Archives :

As winter approaches, homeowners are confronted with the need to turn on their heating systems and the higher costs of additional heating. This winter, many US consumers will likely pay even more to heat their homes because of surging fuel prices and colder weather forecasts.

The National Energy Assistance Directors Association predicts increased winter heating expenditures across the board, with electricity up 1.2%, propane 4.2% and heating oil 8.7%. Natural gas is expected to be down 7.8%. Air conditioning and heating are by far the biggest sources of home energy use, comprising 51% of household energy bills. A main reason energy bills spike in winter is due to inadequate insulation.

This is where Installed Building Products (IBP) comes in – and why we’ve invested in this company. This week, we’ll share insights into our investment process and approach to selecting companies like IBP that we believe are poised to generate shareholder value.

Who is Installed Building Products (IBP)?

Founded in 1977 and based in Columbus, Ohio, IBP is one of the largest insulation installers in the US. In the late 1990s, the company embarked on an ambitious acquisition strategy to expand its reach nationally. IBP went public in 2014, at which point it was generating $432 million in revenue with earnings of 2 cents a share. Last year, its revenue reached $2.6 billion with adjusted earnings of $8.95 per share.

Besides insulation, which makes up 60% of its revenue, IBP has diversified into complementary building products (waterproofing, fireproofing, garage doors, rain gutters and more) for both the residential and commercial construction markets.

Target market

- Combined single family and multifamily insulation market has a ~$6 billion total addressable market (TAM).

- Complementary products add another $4 billion TAM ($1.4 billion for garage doors, $1.1 billion for shower shelving and mirrors, $800 million for window blinds and $700 million for gutters).

- Amount of insulation per home is increasing due to a greater focus on energy efficiency and stricter energy codes.

- IBP’s largest competitor is TopBuild (they each rank #1 or #2 in different markets).

IBP has a cost advantage

Industry suppliers lack power. The fiberglass insulation manufacturing industry is highly consolidated, with four players accounting for all sales (Owens Cornings 40%, CertainTeed 20%, Knauf 20%, Johns Manville 20%). While the supplier concentration would suggest high pricing power, insulation manufacturing is a capital-intensive business with high fixed costs. Ovens cannot be easily shut on and off. As a result, manufacturers are incentivized to run their lines at high capacity to cover their fixed costs and get leverage. This makes the industry more competitive despite its concentration. Given IBP’s scale, it can buy insulation foam at a larger discount than smaller competitors and save big on costs.

IBP’s growth strategy

- Organic growth is achieved through increasing penetration in developing markets.

- On average, an established IBP branch generates ~$4,400 per residential permit versus $2,200 for a new developing branch.

- Inorganic – M&A is part of IBP’s expansion story and it aims to acquire ~$100 million of revenue annually.

Strengths

- Leading positions in insulation installation, with a 28% market share up from 5% in 2005.

- M&A has been a part of its growth strategy since 1990.

- Scale = ability to buy product cheaper than smaller competitors.

Weaknesses

- Distribution arm is relatively small when compared to peer TopBuild.

- No centralized ERP = branches could be competing for the same business.

- Complementary products have lower margin due to current lack of scale.

Opportunities

- Complementary products.

- Capacity to penetrate developing markets.

- Increasing residential building codes = higher revenue per unit.

Threats

- Weakness in US residential markets.

- Current supply constraints cap organic growth.

- Supply shortage (COVID-19 period) or explosion/fire at a supplier plant (2018) can temporarily increase cost of raw material.

IBP management

IBP’s management, led by CEO Jeff Edwards since 2004, is a key part of the business’s success. Edwards, who joined the company in 1994 and became chairman in 1999, is one of its largest shareholders.

When we first spoke to Jeff and he walked us through how he built the business, we quickly realized he was a visionary leader with a solid plan for future growth.

He told us how he saw potential in the niche sideline of foam insulation. His rational was simple: every home, every building, needs insulation. He was not looking to reinvent the industry, but rather focused on delivering the best service to builders while acquiring successful businesses in various cities. The sales pitch to targets was also simple: being part of IBP means they can do what they like and not be bogged down by functions that aren’t core to their business, like insurance, human resources, accounting and payroll.

In 1994, IBP made its first acquisition with Freedom Construction in Columbus, Ohio, followed by several more in the ensuing years. The rest as they say is history.

Unseen value beyond the walls

Investment potential often lies hidden in plain sight, like the insulation in our walls. IBP has all the characteristics we look for in an investment: a small-cap company with what we believe to be tremendous growth potential with low debt, rapid revenue and earnings growth compared to its industry, and strong management.

Insulation may not be exciting, but not only does it conserve energy and reduce bills, it also represents a notable sector in our investment landscape. How often do investors overlook the potential in the ordinary and what opportunities might we uncover by paying closer attention to what others may miss?

Summary

- Treasury yields retreated through the month on inflation data that undershot market expectations (in line with our forecasts), with stocks and bonds celebrating the news.

- We remain cautious and view the exuberance with scepticism, and expect a weakening global economy and earnings downgrades to test the bulls.

- On a brighter note, rapid disinflation and the prospect of rate cuts in 2024 will precipitate a recovery in money numbers that could be the signal to tilt away from current defensive positioning.

Institutional quality is key to unlocking development

Analysis of qualitative macro factors in emerging markets is a cornerstone of our process, which is critical to identifying the potential for downside shocks that can wipe out investor returns (irrespective of how attractive a company’s fundamentals may appear). Given the relative fragility of institutions in EM, politics can have an outsized impact on a country’s progress up (or down) the development ladder, with elections often serving as critical junctures.

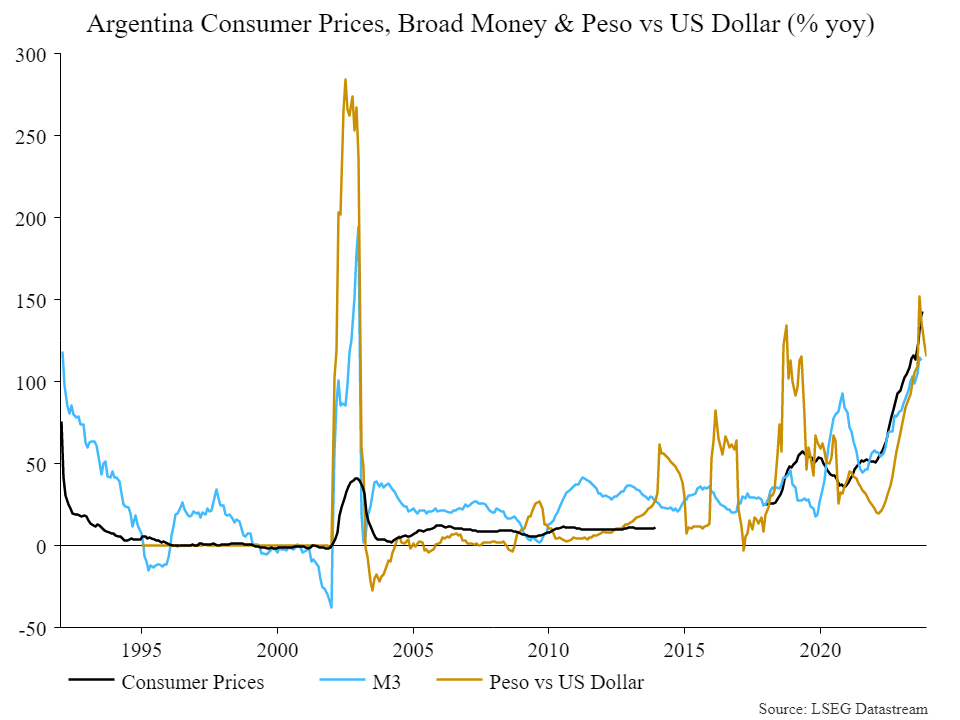

This month we saw the conclusion of national elections in Argentina, with right-wing libertarian and economist Javier Milei crushing the incumbent Perónists on a platform of radical economic reform. While markets have celebrated the development, does Milei’s election truly represent a structural turning point given the institutional forces that stand in his way?

Argentina a case study of the vicious cycle

A hundred years ago, Argentina was one of the richest countries on the planet, with the young and dynamic South American country outstripping the likes of even France and Germany. The rise and dominance of the left-wing populist Perónists in the 20th and 21st centuries (interrupted by a succession of military juntas in the 1970s and 80s) put an end to this.

For us, Argentina’s downward spiral from such an enviable position to today underlies the importance of institutional quality as the key determinant of whether a country climbs or slides down the development ladder. Vicious and virtuous circles of development (where political and economic institutions become either more extractive or inclusive) can form momentum that is hard to break. For EM investors in particular, who deal with countries with relatively more fragile institutions than DM counterparts, it pays to be mindful of what kind of cycle is at play in a country.

The book “Why Nations Fail” by Acemoglu and Robinson provides an excellent summary of these vicious/virtuous circles:

“Rich nations are rich largely because they managed to develop inclusive institutions at some point during the past three hundred years. These institutions have persisted through a process of virtuous circles. Even if inclusive in a limited sense to begin with, and sometimes fragile, they generated dynamics that would create a process of positive feedback, gradually increasing their inclusiveness. England did not become a democracy after the Glorious Revolution in 1688. Far from it. Only a small fraction of the population had formal representation, but crucially, she was pluralistic. Once pluralism was enshrined, there was a tendency for institutions to become more inclusive over time, even if this was rocky and uncertain process.” (Why Nations Fail, p364)

Clearly nothing of the sort occurred in Argentina over the last century. Instead, a confluence of economic and political crises from the 1930s onwards saw the country follow nearly half a century of growth with a lapse into domestic upheaval, the rise of Perónism and extreme political choices that fuelled a vicious circle causing Argentina to backslide.

Rise of the Perónists

While it is possible for countries to grow under extractive institutions, this will begin to falter at more advanced levels of development. Improving institutional quality is essential to break through to the next level.

“It is true that Argentina experienced around fifty years of economic growth, but this was a classic case of growth under extractive institutions. Argentina was then ruled by a narrow elite heavily invested in their agricultural export economy … [involving] no creative destruction and no innovation. And it was not sustainable.” (Why Nations Fail, p385)

Becoming Minister of Labour in 1943 following a military coup, Juan Domingo Perón was elected president in 1946. He then set about attacking Argentina’s institutions much as the previous military junta had done before him. He started by gutting the Supreme Court to remove any checks to his power, and sidelined the main opposition party by arresting its leader. The Perónists emerged as a new elite which shaped extractive institutions to their benefit.

“The Perónists won elections thanks to a huge political machine, which succeeded by buying votes, dispensing patronage, and engaging in corruption, including government contracts and jobs in exchange for political support. In a sense this was a democracy, but it was not pluralistic. Power was highly concentrated in the Perónist Party, which faced few constraints on what it could do, at least in the period when the military restrained from throwing it from power.” (Why Nations Fail, p385)

Is Milei’s election a critical juncture?

Following 28 of the last 40 years under Perónist rule, the country today battles its worst economic crisis in two decades as inflation spirals, poverty rates climb and – in the words of President-elect Javier Milei – the peso “melts like ice cubes in the Sahara.” Such is public frustration for perpetual economic catastrophe that Argentinian voters dumped the incumbents for libertarian rockstar economist Milei, who attracted 56% of the second-round vote, the most votes garnered by any candidate since 1983.

Source: NS Partners & LSEG Datastream

Milei campaigned on the promise of radical change and economic shock therapy. This includes dollarising the economy and eliminating the politicised central bank, putting the “chainsaw” to public spending, privatising state-owned companies, along with a host of controversial conservative social and libertarian reforms. Clearly, breaking the vicious cycle in play in Argentina will require radical policy change. Well implemented dollarisation could indeed work (with a deep recession) to restore economic order, working to reduce inflation, increase consumer buying power, and stabilise the economy in a way that enables better long-term economic planning while attracting foreign investment.

This sounds great in theory and markets have cheered the election results, but can Milei actually translate his victory into policy that passes through parliament when his party holds just 39 of 257 seats in the lower house and 8 of 72 in the senate? An alliance with centre-right former president Macri and his Republican Proposal party still won’t constitute a governing majority, but it will boost the chances of pushing through the reform agenda. For this to happen, however, it is likely that compromises will need to be made with Macri’s moderates and other neutrals. Will Milei, a libertarian firebrand who has gained so much popularity from demonising the political elite, be able to stomach a watered-down agenda?

How do we implement development theory in EM investing?

Our approach to macro analysis is not to place bets on such uncertain outcomes, but instead to assess the direction of travel and mark conviction in that country up or down accordingly. If Milei can beat the odds, then Argentina may gradually emerge as a hunting ground for investment opportunities.

For now, the reality is that powerful structural forces suffocate the country’s potential and make for a fragile environment that can easily wipe out investors lacking a robust approach to accounting for macro risk.

Une occasion de favoriser les avantages mutuels et de soutenir le développement durable

Cet article a été initialement publié dans le numéro 33 du Journal of Aboriginal Management (JAM), dans le thème Infrastructures : Bâtir un avenir meilleur.

La participation des Autochtones dans des projets d’infrastructures favorise l’autonomisation économique des communautés tout en contribuant à la réussite et à la durabilité globales des projets. Dans cet article, nous examinons certaines des façons dont les communautés autochtones peuvent participer aux investissements en infrastructures et nous soulignons les avantages que de tels partenariats peuvent créer.

L’investissement responsable nécessite la mobilisation inclusive des parties prenantes

Les projets d’infrastructures sont généralement des actifs corporels à grande échelle qui répondent à un besoin humain de base. Ces actifs sont essentiels au bien-être des communautés et au bon fonctionnement des économies locales. Les infrastructures englobent des projets comme les routes, les ponts, les écoles, les hôpitaux, la distribution et le traitement de l’eau, ainsi que la production et le transport d’électricité. L’aménagement et la construction de ces actifs nécessitent des investissements importants et l’apport de nombreuses parties prenantes. L’importance des projets d’infrastructure pour les communautés, leur nature à long terme et leur taille exigent une approche de placement responsable pour garantir et maintenir un permis social d’exploitation.

La mobilisation des parties prenantes joue un rôle crucial, car elle fait en sorte que les placements intègrent un large éventail de perspectives et produisent des résultats positifs. En fin de compte, l’investissement responsable consiste à produire des rendements financiers tout en tenant compte de l’incidence plus générale sur la société et l’environnement. Une approche inclusive de la mobilisation est essentielle pour garantir que toutes les parties concernées sont consultées.

On reconnaît de plus en plus l’importance d’inclure les peuples autochtones en tant que parties prenantes essentielles dans les projets d’infrastructures, en veillant à ce que leurs droits, leur patrimoine culturel et leurs intérêts économiques soient respectés et soutenus. Cela est particulièrement important dans des pays comme le Canada, où de nombreux projets d’infrastructures ont un impact direct sur les terres et les territoires des Autochtones, ainsi que sur leurs peuples et leurs communautés.

Cette sensibilisation accrue, combinée à une plus grande volonté d’inclusivité de la part des gouvernements et des entreprises, devrait contribuer à accroître la participation des Autochtones à l’aménagement responsable de nouveaux projets d’infrastructures durables au Canada. Toutefois, il est important que ces efforts soient axés sur le désir d’une véritable compréhension des points de vue et des priorités des Autochtones, ainsi que sur l’établissement d’une relation authentique qui vise à atteindre un avantage mutuel. Une telle approche favorise la transparence tout en encourageant la collaboration et la recherche de consensus, qui peuvent améliorer la prise de décisions et les résultats.

La collaboration favorise les avantages mutuels et le développement durable

Les partenariats positifs offrent une voie prometteuse vers des occasions d’investissement plus inclusives qui facilitent l’autonomisation économique des communautés autochtones et appuient l’aménagement, la construction et l’exploitation de projets d’infrastructures durables et de grande qualité.

La participation accrue des Autochtones peut contribuer aux efforts de réconciliation en encourageant le développement des entreprises autochtones, l’autodétermination et des résultats socioéconomiques positifs. Les flux de trésorerie réguliers générés par les investissements en infrastructures peuvent fournir aux partenaires autochtones des fonds pour répondre à un grand nombre d’objectifs : logement, soins de santé, éducation, installations récréatives, centres communautaires, développement économique, revitalisation culturelle, ou tout ce que la communauté valorise et priorise.

La mobilisation des communautés autochtones contribue également à protéger la valeur des investissements dans les infrastructures : elle atténue certains risques, permet d’éviter ou de résoudre promptement les conflits et les problèmes juridiques et rend l’aménagement et l’exploitation des projets plus fluides et efficaces.

Scott Munro, chef de la direction adjoint du Conseil de gestion financière des Premières Nations, l’a bien souligné dans son article sur l’évolution des normes ESG (JAM 32) : « La manière dont une entreprise prend en compte et respecte les droits des Autochtones déterminera l’impact sur sa valeur d’entreprise. Si l’entreprise ne peut montrer aux investisseurs et aux prêteurs qu’elle a obtenu le consentement libre, préalable et éclairé des peuples autochtones touchés par un projet, aussi bien intentionné et avantageux qu’il soit, le conflit sera inévitable. Le projet pourrait être retardé ou prêter le flanc à un litige coûteux, et l’entreprise fera face à une atteinte à sa réputation et à des actionnaires mécontents. »

En plus d’atténuer certains des risques associés aux projets d’infrastructures, la participation active des communautés autochtones dès les premières étapes de la planification des projets apporte des connaissances et des perspectives locales précieuses. Les communautés autochtones connaissent très bien leurs terres, leurs ressources et leurs pratiques traditionnelles. Ces perspectives contribuent à améliorer la conception des projets, à approfondir les connaissances dans les domaines d’importance archéologique, à gérer durablement les ressources, à préserver la biodiversité et à réaliser des évaluations d’impact environnemental plus robustes, tout en favorisant une surveillance et un entretien efficaces de l’environnement.

La collaboration accroît la durabilité des projets et renforce les efforts d’intendance en intégrant les perspectives et les pratiques autochtones qui se sont avérées respectueuses de l’environnement et résilientes au fil des générations. Elle peut mener à des résultats plus fructueux, tant pour le projet que pour les communautés concernées, en promouvant la collaboration, la confiance et la prospérité partagée.

Des occasions pour les Autochtones dans les infrastructures

Les collectivités autochtones peuvent participer à un projet d’infrastructures de différentes façons. Elles peuvent le faire directement par le biais d’une participation en actions, d’un partage des revenus ou d’une autre entente mutuellement avantageuse, ou encore d’une participation moins directe comme un placement dans une entreprise d’infrastructures publique ou un fonds d’infrastructures privé.

Le plus souvent, la participation est officialisée au moyen d’une entente négociée sur les avantages qui régit la relation entre la communauté autochtone et le projet d’infrastructures. Ces ententes énoncent les avantages et la rémunération spécifiques que la communauté autochtone recevra en échange de son soutien ou de son consentement à un projet, en veillant à ce que ses intérêts soient codifiés et reconnus dans le cadre des activités courantes du projet. Les ententes fructueuses facilitent la consultation et l’approbation de la communauté en tenant compte de ses objectifs sociaux, économiques et environnementaux, tout en assurant une distribution équitable des coûts et des avantages du projet. Les avantages peuvent comprendre la rémunération financière, des possibilités d’emploi, la formation professionnelle et les initiatives de développement communautaire.

La participation en actions permet à la communauté autochtone de participer directement aux facteurs économiques des investissements en infrastructures. En ayant une participation dans un projet, les communautés reçoivent des profits et prennent part à certains aspects du processus décisionnel. Les ententes de partage des revenus sont une autre façon pour les communautés autochtones de partager les profits générés par un projet d’infrastructures et peuvent constituer une importante source de revenus. Ces deux types d’ententes peuvent renforcer leur économie, favoriser la création d’emplois et améliorer l’accès aux ressources.

En plus des participations en actions et des paiements de redevances, on peut envisager d’autres ententes mutuellement avantageuses. Il est important de reconnaître que les besoins, les valeurs et les ambitions de chaque communauté autochtone sont uniques de la même façon que chaque projet d’infrastructures est distinct. Bien qu’il y ait des avantages à tirer parti de l’expérience passée et des pratiques exemplaires, il n’existe pas d’approche universelle. Chaque discussion doit s’amorcer dans le respect de la communauté autochtone et la volonté de dialogue ouvert qui aboutissent à une entente et à une collaboration productive.

Accent mis par CC&L Infrastructure sur la valeur partagée et les partenariats solides

CC&L Infrastructure investit dans des infrastructures présentant un profil risque-rendement attrayant, une longue durée de vie et la possibilité de générer des flux de trésorerie stables pour une clientèle très diversifiée : fiducies autochtones, fonds de pension publics et privés, sociétés d’assurance vie, institutions financières, fondations et fonds de dotation, particuliers fortunés, etc.

En tant que propriétaire d’actifs à long terme et intendant du capital de ses clients, CC&L Infrastructure se concentre sur la gestion responsable de ses actifs, qui comprend une approche systématique de l’évaluation des facteurs environnementaux, sociaux et de gouvernance. Nous croyons que cette approche améliore notre capacité à gérer le risque, protège la valeur de nos placements et bonifie le rendement des placements à long terme.

Notre société collabore depuis longtemps avec des partenaires autochtones. Il y a plus de 15 ans, nous avons collaboré avec les Premières Nations locales lors de notre premier investissement; aujourd’hui, nous coopérons d’une façon ou d’une autre avec les communautés autochtones pour plus de la moitié des actifs d’infrastructures canadiens en portefeuille. Il s’agit notamment de plusieurs installations hydroélectriques au fil de l’eau et projets d’énergie solaire dans lesquels nos partenaires autochtones détiennent une participation directe à nos côtés.

CC&L Infrastructure est membre du Groupe financier Connor, Clark & Lunn Ltée, une société de gestion de placements détenue par ses employés, dotée d’une structure multientreprise et dont les sociétés affiliées gèrent collectivement un actif de plus de 188 milliards de dollars canadiens.

2024 is shaping up to be a historically significant year for elections, with around half of the world’s population having the opportunity to vote. An estimated 76 countries will hold elections in 2024, including eight of the 10 most populated (Bangladesh, Brazil, India, Indonesia, Mexico, Pakistan, Russia and the US). Europe will witness the most election activity, with 37 countries voting, followed by Africa with 18.

US elections: The world watches

The US election in November, when voters will choose the next president, the entire House of Representatives and a third of the Senate, is expected to dominate headlines. The most likely scenario is a rematch between President Joe Biden and Donald Trump.

The shifting focus of Europe’s political landscape

The European Parliament elections are in June and the topic of migration will likely be at the forefront of debates. If current trends persist, the EU could see the highest number of asylum applications since the 2015-16 refugee crisis. Once thought of as a solution to labour shortages, migrants are increasingly being viewed by some European politicians as a security threat, despite ongoing worker shortages. This could lead to a meaningful political shift toward stricter immigration controls.

Dutch elections: A sign of the times?

The Netherlands’ snap elections on November 22 were perhaps a glimpse of what is to come, with the far-right Freedom Party led by Geert Wilders winning unexpectedly. No party achieved more than 25% of the vote, necessitating coalition talks that could stretch well into 2024. In addition to a strict stance on immigration, the Freedom Party campaign included higher taxes on banks, which negatively impacted Dutch bank stocks the following day. However, the Amsterdam Stock Exchange remained stable after the election due to the pending coalition formation.

Poland’s election results as a market catalyst

Poland’s October elections saw a major upheaval, with the long-ruling nationalist party being replaced by pro-Europe parties, lifting Polish markets the following day.

From voting booths to market trends

That is not to say all elections wield the same influence. Russia’s elections are unlikely to challenge Vladimir Putin’s stronghold. Brazil and Turkey will hold local or municipal elections, while the EU will elect its next parliament.

India, the world’s largest democracy, is likely to see Modi’s party re-elected in May despite some recent discontent. Indonesia will also hold elections early in the new year.

Taiwan’s January elections, important for their geopolitical implications, are expected to see the pro-independence party maintain control. It remains to be seen how the country’s relationship with China will develop from there.

Understanding the election effect on markets

US Bank reports that the S&P 500 Index typically experiences lower returns due to investor uncertainty before US presidential elections, with stronger returns in the following year regardless of the election outcome. Notably, returns tend to be higher when an incumbent party is re-elected and when one party wins decisively, suggesting larger policy changes.

Investing smart in election years

We believe our diversified portfolio is especially critical in periods of uncertainty. Election outcomes can heavily influence economic policies, affecting taxation, regulations and economic reforms. These changes have the power to shape various sectors and industries in profound ways. Safeguarding your investments by diversifying across different securities and industries is a wise strategy.

The role of quality companies

Quality companies that demonstrate enduring strength, guided by capable management and driven by long-term secular trends are well-equipped to weather the market’s ups and downs. Their resilience and adaptability often become key to their sustained success, offering a more grounded perspective for investors looking beyond the immediate horizon of shifting politics.

The US commercial real estate (CRE) sector is experiencing heightened concerns due to increasing interest rates and diminishing credit availability. In the third quarter, US banks faced challenges from the CRE loans in their portfolios. For instance, Morgan Stanley allocated an additional $134 million for credit losses, in addition to the $161 million provisioned in the previous quarter, attributing this to worsening conditions in the CRE sector. Bank of America saw its nonperforming loans surge by $707 million, reaching $4.8 billion in the third quarter, driven primarily by CRE.

While it might seem like the entire sector is facing turmoil, it is important to note that CRE includes a wide range of assets. Segments like industrial, retail and hotels remain relatively stable, whereas offices spaces are facing substantial difficulties.

JLL reports that the US office vacancy rate has soared to 21%, a peak not seen in over 25 years as of Q3 2023. The imbalance between supply and demand is reflected in the 18.3 million square feet of negative net absorption, contributing to an annual total occupancy loss of 51 million square feet, although the vacancy rate differs significantly between the high-quality segment of the office market and the more obsolete ones.

Furthermore, the Trepp CMBS Special Servicing Rates for offices, which tracks the share of loans at risk of default, surged to over 8%, the highest since May 2017. This increase suggests more challenges ahead.

The sector also faces a huge refinancing hurdle. From 2023 to 2025, nearly $1.36 trillion in CRE loans will mature, a quarter of which are collateralized by office properties. Even with prevailing rates, new lending rates are likely to be 3.5 to 4.5 percentage points higher than existing mortgages.

The combination of high vacancy rates and rising interest rates complicates refinancing efforts. Lenders and CMBS investors have significantly tightened underwriting standards, pushing the loan-to-value (LTV) ratio to around 53%, the lowest in 23 years, and well below the historical average of around 65%.

This shift and higher financing costs could devalue office properties by around 20% for prime buildings and over 60% for lower-quality ones. While public market valuations are resetting, the private market has been slower to respond. A narrowing valuation gap between these markets is expected as risks persist.

The increase in office landlords defaulting on loans is concerning, with some properties falling below their mortgage values, prompting landlords to surrender properties to lenders. Even leading office owners like Pacific Investment Management Co. and Brookfield defaulted on their mortgages earlier this year. Most landlords have managed to maintain their mortgages due to typically long-term office leases, but as more mortgages come up for renewal, we expect an increase in defaults.

The typical capital structure in CRE is around 30% to 40% equity and 60% to 70% debt, with banks owning around 60% of the loans. Therefore, there is concern that the challenges in the CRE, especially the office sector, may trigger another banking crisis.

The basic problem is an oversupply of office space. Solutions like converting office spaces to residential use are being discussed, but only 10% to 15% of US offices are suitable for residential conversion. Government support may be necessary to incentivize and facilitate these conversions. Cities like Boston, New York, Washington DC, Chicago, Portland, Los Angeles and the Bay Area have already started incentivizing office conversions since the pandemic.

In our portfolios, we hold a few positions with exposure to commercial real estate:

IWG, which we talked about in a recent commentary, is the world’s largest provider of workspace solutions. While the growth outlook for traditional offices is in question, demand for flexible workspace has been growing, driven by the structural growth in flexible and hybrid working. Higher vacancy rates at office buildings also allow IWG to negotiate better lease terms with landlords. With a major competitor WeWork fading out of the landscape, IWG is well-positioned to expand its network.

Savills, established in 1855, is a leading global real estate advisor with expertise in various segments including residential, office, industrial, retail, leisure, healthcare, rural and hotel property, and mixed-use development schemes. Its revenue is diversified, with 40% from transaction advisory (30% commercial, 10% residential), and 60% from stable segments like investment management and property management. Despite a decline in transaction advisory business in the first half of the year, revenue growth in property management has kept its business relatively stable. Savills generates over 85% of its revenue from the UK, Asia Pacific, Continental Europe and the Middle East, with less than 15% from North America. Office occupancy rates are higher in Asia Pacific (79%) and Europe (75%) compared to the Americas (50%), suggesting less distress in these regions. Savills has a strong balance sheet to weather the current turbulent times.

The hotel sector, while hit hard during the pandemic, is recovering faster than offices. With international borders reopening and a surge in travel demand, hotel occupancies, especially in cities like London, New York and Tokyo, are improving and contributing to a strong investment outlook supported by fundamental performance.

Melia Hotels, a major holding in our strategies, is seeing strong bookings and improvements in occupancies and RevPAR. The company operates 350 hotels, with nearly 92,000 rooms globally. Despite its quality assets, it is trading at a significant discount to its net asset value, but increasing transaction volumes in the industry at higher multiples may reduce this discount.

We recently initiated a position in Hoshino Resorts REITs (HRR). Sponsored by Hoshino Resort, HRR has an extensive hotel portfolio, including upscale resorts and city hotels. Its flagship hotels managed by Hoshino Resorts show a strong recovery, with RevPAR 20% above pre-pandemic levels.

Despite ongoing challenges in the CRE industry, we believe the resilient business models and strong balance sheets of the companies in our portfolios will help them navigate these difficulties.

The strategy focuses on investing in frontier and emerging market companies that our team expects will benefit from demographic trends, changing consumer behaviour, policy and regulatory reform, and technological advancement.

Below, we discuss some of the key factors influencing returns and share observations on the portfolio and the markets.

Information Technology

The strategy saw strong returns from the technology portfolio in the quarter. A significant contributor was Vietnam’s FPT Software (FPT), which featured prominently in agreements between Vietnam and the United States following the upgrade of their relations to a Comprehensive Strategic Partnership. This development signals that the US views Vietnam as a strategic alternative in diversifying its technology supply chain away from China. FPT’s technology-focused educational institutions are instrumental in building the human resources necessary for Vietnam to ascend the global manufacturing value chain. They also strengthen the company’s human capital advantage in its ~$1 billion annual IT outsourced services business in key global markets like Japan and the US.

We also saw strong performance from HPS Worldwide, the Morocco-based payment technology software company. Despite being in a heavy investment phase, the company maintained stable margins and grew its revenue by 17% year-over-year in 1H 2023. HPS recently won a major Canadian bank client and subsequently opened an office in Montreal to support that contract. By virtue of its global presence, HPS is a long USD business which provides a hedge against a rising US dollar.

Financial Services portfolio

The strategy experienced mixed performance from the financials portfolio in the quarter. Kazakhstan’s Kaspi.kz continues to deliver exceptional results, (~50% EPS growth in the first nine months of 2023), demonstrating the uniqueness of its super app product, which continues to record globally leading levels of engagement (65% of its 13.5 million average monthly users transact daily) driven by leadership in e-commerce, payments, and lending. We added to our investment in Kaspi at the beginning of the quarter following the company’s strong second-quarter results.

We’re also optimistic about developments at CTOS, Malaysia’s leading credit reporting agency. The company’s recent acquisitions in Indonesia and the Philippines in the area of alternative data, such as phone bill payment history, are expected to enhance the proprietary database used by its institutional lending clients. CTOS has affirmed its guidance for revenue growth of 28% and EBITDA of 23% for the lower end of the range in 2023. These acquisitions and affirmed guidance reinforced our confidence and led us to add to our investment in CTOS this quarter.

On the other hand, Kenya’s Safaricom underperformed in the quarter due to challenges related to its 2022 expansion into neighbouring Ethiopia, which have complicated the investment case at a time when its home market of Kenya is experiencing macroeconomic headwinds. While we acknowledge that Ethiopia’s 100-million-person population is a blue ocean for communication and financial services (Safaricom’s forte through the M-PESA app), the capital investment required is considerable and likely to weigh on margins for the next few years. With an enterprise value of approximately $4.5 billion and an EV/EBITDA of ~5x, we believe the shares are undervalued and reflect concerns over the Kenyan Schilling and the impact of the Ethiopia investment.

Consumer portfolio

It was a difficult quarter for the strategy’s consumer portfolio, punctuated by an earnings miss from Sido Muncul, the Indonesia-based herbal medicinal consumer company behind the Tolak Angin brand. Sido’s second-quarter results reflected a challenging environment for a large majority of Indonesian households, who are experiencing pressure on their incomes and are down trading or deferring non-essential purchases. Despite this, Tolak Angin’s market share grew in the first half of 2023 from an already high 75%, although the total profit pool for the category was down significantly. We reduced our exposure to Sido Muncul in recognition that the consumer environment is likely to remain challenging. However, we continue to own the company given its debt-free balance sheet, brand equity, and dominance in a category that is culturally entrenched. Rising health awareness post-COVID and a potential income recovery next year should eventually revive demand for its products. Indonesia will hold general elections in 2024 and we expect that economic activity and consumer demand will start picking up in the fourth quarter as election-related spending kicks in.

On the positive side, Century Pacific Food Inc., the Filipino food and beverage company, was included in the country’s main market index, reflecting its increased free float market capitalisation. This inclusion led domestic fund managers to bid up the shares, offering us an opportunity to reduce our position given the non-fundamental nature of the event, and the valuation opportunity it presented.

Healthcare portfolio

Quarterly returns were negative from the healthcare portfolio, mainly due to the weak share price performance of laboratory and diagnostics company, Integrated Diagnostics Holdings (IDH). The deteriorating outlook in Egypt is having an adverse impact on IDH’s margins, and the increased risk premium associated with Egyptian assets is also impacting the company’s valuation. That being said, we did see the CEO step in and buy shares in the market in October, a move we interpret as a positive signal regarding the valuation.

At the end of the quarter, we invested in Hermina Hospitals, Indonesia’s largest healthcare provider, which operates a chain of 47 hospitals in a country of around 250 million people. We are bullish about the healthcare reforms being implemented in Indonesia, and the large demographic opportunity that should support visible growth for years to come. While these are long-term drivers, Hermina’s investment in upgrading its operational systems through technology and improvements in patient experience is enabling significant near-term margin expansion, positioning the company for profitable growth in the next five years. Hermina was removed from the FTSE Emerging Small Cap Index in September, which resulted in selling pressure from index funds. We took advantage of this non-fundamental event and invested at what we deem to be attractive valuations.

Outlook

While the environment globally remains challenging, we see openings to deploy capital at attractive valuations. The fundamental metrics of the portfolio remain healthy: our companies are unlevered, generate high EBITDA margins of around 25%, and deliver returns on invested capital of approximately 18%. These metrics are the output of a dynamic research process that aims to identify high-quality companies exposed to secular themes that offer our chosen companies opportunities to sustain strong earnings growth over the next five years.

Vergent Asset Management LLP

MENA equity markets posted negative returns in the quarter (-1.3%) as indicated by the S&P Pan Arab Composite Index. However, they still managed to materially outperform emerging markets, which declined by -3.7% (as measured by the MSCI Emerging Markets Index). There was a high degree of performance dispersion in the quarter, with the Dubai Financial Market General Index up 11.2% and the Tadawul All Share (Saudi) Index down 3.5%. Year-to-date, the performance spread between the best-performing market (Dubai) and the worst-performing one (Kuwait) is a remarkable ~32%. This performance divergence theme is also evident within individual markets. Saudi mid caps, for example, outperformed the broader country index by a staggering ~16%, as seen in the difference between the MSCI Saudi Arabia Midcap and the MSCI Saudi Arabia Index.

This degree of performance dispersion in the region is unusual during periods of high oil price, which have typically raised all boats, so to speak. We attribute this phenomenon to several key factors that we believe will continue to influence return dispersion:

- Banks are no longer the only conduit between fiscal surpluses and the non-oil economy. Governments are now channelling more surpluses to sovereign wealth funds and directly funding their own economic programs. This is reducing the deposit opportunity set that was historically available for the banks. This is especially apparent in Saudi, where liquidity conditions are tight, evidenced by a headline loan-to-deposit ratio (LDR) of 96%. Conversely, UAE banks are enjoying an abundance of liquidity, with a headline LDR of 75%. This marked difference in balance sheets reduces the correlation in earnings between the two countries (given banks are the largest sector in both) and is partly responsible for the ~13% performance spread between Saudi and UAE banks on a year-to-date basis in favour of the latter as evidenced by the S&P country bank indices.

- Economic policies among Gulf countries are diverging more than ever. Kuwait’s political deadlock continues to be a drag on government spending and economic growth, a stark contrast to the Saudi pro-growth agenda that is being galvanised by a single vision and strong political will. The UAE is further solidifying its regional competitive advantage through ongoing economic liberalisation (more recently creating a federal authority to regulate the gaming industry), while Qatar appears to be experiencing stunted growth and a hangover from infrastructure investments made to prepare the country for the World Cup. These economic policy outcomes have obvious ramifications for sector-specific corporate earnings growth. At oil prices of $80 and above, earnings growth has a more pronounced impact on equity returns than sovereign fiscal health, in our opinion.

- The structure of equity markets is changing, with liberalisation and issuance activity attracting a new investor base, mainly institutional, to the region. Consider Saudi: the number of listed issuers increased from 188 in 2017 to 228 in 2023, and its weight in the MSCI Emerging Markets Index climbed from 0% to just over 4%. The deeper opportunity set and increased foreign ownership has reduced the contribution of highly correlated sectors like banks and materials in the Index (from 56% in 2021 to 43% today according to Morgan Stanley; note: this has certainly been aided by performance), which has contributed to reducing regional intra-correlations.

Lower market intra-correlations, higher return dispersion, and a deeper and less cyclical opportunity set is a powerful combination that will make stock picking in the region even more interesting, and possibly more rewarding.

Having witnessed the evolution of MENA markets over a long period (since 2005), we are in a unique position to understand the impact of the developments the region is undergoing on equity returns. Our historical understanding complements an adaptive and disciplined investment process rooted in a clear philosophy and focused solely on fulfilling our return promise to investors.

Vergent Asset Management LLP

Within the emerging market universe, plenty of ink has been spilt on extreme pessimism regarding China and over-the-top optimism around India. Yet, as the following chart shows, small-cap stocks in Mexico have quietly been a top performer in the post-pandemic period.

Mexico’s unforeseen rise

Growing tension between China and the US has positioned Mexico as an unintended beneficiary due to its geography and the trend among companies to shock-proof their supply chains through nearshoring.

Will this time be different?

As noted in an earlier weekly, we recently met with companies across various sectors in Mexico and most of the executives we spoke to seemed convinced that the nearshoring wave was sustainable while also being realistic about the challenges ahead.

They have good reason to be pragmatic. The last time the economic stars aligned for Mexico via NAFTA (North American Free Trade Agreement) in 1994, the country delivered mediocre growth of around 2% and watched on the sidelines as China took full advantage of a shift in manufacturing from the West. The question now is if the outcome will be any different this time.

The nearshoring challenge trifecta

Mexico’s ascent as a key supplier to the US can be traced to three key events: Trump’s tariffs on China in 2018, the US-Mexico-Canada Agreement (USMCA) that raised the bar for North American product content requirements and pandemic-induced supply chain disruptions. These factors, coupled with deteriorating US-China relations, have led to Mexico surpassing China as a supplier to the US this year.

However, as emerging market investors, we know that structural tailwinds that are attractive and advantageous today don’t preordain good outcomes. Our conversations with Mexican executives at the recent LatAm conference gave us a good reality check on the constraints they face on the ground, from infrastructure and water supply to the political climate.

Electric dreams, grounded realities

While Mexico generates sufficient power, it struggles with inadequate transmission infrastructure in its north that hinders industrial growth. We spoke to two industrial REIT developers that had to build their own power systems, passing those costs to customers. For perspective, Mexico’s state utility, CFE, built 150 kms of transmission lines in 2022 compared to Brazil’s Electrobras’ 8,679 kms.

Parched prospects

Water availability is another constraint, especially in Nuevo Leon, home to the populous city of Monterrey and the large, water-hungry beverage industry that includes Heineken and Arca Continental, one of Latam’s largest Coke bottlers that extracts billions of gallons of water under federal concessions. As recently as 2022, Mexico had declared a drought in the state of Nuevo Leon and yet Tesla plans to open a factory there.

The political maze

The final speed breaker to the nearshoring story could be politics and a volatile security situation by the US border. On the political front, Mexico’s President recently demanded that airport operators in Mexico reduce their tariffs even though they were bound by law via a concession system instituted in 1998. In terms of security concerns, the cities of Juarez and Tijuana, while strategically located across the border from California and Texas, have a history of gang violence and cartels profiting from piracy and counterfeiting.

Mexico’s unique competitive edge

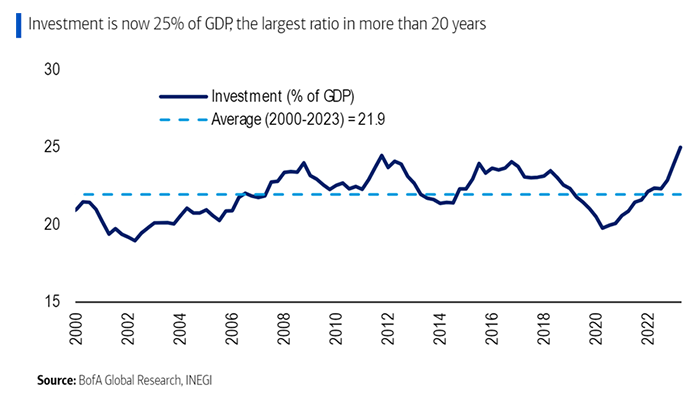

Despite these hurdles, Mexico offers several advantages, including lower labour costs compared to China, a younger workforce and significant investment in GDP, particularly in nearshoring and public infrastructure projects.

Unlocking nearshoring potential

With plenty of natural resources, a faster lead time and shorter distance to market, we think Mexico can continue to benefit from current trends with some policy support. Our Mexican holdings offer three different ways to access the nearshoring theme.

Grupo Cementos de Chihuahua (GCC MM) – Primarily selling cement in the US, GCC also operates in Chihuahua. It benefits from strong volume demand generated by the region’s growing industrial sector, particularly maquiladoras and warehouses near the Texas border. Recently, GCC expanded its Samalayuca plant and now supplies cement to about 85 projects in Northern Mexico, serving clients like Foxconn, Wistron and Pegatron.

Regional SAB de CV (RA MM) – Known as “Banregio,” this Mexican bank specializes in lending to small and medium enterprises, with a strong focus in Neuvo Leon, its home state and a big beneficiary of the nearshoring trend. With about 45% of its assets in the region, Banregio is poised to benefit from the growth of industries supporting multinational corporations relocating to Mexico, thanks to low credit penetration and an expected easing cycle.

Grupo Aeroportuario Del Centro Norte (OMAB MM) – OMA, managing 13 airports in Central and Northern Mexico, sees its largest traffic accounting for nearly half of its total at Monterrey Airport. Despite recent concerns about tariff cuts, we remain positive on OMA both for its exposure to nearshoring and potential for growth in its commercial business. The company operates six airports closely tied to nearshoring, covering 33.5 million square metres of industrial gross leasable area, about 35% of Mexico’s total.

A crucial crossroads

The real intrigue lies not in what Mexico has already achieved, but in what it could accomplish moving forward. Will it leverage its current position to create a more diversified, resilient economy, or will it repeat the patterns of the past? As global dynamics continue to shift, Mexico could be a big winner and serve as a blueprint for other emerging markets navigating the balance between risk and opportunity.

WeWork’s downfall and IWG’s ascent

Last week, WeWork, once regarded as the world’s most valuable start up, declared bankruptcy. This decision followed weeks of speculation. WeWork’s mission of being the leading global co-working community came to an end due to its relentless pursuit of growth. Its initial misrepresentation as a tech company and consistent cash burn from unprofitable leases indicated overambition from the start. This development provides an interesting opportunity for one of our holdings.

With WeWork’s restructuring of its extensive 700-plus-location portfolio, IWG (IWG LN) stands to benefit from less competition and an opportunity to expand its own network. For years, WeWork imposed pricing pressures to attract members. Now, this industry-wide pressure should ease, to IWG’s benefit.

IWG, the world’s largest provider of workspace solutions, began its operations in Brussels over 30 years ago. With more than 4,000 locations across 120 countries, its early entry into the market has been advantageous. The company is currently trading at 5.44x EV/EBITDA, a notable multi-year low. It has demonstrated strong pricing power and momentum, with revenues up 14% in the first half of 2023, totaling a record £1.7 billion. The company has focused on revenue growth and free cash flow generation, which has helped strengthen its balance sheet by lowering net debt.

Several years ago, to boost its top line and margins, the company introduced a capital-light business model. This model is particularly interesting due to the lower CAPEX requirements because of sharing agreements with building landlords for office space renovations. IWG partners with landlords for management, operations and member recruitment in return for a management fee. Additionally, the model includes franchise agreements in two forms. The first involves master franchise agreements, where a partner buys out an existing IWG portfolio and commits to additional office roll outs, paying a franchise fee. The second form involves franchised locations in existing markets, where IWG partners with smaller franchise owners to open new centres in markets that IWG already has presence in. This strategy has gained traction, with 582 new centres opened this year compared to 421 in 2022.

For the last couple of years, IWG was affected by its association with WeWork, trading in parallel despite superior financial performance. Though the pandemic took a toll on the coworking sector, IWG continued to generate strong positive free cash flow and EBITDA margins consistent with the company’s historic levels. In contrast, WeWork was aiming to grow revenues, but showed negative EBITDA margins and free cash flow.

Source: Bloomberg.

Around September 2022, IWG’s stock price finally decoupled from WeWork’s as the troubles continued to brew for the latter. Following Q2 2022 results, it became evident that despite growing occupancy at WeWork offices, it continued to offer price cuts to members to contain retention rates unlike IWG that not only grew occupancy but was beginning to raise prices, a trend continuing to date.

In the current market, which still seems to favour some growth stocks with weak financials, we continue to prioritize companies with healthy balance sheets and promising profitable growth prospects.