The biggest investment challenge today is that bond yields are near all-time lows. This means lower bond returns in the future. Equities will continue to be a source of long-term return but developed market valuations are above average. Further, the integrated global supply chain means developed market equities are more interconnected today and don’t always provide the desired level of diversification. This is where the search for alternative sources of return and increased diversification begins.

Evolution of our investment platform

Part of our job is to find sources of differentiated return and evolve our investment platform to include new strategies when appropriate. This happens when the opportunity is significant and we can find the right talent. Two years ago, we found just such an opportunity and brought on an experienced team to manage frontier equity investments. We are now making this strategy available in client portfolios.

The opportunity in frontier markets

Let’s start with a definition. Frontier markets are made up of some of the fastest growing countries in the world that are not yet considered emerging markets. These countries are located in Southeast Asia, the Middle East and Africa and are largely overlooked by global investors. We focus on buying companies in countries with large populations and rising incomes. As incomes rise, large segments of the population move out of poverty and begin to increase their spending significantly on goods and services that weren’t affordable before. Our investment team finds companies that benefit from this growth in consumption. The companies we choose to own are very different to businesses in the developed world because they are meeting local consumption demand rather than being another supplier to global markets.

We also invest in companies that are exposed to other long-term trends exhibited by countries experiencing significant economic change. These include the benefits from urbanization, improvements in technology and access to healthcare, to name a few. These trends present investors with long-term growth opportunities. Along the way, investors are also providing much needed capital to companies that are under invested, which also has an impact on the development of these countries.

What about risk?

Managing risk in our portfolio is as much about what we don’t own as what we do own. For example, our investment universe has 8,000 companies of which we only expect to own 20-40. We start by avoiding higher risk industries and buy those companies with strong growth trends. We also focus on industries and companies with favorable environmental, social and governance (ESG) characteristics. This is an important part of our risk management process. We reward companies with strong ESG factors and engage those companies who need to improve. Once we have screened out the industries and types of companies we don’t want to own, we identify high quality companies with strong brands in large markets. Finally, we only invest in companies with experienced leadership teams and companies that we see as underappreciated by the market. Together, this helps us screen out risk in our portfolio and focus on the investments with the highest probability of success.

The nature of investing in frontier markets is that these are developing countries which often lack a truly democratic process and strong regulations. This can’t be ignored and our research process identifies these risk exposures and adjusts our targets and ultimately the exposure to the companies in that country. For some countries, the risk is too high and we avoid them altogether.

Adding frontier markets to a portfolio

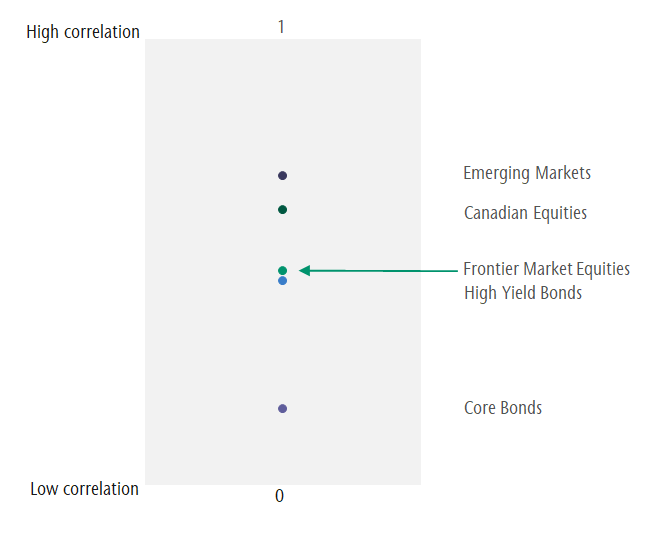

Adding frontier markets will increase portfolio expected return and diversification. The added diversification is important because it means we can add a modest allocation to this volatile asset class without meaningfully increasing risk. This is possible because frontier markets experience volatility for different reasons and often at different times. In the chart below we show the degree to which frontier markets and other asset class returns move in relation to global equities. The lower the asset class is on the chart, the more different the returns are and the greater the benefit of diversification.

Diversification benefit of frontier

Despite frontier markets’ low correlation to other parts of a portfolio, we recommend a modest allocation that varies depending on the portfolios’ mix of stocks and bonds. At modest allocation levels, investors can increase expected portfolio return and improve the relationship between the portfolio return and the risk required to generate that return.

Is adding frontier markets right for you?

As a firm we want to provide our clients with differentiated sources of return that will benefit their portfolios as long-term market outlooks change and new opportunities become compelling. We believe adding a modest allocation of frontier markets to a portfolio is a good option for many investors. However, the decision to change the portfolio asset mix should be made in conjunction with a fulsome discussion about the risk and return tradeoffs. We are here to help clients navigate a more challenging market environment and position their portfolio to meet their objectives while considering any unique circumstances. We can help you determine if adding frontier markets is right for you.