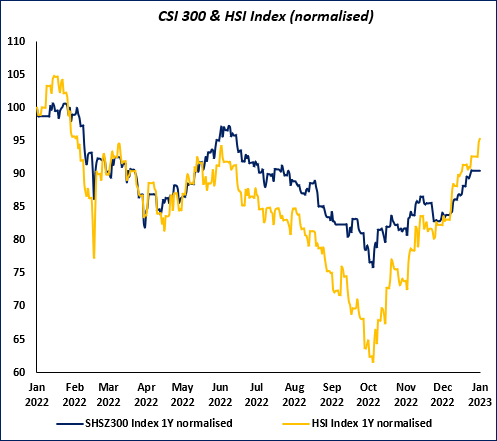

Sparked by China’s rapid reopening, emerging market equities staged a sharp recovery from the lows of last October with the MSCI EM Index up nearly 23% (in USD terms) since the end of October, led by China which is up 54%.

The Institute of International Finance reported that January flows into EM equities and debt were the second strongest on record — the strongest being post-lifting of lockdowns in late 2020.

Buoyant sentiment in India is set to be tested with the collapse of Adani Group’s follow on public offer (FPO) after a report by U.S. short seller Hindenburg Research accusing the conglomerate of “brazen stock manipulation and accounting fraud over decades.”

The news drowned out positive press on the Indian federal government’s budget, with tax relief for India’s middle class expected to boost consumption, alongside a drive to slash regulations and improve the ease of doing business across the country.

The Bank of Korea is raising rates aggressively, pressuring equities and property markets. There is also added pressure from the downswing in the semiconductor cycle hitting DRAM giants Samsung Electronics and SK Hynix. Macro in Korea is a drag but longer-term the U.S. Inflation Reduction Act will provide a meaningful tailwind for the economy, particularly for those companies operating in the EV and renewables supply chains. There is also added pressure from the downswing in the semiconductor cycle hitting DRAM giants Samsung Electronics and SK Hynix but both are guiding for a H2 recovery and a strong 2024 outlook.

Similarly in Taiwan, there are signs that the semi cycle is bottoming. TSMC reported results with management expecting a H2 rebound in demand driven by increasing demand from data centres/hyperscale servers/AI applications, along with greater penetration in EVs.

Money numbers in a number of major EM countries outside of Asia are picking up. In Brazil, inflation has fallen and there should soon be some scope for central bank easing (after pausing hikes at 13.75% last September). However, we are cautious of the impact of weakening commodities and political risk. In mid-January President Luiz Inácio Lula da Silva gave a TV interview where he stated that the formal independence of the central bank (enshrined into law in 2021) was “nonsense”. This was likely retaliation to comments from central bank governor Robert Neto that a spending boom by Lula’s government posed an inflationary risk. Tempering this political risk is a divided and right-leaning Brazilian Congress which should force Lula to moderate.

Can the EM bounce be sustained?

While 2022 was a painful year for EM equities (following a disappointing decade), the outlook is increasingly positive as a number of headwinds abate.

Inflation – superior monetary policy and greater fiscal discipline in EM is the foundation for falling inflation, which opens the door to policy easing as the Federal Reserve approaches the end of its tightening cycle.

Economic growth – global economic weakness remains a headwind. However, EM is forecast to outpace growth in the West, led by China reopening. GDP in EM economies is expected to grow by 3 ppts more than the rate in the U.S. over 2023 and 2024, versus even in 2022 (Morgan Stanley).

Earnings momentum – the relative profitability gap between EM and DM is set to close, as companies benefit from the end of an extended deleveraging cycle and the recent period of global monetary tightening. On the other hand, profit margins in the U.S. sit at all-time record levels, a significant hurdle in the face of higher labour and other input costs.

Valuations – attractive relative to history and to DM, with positioning in EM equities among global allocators currently at depressed levels (Copley Fund Research).

Dollar – the dollar slumping into year-end 2022 was a tailwind for EM, but we are sceptical that the slide will continue at this rate in the near-term. Positive catalysts for a weaker dollar will include inflation continuing to fall, thereby increasing the odds of a Fed pause, and improving EM growth relative to DM.

China rally – is it time for a breather?

Chinese equities have run up a long away over the last two months following Xi’s pivot to more pragmatic policy on COVID, property, tech regulation and foreign relations. Abandoned by foreign investors earlier in 2022, H-shares rallied hard while A-shares lagged.

Source: Bloomberg

Source: Bloomberg

Valuations across Chinese equities remain supportive, although our view is that the “reopening trade” is now largely reflected in valuations. From here we see support for continued outperformance by Chinese stocks on an economic growth and corporate earnings recovery, along with positive money numbers. Consumption data over the Chinese New Year period were generally better than expected, with retail sales, passenger trip volumes, domestic tourism, box offices sales and restaurant sales up significantly and in many cases exceeding pre-COVID numbers.

That said, we do not expect a repeat of the reopening boom (in markets and the economy) that took place in the West when lockdowns ended. In the U.S. and Europe there were huge excess money balances and pent-up demand, to a far greater degree than what we currently see in China. On the latter, China was not subject to countrywide lockdowns, instead, harsh restrictions were applied on a regional basis to stamp out spikes in case numbers. In addition, the PBoC appears to be far less expansionary than Western counterparts, wary of setting off a wave of inflation as a result of pumping too much monetary stimulus. The weakness in the Chinese property market will also weigh on recovery as a negative wealth effect will hit consumer sentiment. Markets will be watching for additional government support to quash lingering structural risks in the sector.

Adani to test “India Inc.”

U.S. short-seller Hindenburg released a damaging short report claiming that giant Indian conglomerate Adani Group (with businesses across healthcare, energy, food and infrastructure) has been involved in “brazen stock manipulation and accounting fraud over decades.” The report argues that the group operated an elaborate web of shell companies across numerous tax havens, which were used as instruments to inflate Adani stock which in turn would be pledged as collateral for loans and thus placed the group on a “precarious financial footing”.

Hindenburg alleges the fraud enabled founder and Chairman Gautam Adani – who rose to prominence in Gujarat at the same time Prime Minister Narendra Modi was the state’s chief minister – to amass a personal fortune of over US$120 billion. Much of the wealth is owing to an 800% appreciation in stock prices across the Group’s seven listed companies over the last three years.

The release of the short report and subsequent collapse of Adani Enterprises’ stock has scuttled plans to raise over US$2 billion via a follow on public offer. Attention now turns to the Modi government and the Securities and Exchange Board of India to investigate any wrongdoing. Given both the close ties between Modi and Gautam Adani, and a business that lies at the heart of India’s economy, this will be an important test of institutional credibility.

We have written to clients extensively on India’s steady progress up the development ladder and opportunity this presents to investors. How authorities deal with this situation will provide an indicator of this progress – they will have to catch up to the local investment industry which has viewed Adani with suspicion for years. Hindenburg notes in its report that despite the Adani Group’s size, there is a dearth of reputable sell-side coverage on the companies, and no local active funds willing to hold these stocks in any meaningful size. We will watch on with interest to see how the government and the SEBI engage with the accusations – and hope for a tough response should they hold water.

We are sanguine with respect to the potential for systemic fallout in India should Adani collapse. India’s state banks would bear the brunt, however, it is likely that the viability of projects tied to Adani loans should cushion the blow. Indeed, should the market narrative around India’s rise lose some sheen in the coming months, we may see some emerging opportunities to add exposure to some names that we believe are long-term winners.

The story of Little Red Riding Hood is perhaps the most implausible of all the pre-17th century European folk tales. Just how – a rational mind may presume – does a little girl mistake a ravenous wolf for her own grandmother? Like many such fables, the beauty in the Grimm brothers’ work lies in the extraction of rich metaphorical meaning from absurdity. Timeless lessons that have a habit, for those paying attention, of occasionally popping up in unexpected areas of our lives like a sagacious Whac-a-Mole. While Little Red Riding Hood is hardly a fulsome guide to investing, her ill-fated demise due to a case of mis-identity may still offer a lesson for investors.

As fundamental equity investors, it is critical that our decisions stem from objective reasoning. Spending each day striving to achieve the clarity of thought that comes with truly unbiased, matter-of-fact thinking, honed by experience and devoid of prejudice, is key not only to our long-term success but also in upholding the fiduciary duty to our clients.

It is why our philosophy centres on two simple ideas: invest with conviction and act with humility. The guiding principles behind each of our decisions that help us uncover wolves concealed amongst even our highest conviction ideas, and prevents deception from the seemingly familiar becoming – ironically – all too familiar.

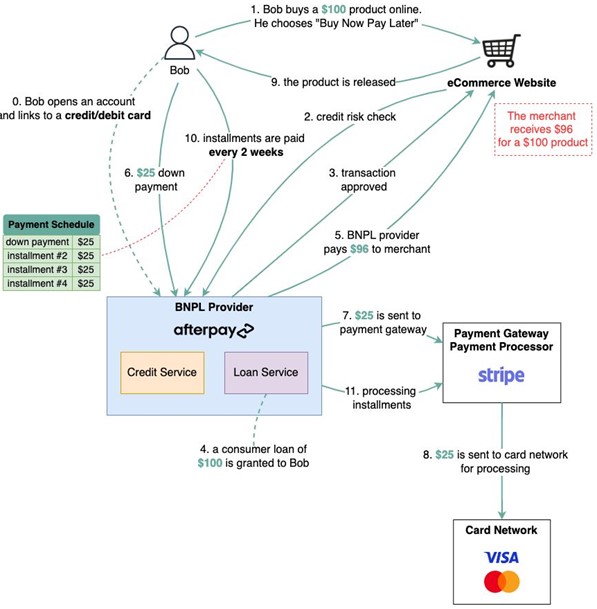

Buy-now-pay-later (BNPL) is one concept that we believe can be particularly deceptive. To the unassuming consumer, BNPL is wonderfully ingenious. Credit risk for your transaction is shouldered by the merchant from whom you purchase. It looks, smells and tastes like free money. Only alas! On closer inspection we find that BNPL is in fact just a craftily marketed, dolled up version of the same age-old credit process. Soft pastel colours and smiling millennials may have replaced images of burly debt collectors demanding pounds of flesh, but the core underlying credit agreement between consumer and lender remains unchanged. Missed payments will still result in the same letters in the post, demanding the same penalizing late fees. And opening them will still provoke the same sense of incredulity as you jump up and shout, “Oh my! I didn’t realise what big teeth you have!”

Contextualising BNPL as a branch of consumer credit is a prerequisite to appreciating its value. The ongoing arms race between technology giants Grab, GoTo and Sea Ltd over Southeast Asia’s 120 million Indonesian labour force participants who do not own a credit card is the archetype of the modern fintech battle that we see across many of our markets. There are millions of people in Egypt, Vietnam, Philippines, Nigeria, Kenya and Bangladesh without access to consumer credit, but poor pre-existing infrastructure makes it difficult for highly focused credit products such as BNPL to gain traction.[1] Here, the spoils of war will not be won on credit alone. Funding gaps of such depth and complexity must instead be addressed by a broad arsenal of fintech services including digital banking, cashless payments, credit reporting and cross-border transactions.

Alibaba’s Alipay is arguably the best example to-date, and its success in China has created a blueprint for many platform businesses within our markets. A collection of fledgling financial Megazords working to refine the configuration of their autonomous product constructs. For many it remains a work-in-progress. However, there are exceptional cases that indicate some may have found a winning formula.

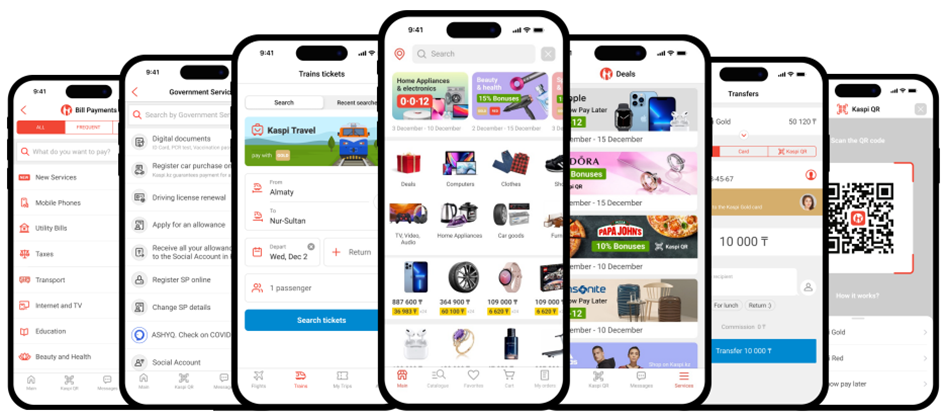

Nestled away in a market of just 19 million people, Kaspi.kz has built a formidable application that boasts a user base comprising over 95% of the adult population of Kazakhstan. What originated as a humble Tier 2 bank has emerged over the last decade as the largest payment network, e-commerce platform and consumer finance business in the country.[2] Today, Kaspi.kz processes more transactions in Kazakhstan – where over two thirds of all transactions are cashless – than Visa and MasterCard combined.[3] Online purchases through the 260,000 active merchants on the platform account for over 70% of the entire e-commerce market.[4] And in 2021 they distributed over twice the amount of consumer loans compared to the largest and most systemically important bank in the country. In short, Kaspi.kz is not just a part of the fintech revolution in Kazakhstan. It is the revolution.

Figure 2: Kaspi.kz has multiple payments, e-commerce and credit products within a single application

Source: Kaspi.kz

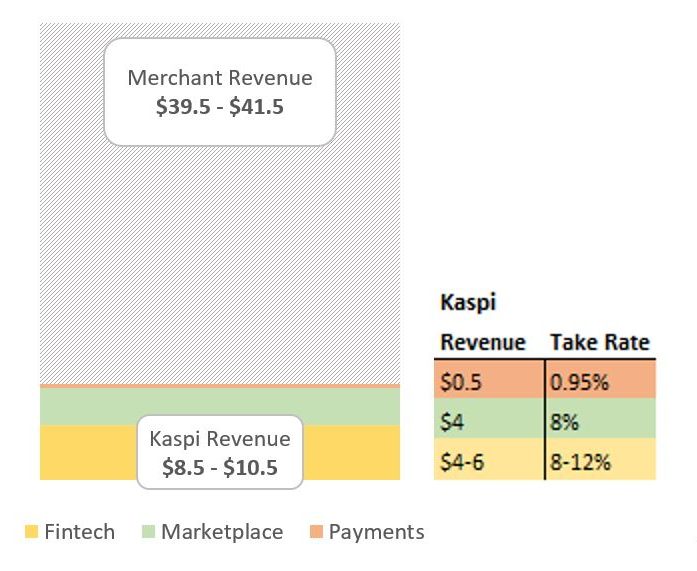

Indeed, outside of China, one would be hard pressed to find a company that has a firmer grip on the consumer spending journey than Kaspi.kz enjoys in Kazakhstan. In providing a place to purchase, a method to purchase and the means to fund that purchase, Kaspi.kz owns every commercial touchpoint of the transactions through its platform, thereby gaining access to the maximum profit pool of each consumer. Consider someone making a US$50 online purchase, funded through a three-month, 0% interest BNPL product. That single transaction has three revenue channels for Kaspi.kz, equating to between US$8.5 and US$10.5 in revenue. That is a whopping 17-21% of the overall transaction value.[5]

Figure 3: Revenue distribution for $50 e-commerce transaction funded through 3month BNPL

Sources: Kaspi.kz; Vergent Asset Management

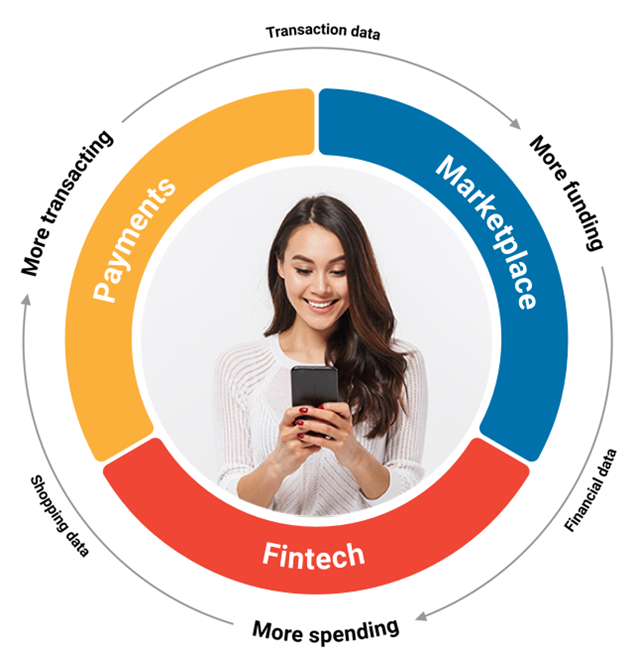

The roots of success are often multifaceted, and Kaspi.kz is no exception. No doubt there are traces of the Matthew Effect, but equally we see attempts to deploy the same payments-marketplace-consumer finance trifecta in other markets as far inferior.[6] In our view, the triumph of Kaspi.kz in Kazakhstan is not as much in the business mix as it is in how those businesses are woven together. And in this case all yarns lead back to BNPL.

Figure 4: Kaspi.kz’s three businesses benefit from a strong network effect

Source: Kaspi.kz

Contrary to the traditional BNPL model of maximising standalone yields, Kaspi.kz utilizes BNPL as the engine room to drive the average transaction value (ATV) and volume of its users high enough to maximise the revenue of the entire platform. Incremental transactions generate proprietary data points on each user that pollinate other revenue generating areas of the business, whilst simultaneously diluting cost centres such as product development, sales and marketing, and risk management. That arms Kaspi.kz with new products and data to support more informed lending decisions, and thus the cycle repeats. Such is the potency of this lending model that through 2021— a period when the three global BNPL giants collectively burnt over US$1 billion of cash— Kaspi.kz’s standalone lending business generated a return on equity of over 45%.[7]

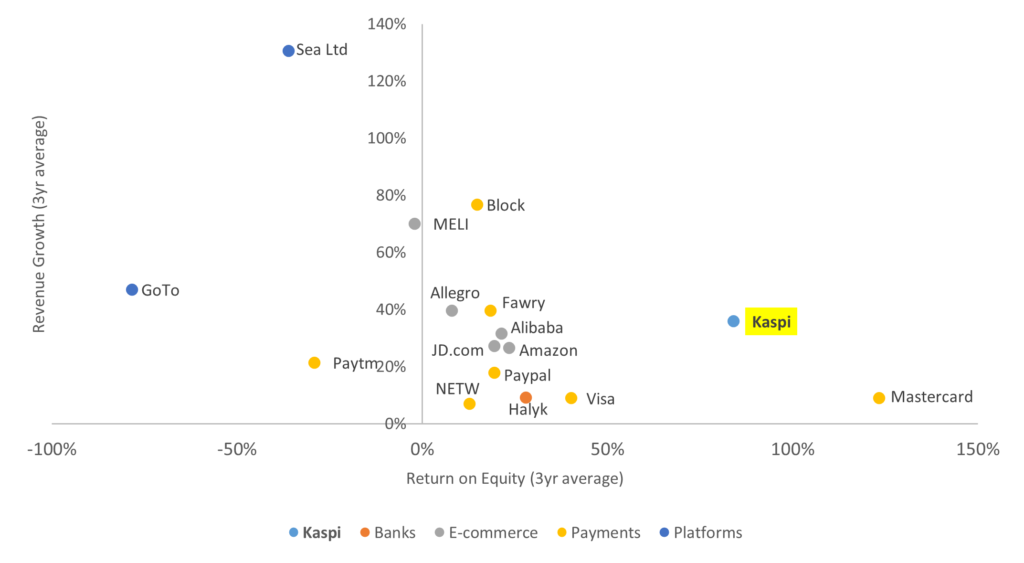

One of the most compelling upshots from this model is the impact on growth. Revenues magnified by intertwined, self-perpetuating products have a diluting effect on the cost base, sending operating leverage into overdrive. As a result, Kaspi.kz has managed to grow revenues at a 34% CAGR since 2019, despite spending on average just 4% of revenue on sales and marketing.[8] Even more astounding is that this growth was delivered at an average net margin of over 40%, for a combined growth and return profile that is best-in-class on an industry, regional and even global basis.

Figure 5: Revenue growth (three-year average) vs. return on equity (three-year average) for comparable peers

Sources: Bloomberg; Company Filings; Vergent Asset Management

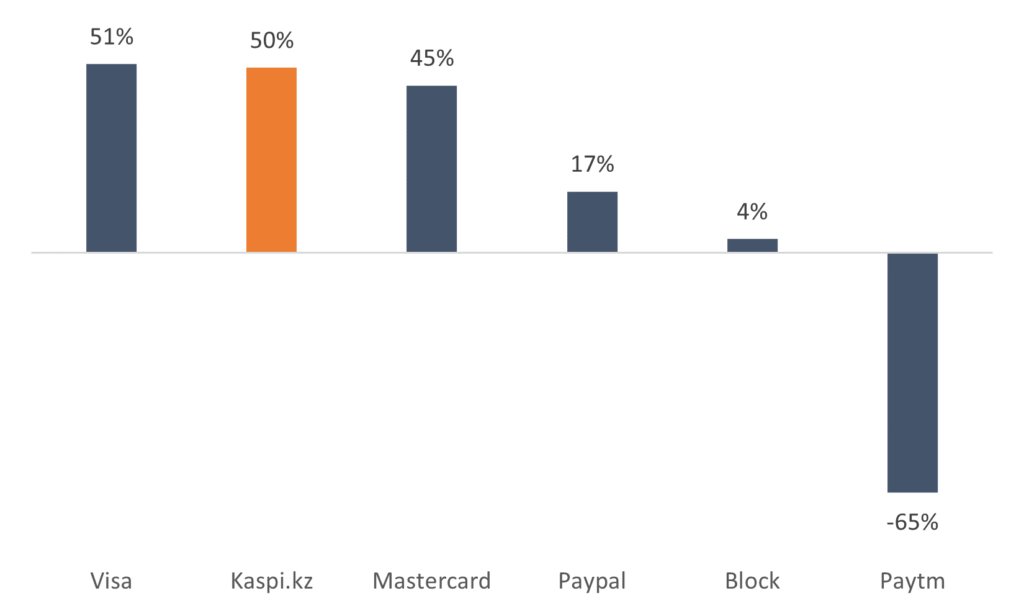

Consequently, Kaspi.kz enjoys the luxury of being able to subsidise strategic products profitably. In the marketplace business that means providing 95% of deliveries free of charge whilst still operating at over 60% net margin. Within payments, it means monetizing less than 10% of the peer-to-peer (P2P) transactions that constitute over 75% of total payments volume, thereby forgoing the lucrative interchange fee that typically represents the largest revenue line for digital banks, including Monzo and Revolut, as the cost of customer acquisition. That Kaspi.kz’s standalone payments business can still deliver net margins comparable to the largest and most successful global payments companies, despite surrendering these fees and operating in a market a fraction of the size, speaks to the harmony of its consolidated platform.

Figure 6: Net income margins of payments peers (three-year average to last reported period)

Source: Bloomberg; Kaspi.kz Data shown for Kaspi.kz is the standalone payments business

The term super-app is overused and, in our view, frequently misunderstood. Sifting through investment decks of the not-so-super, the moderately-super or even the one-day-we-are-sure-to-be-super apps that flood our markets can at times feel like dragging a philistine through a modern art exhibition. No matter how fervent the arguments may be that the blue square in front of you is a masterpiece – a unique perspective on modernism – to the untrained eye it all looks rather the same. When we suggest that Kaspi.kz is emerging as one of the few genuine super-apps it is not because the platform tells the same exhausted story of having multiple products under one roof. Strength here is not in numbers: It is in the intricate design of each product such that the sum of all products is greater than the parts.

Critically, the platform must have ‘plug and play’ compatibility with new products. Acting as a magnet for new services that yearn for an adrenaline shot of growth is vital for keeping the platform sharp, competition blunt, and deepening the competitive moat of any aspiring super-app.

Take for example, Santufei, a negligible rail and airline ticketing vendor that comprised just a handful of people and a few basic aggregator relationships when Kaspi.kz acquired it in August 2020 for a paltry US$5 million. Today, that business (rebranded ‘Kaspi Travel’) sells over 70,000 tickets per month through what is now the largest rail and ticketing platform in the country. And travel tickets are just the start. There is a not-so-distant future where we foresee an office worker in Almaty ordering a taxi after a long day, getting home to receive promotions for their favourite takeaway, placing an order and then tipping the delivery driver all through Kaspi.kz. In this world, it is 3rd party developers that must bow as Kaspi.kz ascends to the gilded heights of consolidator. The gatekeeper to an ecosystem so rich that 3rd parties are forced to cede a slice of the economics, despite assuming all the business risk.

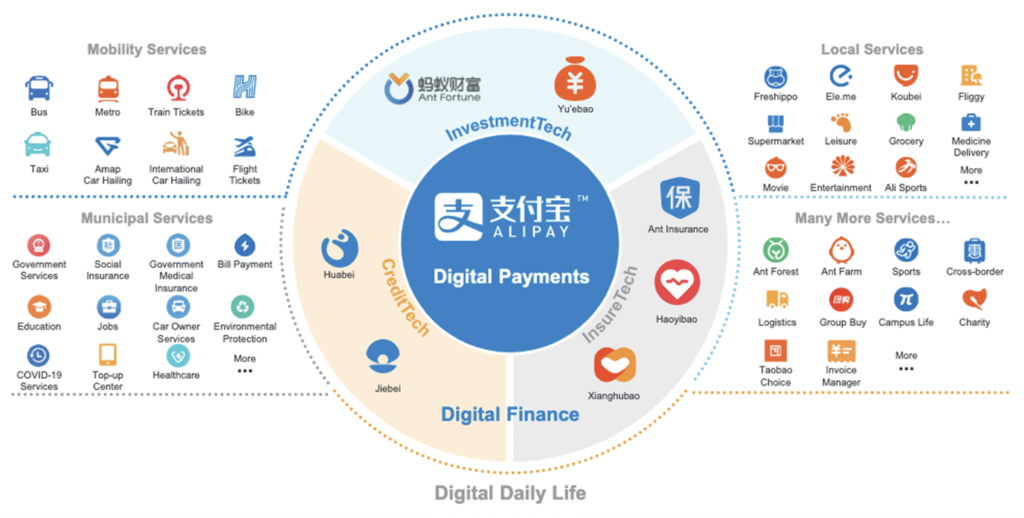

Platform compatibility is also relevant for the merchant base. Many services unbeknownst to consumers such as B2B payments, supply chain management solutions and merchant credit services offer equally attractive economic prospects, if not a means to entrench the platform deeper into the Kazakhstan economy than their consumer product counterparts. One only needs to look at the breadth of services offered through Alipay today to get a sense of how much more room there is for Kaspi.kz’s platform to grow.

Figure 7: Alipay offers insight into what the future Kaspi.kz platform may look like

Source: Alibaba; Vergent Asset Management

Although the example of Alipay offers a glimpse as to the end state for every aspiring super-app, we must remember that by no means does it reflect the sole operating model. Platforms with origins in payments will differ to those grown out of e-commerce, financial services, or one of the countless other services that can support the initial acquisition of customers. In our view, it is the understanding of this centrality that becomes essential in helping us see beyond a familiar and otherwise undifferentiated countenance.

So while Kaspi.kz will march on, continuing to forge new products against the idiosyncrasies of Kazakhstan, the near-term focus for us will remain firmly on BNPL. For today, that is the beating heart of the company’s ecosystem. The consumer credit juggernaut that in equal measures poses the greatest risks and opportunities to sustainable growth.[9] That we maintain our diligence, stay grounded in our approach and appreciate the consumer credit business for what it really is, will give us the best chance – we hope – of seeing Kaspi.kz write its own fairy tale ending.

[1] Based on ~139 million labour force and ~17 million credit cards in circulation. Sources: World Bank; Bank of Indonesia.

[2] Grossly simplified, Kaspi.kz is probably best thought of as a combination of Revolut, Paypal and Taobao. A somewhat fitting unity of East and West.

[3] Source: Analysis of the payment market in the Republic of Kazakhstan, PWC (March 2022).

[4] Source: Analysis of the retail e-commerce market in the Republic of Kazakhstan, PWC (October 2022).

[5] Moreover, this example is conservative. BNPL products that exceed three-months draw interest from the consumer and higher take rates from merchants, while certain e-commerce categories also command higher take rates.

[6] Taken from the Gospel of Matthew and popularized as the Power Law, the Matthew Effect is based on the idea that market leaders will attain a disproportionate amount of value over time. For companies with large network effects, that typically means being first to market.

[7] The three global BNPL giants referenced here are Klarna, Affirm and Afterpay, which reported US$631 million, US$431 million and US$159 million FY21 net losses respectively.

[8] Calculated as three years to June 2022.

[9] Macroeconomic risks associated with Kazakhstan are also at large, and the exclusion here for simplicity should not be confused with insignificance.

Summary

Slight down month for EM to round out the year.

The US dollar steadied against major currencies, following a sharp fall in November.

Turkey finished the year as the best performing market in EM (having been the worst in 2021), nearly doubling in USD terms.

Unsurprisingly, Russia was the worst, having been rolled out of the index in Q1.

China was the only major EM market to notch positive gains through the month as reopening moves ahead at a rapid clip.

Gulf markets struggled as a darkening global economic outlook hit energy stocks.

India had a down month following strong performance through the year. We think the long-term structural story in India is extremely compelling, but valuations look rich at this point.

Political risk in South Africa fell following president Cyril Ramaphosa’s re-election as African National Congress (ANC) party leader for a second five-year term, allowing the leader to run in the South African presidential election in 2024.

Re-election followed a tumultuous campaign, rocked by allegations that emerged in June that a large sum of foreign currency stashed inside a couch had been stolen from the president’s game farm in 2020.

A subsequent parliamentary investigation indicated that the president may be liable for misconduct, leading to an impeachment vote that was ultimately shot down by the ANC majority parliament in December.

Portfolio activity

Paring back exposure in Southeast Asia and India to add to China H-shares.

Maintaining bias to defensive sectors and quality.

Missed opportunity in Turkey?

There is currently no exposure to Turkey in the portfolio. Despite the sharp rally this year, we are wary of very poor liquidity and high macro risk. It is hard to see how the recent run is sustainable, to say the least.

Portfolio Manager Oliver Adcock visited Turkey earlier in 2022 to see whether there is a realistic chance of political change in presidential and parliamentary elections scheduled for most likely June 2023. Markets would undoubtedly cheer the election of an Erdogan alternative who would move quickly to establish a more orthodox fiscal and monetary regime.

Oliver met with pollsters, the head of one of the opposition parties, banks, corporates and a local thinktank.

Elections in 2023 look to be a close call, with the most likely outcome being that Erdogan and his AK Party lose control of parliament while retaining the presidency. We see this as a poor outcome.

One of the factors in Erdogan’s favour is that the coalition of opposition parties (the “Table of Six”) are struggling to decide on a presidential candidate, much less one that is likely to beat Erdogan to the presidency.

Erdogan does have room on the fiscal side and is likely to continue to pump the economy as much as he can into elections. This is despite headline inflation running at around 80%. Rates have recently been cut to 12%.

Cutting rates in the face of raging inflation courts serious currency risk, especially when forex reserves stand at around -$56 billion when accounting for currency swap lines (mainly with other Middle Eastern countries).

One large factor in the market rally has been driven by single stock futures, whereby the Turkish regulator has been allowing investors to reinvest gains made on trades even though they were not closed out. This has had the effect of supercharging the upswing.

Meetings with a number of banks confirm the economic situation is very volatile and fragile. The government is trying to control everything. New regulation attempts to force banks to lend at rates lower than 25%. The central bank rate is set at 12% but no one is lending there, banks are lending at 20% to SME and consumers, while deposits are 16%.

Overall, the economic backdrop is changing so rapidly that banks are reluctant to do anything, compelled to keep lending tight, and are holding weekly strategy meetings to assess key risks such as dwindling forex balance sheets.

The rally in Turkish stocks looks fragile and recent data indicates that foreign investors have been selling into it. Foreign ownership was already at historic lows and has continued to fall so it would seem that very few people have benefitted from this rally apart for the domestic traders who have been pumping the market (in many cases on margin) with the domestic liquidity created in the election run-up.

Risks are too high for us to build conviction in Turkey, however, it will be worth keeping an eye on polls in the coming months to see if sentiment changes once an opposition candidate for the presidency is chosen.

China regulatory headwinds abating

In March, Chinese Vice-Premier Liu He called for greater order and transparency in regulation of the tech sector. Our view was that this signalled a policy shift from Beijing, and that regulatory pressure was set to ease.

China made further supportive moves in December at the CCP’s annual Central Economic Work Conference (which shapes economic policy priorities), with policymakers declaring that it is essential to “support platform-based companies to leverage their abilities in leading development, creating jobs, and participating in international competition” (China Daily, December 2022).

This was soon followed by news that the China’s gaming regulator had granted 84 new game licences to domestic developers, and critically, 44 licences for imported games. These are the first approvals for imports for nearly two years. This shift from Beijing, which in August 2021 described gaming as “spiritual opium,” lifted the stocks of major gaming companies including Tencent and Netease.

Source: NS Partners Ltd., authorized and regulated by the Financial Conduct Authority.

China’s reopening accelerates

Following last month’s COVID 180 and rapid shift to reopening, Beijing pressed ahead through December despite news of a huge spike in cases (and presumably deaths) and hospital ICUs being overwhelmed.

China’s National Health Commission (NHC) announced a downgrade to the risk level for COVID (from class A to class B infectious disease), effective from 8 January. This effectively removes all centralised quarantine, contact tracing and risk area categorization throughout the country. Further, no control measures related to infectious diseases will apply at the border to all goods and people arriving from overseas. Travellers will only need a 48 hour pre-departure PCR test.

Outbound travel for Chinese citizens will also resume.

The NHC also reiterated that its focus will shift to boosting elderly vaccination levels, securing medical supply and healthcare resources (especially in rural areas), as well as prioritising treatment of severe cases.

Summary

Emerging markets bounced back throughout the month, fuelled by signals that inflation is peaking, China announcing measures to support the property market along with taking steps to reopen.

More cyclical markets such as Brazil and the Gulf states underperformed, as recession risks for major economies loom.

The DXY dollar index retreated, providing an additional tailwind for EM.

Portfolio Activity

Added to China H-shares, particularly names set to benefit from a recovery in consumer demand as COVID-zero is phased out.

China’s Policy Pivot

While CCP Congress drew focus to longer term structural risks brought about by Xi’s consolidation of power and confirmation of a third term, the event was followed by a series of policy announcements that addressed more immediate economic and political risks, that served as a positive catalyst for Chinese equities.

Property

Beijing announced one of the first major support measures for the property market in an attempt to put a floor under structural risks in the sector.

The measures inject around US $183 billion of credit into the property sector (Jeffries estimate) and should help to alleviate the wider economic drag brought about by the crunch.

Likely a turning point with additional policy support to follow to ensure the recovery in home sales and credit growth has legs.

Has Beijing ditched ‘wolf warrior’ diplomacy?

Beijing’s diplomatic charm offensive began with German Chancellor Olaf Scholtz leading a high level business delegation to meet with Xi and Li Keqiang. The Chancellor stressed the need for Germany and its European partners to pursue “areas of mutual interest” with China, but without ignoring controversies.

This was followed by Xi hosting a number of conciliatory meetings with Western leaders on the side lines of the G20 summit in Bali (with the exception of Xi’s confrontation with Justin Trudeau). One particularly noteworthy meeting was between Xi and Australian Prime Minister Anthony Albanese, the first exchange between leaders of the two countries since 2016.

COVID

Following a tragic apartment block fire (which was under COVID lockdown), in Urumqi (the capital of Xinjiang), protests against draconian COVID policy broke out across China. The size, messaging and geographic spread of the protests was significant, with protestors hitting out against Beijing and the local governments tasked with implementing the policy.

While the unrest was inevitably met with a swift police response, it acted as a catalyst for the acceleration of Beijing’s reopening agenda. Protests were followed by a surprising acknowledgement by Xi of the frustration being felt by many Chinese people, the cancellation of routine mass-testing in multiple cities, a reduction in mandatory quarantine periods for foreign arrivals (“7+3” days in a quarantine facility/at home to “5+3”), and state media pushing a new narrative that the Omicron death rate/severity is very low.

The fear is that opening up will inevitably led to a huge spike in COVID cases, which threatens to overwhelm China’s healthcare system, and risk the lives of the elderly population that is under-vaccinated.

To address this, Beijing has set hard vaccination KPIs for local governments: by end of January 2023, the vaccination ratio of people aged over 80 should reach 90%, and 90% of the people aged over 80 who meet certain health criteria must be fully vaccinated and have received booster shots. Additionally, 95% of the people aged between 60-79 who meet health criteria must be fully vaccinated and have received booster shoots. Current numbers are a long way off these targets, so we expect to see the rollout of a massive vaccination campaign.

Michael Zhang’s China trip

Analyst Michael Zhang travelled to China to see family during the month of November and relayed his impressions of consumer sentiment and attitude to COVID:

“Depending on where you’re at, activity levels might vary a lot. Recently in Chengdu, most restaurants were open, food deliveries normal, but restaurants and shopping malls were a lot less busy. The situation literally changes by the hour, you live your life by constantly checking the local community Wechat group for any announcements and might be ready to sleep at your friend’s place if yours is suddenly locked down for a few days. At one point, 30% of Chengdu’s residential complexes was locked down (despite no city-wide restrictions), but many of them suddenly reopened after the change of tone at central government level. Local governments are also nervously watching the message from the top.

It may take longer for Chinese people to shift their mindset, even if governments suddenly announce “we’ve defeated the virus”, a lot of people will still be cautious and unwilling to come out and spend, plus COVID cases and deaths will be rising. With this in mind, the recovery in consumption may be more gradual than many expect.”

Korea and the Inflation Reduction Act (IRA)

Portfolio manager Mazika Li travelled to South Korea on a research trip, and found that the IRA is at front of mind for many Korean companies looking to pursue major investment opportunities.

Asymmetric opportunities

“Free money” – the U.S. government is doling out subsidies in the form of tax incentives and production tax credits to attract investment in its renewable energy and battery supply chain (to the exclusion of Chinese sourcing). The initiative budgets for US$30 billion per year for the next 10 years.

Three key components:

Advanced manufacturing production credits – applies to solar, batteries, offshore and onshore wind technology.

EV tax credits for car buyers for up to $7,500 per car. To claim the full credit: a) at least 50% of the battery components must be manufactured/assembled in North America (and will go up to 90% by 2029), and b) if at least 40% of the battery materials were extracted or processed from countries which have a free trade agreement with the U.S., or recycled in North America (stepping up to 80% by 2027).

Investment tax credits for renewable, energy storage and critical minerals projects.

Who wins?

While building a U.S. plant is an expensive exercise, the strength of these incentives is such that Korean companies will be able to generate a healthy return on investment in a relatively short period of time.

Non-China suppliers of critical raw materials in the EV/renewable/battery supply chains should see increased demand.

Manufacturing equipment makers benefit from the capex spree.

The U.S. strengthens economic ties with allies in the West and East, and gains manufacturing know-how in key areas.

Background

The Gulf region is comprised of six nations that sit on some of the largest and most profitable hydrocarbon resources in the world. Large and successful investments in the extraction and commercialisation of those resources created tremendous wealth for the region in the last 50 years, with average GDP per capita growing from around $1,000 in 1970 to over $30,000 in 2021.

This transformational growth in a relatively short period of time far exceeded the region’s human capital capacity and necessitated that those nations attract foreign workers to fill the gap. Today, over 30% of the region’s ~50 million population is comprised of expatriate labour (ranging from ~90% in the UAE to ~35% in Saudi), the majority of which are employed in the private sector. In the last ten years, governments in the Gulf have embarked on a series of initiatives to promote the localisation of the private sector workforce (Saudisation) through schemes that encourage businesses to hire local citizens. A bloated public sector funded by dwindling oil revenues pushed labour localisation initiatives to the centre of domestic economic and social policy in the Gulf.

In this research, we focus on Saudi Arabia which is home to the largest population in the Gulf region (~35 million in 2021 according to the World Bank), and where Saudisation is a key policy pillar.

Saudisation has been negative for labour-intensive businesses that rely on foreign workers. That, naturally, has been the area that the market has most focused on. In this paper, we move the conversation to the top of the organisational hierarchy by examining the changes in the nationality of the CEOs of publicly listed main market Saudi companies. While Saudisation does not directly determine the nationality of a CEO, the underlying theme of localisation is indeed relevant and consequential for investors in the Saudi equity market.

Academic research measuring the performance of expatriate CEOs has found that executive characteristics have a measurable effect on company performance. One notable study by Sekuguchi et al. demonstrated that expat executives at multinational companies operating in Japan were more effective at increasing subsidiary revenues compared to their native counterparts[1]. Given the limited breadth of data on this subject, our aim -for now- is to use the data available to present a practitioner’s view on the subject.

Investment considerations

At Vergent, we place great emphasis on understanding the culture of the companies we are invested in. This is a difficult task that we reserve for the companies that we believe have compounding potential and we want to own for the long term. It takes years of interactions with business leaders and their teams to begin to appreciate a company’s culture. As such, our process combines quantitative analysis that captures the manager’s capital allocation track record with an understanding of their incentive structures, what drives them, and what irritates them (generally, we don’t invest in irritable CEOs). In Saudi, a country our team has been investing in for over a decade, this is a particularly difficult area to explore and is made more complicated by the fact that CEO tenures are generally short, they rarely own stock, and there is a reasonable likelihood they are expatriates. This does not compromise the quality of CEOs in Saudi, but simply requires a reframing of traditional management evaluation frameworks to reflect the nuances of the market.

The expatriate CEO

Expatriate CEOs come from neighbouring Arabic-speaking countries or from the West. American CEOs are a rarity, given the tax treatment of U.S. citizens’ incomes abroad which makes tax-free destinations like Saudi less attractive.

Many of the Arab expat CEOs built their careers in the region, and so naturally have an advantage over their western peers in the form of a more developed local network and a deeper understanding of consumer behaviour and culture.

Western CEOs are typically appointed directly into a CEO role. Most would have spent time in emerging markets with a multinational company previously. The advantage those CEOs have over their Arab expat and Saudi CEO counterparts is they tend to have a better grasp of global trends and a global multinational managerial experience.

The proportion of expat CEOs leading main market Saudi companies has decreased since 2016. Breaking that down, we find that IPOs contributed six expatriate CEOs by 2021, but that their net number dropped from 15 to 13 because of de-listings/mergers and a churn of expatriate CEOs that was filled by their Saudi peers.

Figure 1: Expats lead a decreasing proportion of Saudi main market companies (%)

Source: Saudi Exchange Filings, Bloomberg

Sector dynamics

Certain sectors have historically had an above average percentage of expatriate CEOs. For example, in telecoms, two of the three listed companies are majority owned by multi-regional companies (UAE’s Etisalat and Kuwait’s Zain) that have tended to appoint expatriate leadership from within their broader group to run the Saudi units. In addition, the telecom industry requires global experience and technical knowledge that is less likely to be found among Saudi CEOs.

Banking is another area where expatriate CEOs are over-represented (relative to the average). We attribute this to the presence of global banks in Saudi. Selective appointments made by leading banks to execute on transformational and highly complex growth strategies have also contributed to this over-representation. Al Rajhi Bank, the largest bank in the country by market capitalisation, hired an American CEO in 2015 to help build out and execute their growth strategy before transitioning to a very capable Saudi CEO in 2020.

Banking as a sector has the highest percentage of Saudisation in the economy. It is therefore expected that we will see more Saudi leadership, even at the traditionally expat-led global banks. Our conversations with those banks suggests that they are increasingly looking to localise at the top. Saudi banks like Al Rajhi have displayed much more agility in the market in the last five years and have materially outperformed global banks who are realising that this competitive environment requires local expertise at the top. A recent example is Saudi British Bank (majority-owned by HSBC) which hired Lama Ghazzaoui, a female Saudi, as CFO in March 2021.

We find that asset-heavy and cyclical industries have a greater proportion of Saudi leadership. Cement and petrochemicals are traditionally Saudi-led sectors. This is because these are established sectors with a good supply of capable Saudi managers with relevant educational and technical backgrounds. Many of these companies tend to be majority-owned by the state, and so naturally Saudi leadership is desired.

Figure 2: Proportion of Saudi main market companies who have had an expatriate CEO at any time since 2016 by sector

Source: Saudi Exchange Filings, Bloomberg

Family business

Family-controlled businesses are a notable feature of the Saudi main market. From a list of 169 main market companies with a market cap of over $200 million (excluding REITs), we found that 84 are family-controlled. For clarity of methodology, we define family control as companies where one or more families sit at the top of the shareholder list.

It is expected that the universe of family-controlled companies will grow as the stock exchange becomes a more desirable growth and exit option for those families. Therefore, an understanding of management dynamics in this area will only grow in importance.

Family-owned companies are particularly prominent in sectors like building materials, retail, real estate, education, and healthcare.

Of the 84 family-owned companies, 17 are still run by CEOs from the controlling family (family CEO). We expect the proportion of family CEOs to decline over time as businesses evolve and shareholder structures fragment with the entry of a new generation of family members who are less interested in being involved in the business. In the last two months, family CEOs of two retail companies resigned from their positions on account of operational and institutional underperformance.

Outsider CEOs (from outside the family) are primarily Saudis rather than expatriates. In fact, 94% of family-controlled companies are run by outsider Saudi CEOs, which is in line with the overall market average.

Saudi CEOs are better placed to fill professional CEO roles in family-controlled companies as they can manage the different stakeholders and processes involved in a traditionally family-run business.

We believe there are significant value unlocking opportunities for companies that effectively transition from a family CEO to a professional CEO. Irrespective of nationality, CEOs will need the freedom to operate, and an aligned compensation that preferably includes stock ownership.

Figure 3a: Proportion of CEOs by nationality in family-controlled businesses

Source: Saudi Exchange Filings, Bloomberg

Figure 3b: Proportion of family CEOs leading their family business today

Source: Saudi Exchange Filings, Bloomberg

Tenures

Intuitively, one would expect the tenure of Saudi CEOs to exceed their expatriate counterparts. Expats often return to their home countries for a variety of reasons and so leave the labour force more frequently. However, the data is inconclusive and suggests nationality is not a determining factor in CEO tenure. It should be noted that we are comparing a small population of expatriate CEOs to a large population of Saudi CEOs and so any observations should be noted in the context of that limitation.

Family-owned and operated businesses with family executives have less turnover. One example is Jarir Marketing where the founding family has occupied the chairmanship of the Board and role of CEO since it listed the company in 2003.

A few Saudi business leaders have been called to serve in government. Just this September, SABIC, the largest petrochemical company in the country, announced the resignation of CEO Yousef Al Benyan after he was appointed Minister of Education by royal decree. This impacts the tenure profile of Saudi CEOs.

We believe that limited stock ownership among professional (non-family) CEOs is a contributing factor to the overall short tenure observed in Saudi.

We observe that demand for the services of Saudi CEOs is high in the market. In the absence of stock ownership, Saudi CEOs are more likely to entertain and accept competing offers, resulting in tenures continuing to be relatively short.

Figure 4: Tadawul Main Market CEO tenure by sector (Since 2016)

Source: Saudi Exchange Filings, Bloomberg

Summary

The measurement of management performance in Saudi is an area of research that is nascent and limited by data constraints (i.e., a small number of observations). Any conclusions we make in this paper are therefore largely based on anecdotal evidence, with data used to sense check those conclusions and provide context.

Localisation and a new generation of Saudi business leaders is likely to see expatriate CEOs become less of a feature in the market. We believe this is positive as it should create more stability in tenures if coupled with aligned compensation structures and less competition for Saudi executives from the public sector.

Family-controlled businesses run by family CEOs have a great opportunity to unlock shareholder value through effective professionalisation of management.

We find that analysts and investors in the Saudi market are sanguine about management quality and alignment. There are numerous examples of the market looking through changes in management and not expecting negative future fundamental performance as an outcome.

We believe management changes carry strong predictive power of future company fundamental performance. Developing an understanding of the people and culture of Saudi companies can contribute to generating significant insights on the quality of a company. This leads to better investment decisions and improves the prospect of generating investment alpha.

[1] Sekiguchi T, Bebenroth R, Li D. (2011). Nationality Background of MNC affiliates’ top management and affiliate performance in Japan: Knowledge-based and upper echelons perspectives. International Journal of Human Resource Management 22 (5), pp. 999—1016.

Summary

We have been discussing the news flowing out of China’s 20th Party Congress (held from 16th-22nd October) at length over the past few weeks. While the press and market reaction was poor, there are some positives from the event that are underappreciated by the press/market. While political and structural risks remain elevated, we have kept our China weighting at neutral given positive signs of economic bottoming and improving liquidity data.

The event is important as the Congress report outlines high level, long term structural issues with more detailed economic policy due for release at the Central Economic Work Conference in December this year. Xi’s speech to Congress, a shortened version of the report, signalled no dramatic changes to policy. In addition, the new Central Committee of the CCP and Politburo Standing Committee were both announced at the conclusion of Congress. The Standing Committee, which is the apex of China’s political system, were all Xi loyalists and with Shanghai Party chief Li Qiang touted as the next Premier being the major surprise.

Below we list the positive, negative and neutral points which emerged from Congress.

Positives

Reiteration of development (implies economic growth) as a top priority and the real economy is the cornerstone (vs. pessimistic market speculations that this will come in second place after national security, or China would reject opening up). However, it seems that they’re calibrating the balance between development and security.

Continued emphasis on education, technology and innovation (in fact, higher priority vs. 19th congress). More support to semis and IT.

Relationship between consumption and investment: strengthen the fundamental role of consumption in economic development and the key role of investment in optimizing the supply structure.

Reiterated target that in 2035, China’s GDP per capita should reach that of a “medium-level developed country”, target was first announced 3yrs ago with no specific definitions, but it will carry more weight given it’s in the opening report of the congress this time.

Negatives

Major shock was the composition of the new Politburo Standing Committee – all belong to Xi’s faction, some are relatively young (by CCP standards) and perceived to lack central government experience.

The market reacted negatively to the news despite this direction of travel having been made clear years earlier when Xi changed the Party constitution in 2018 to remove the two term limit for the presidency. However, most China watchers were hoping to see some checks and balances in the Politburo make-up as per historic precedent.

Foreign investors were quick to dump Chinese stocks once the list of Standing Committee members was announced – especially H-shares and US ADRs, while A-share declines were more moderate.

Appointments broke unwritten precedent that any officials aged 67 or under at the time of a party congress can be promoted, while anyone aged 68 or over is expected to retire (Xi turned 69 this year).

Appeared to double down on zero covid.

Plenty of mentions of common prosperity (basic requirement of China’s modernisation).

Reiterates policy continuity in the housing market (housing is for living, not for speculation).

More security (89 times in his speech, vs. 55 in 2017), less reform (48 vs. 69 before). National security a higher priority (vs. 19th congress). The concept of national security is comprehensive, covering political, economic, military, technology, cultural and social aspects and integrating external and domestic issues. Including key aspects like energy, self-reliance of food & technology.

Relationship between the market and the government: the market plays a determining role in resource allocation, and the role of the government should be improved.

Neutral