Cycle analysis suggests economic and market weakness in 2026-27. A recent monetary slowdown is consistent with this perspective but needs to extend to confirm a negative scenario.

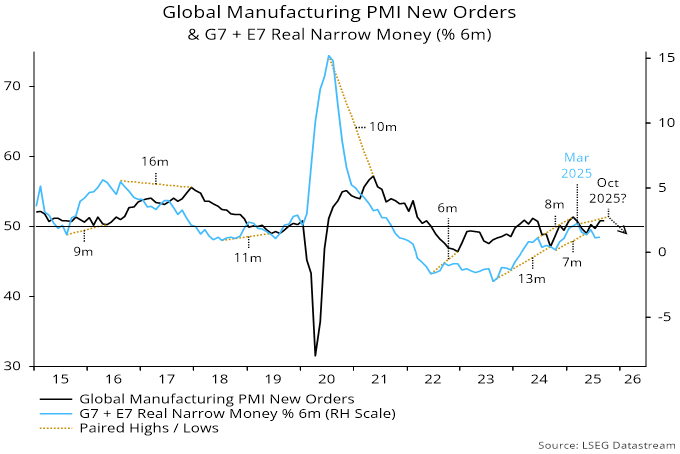

Global (i.e. G7 plus E7) six-month real narrow money momentum moved sideways in August, following a March-July fall. The previous low in real money momentum in October 2024 was reflected in a low in global manufacturing PMI new orders in May. Accordingly, the monetary slowdown since March could be mirrored by a peak and reversal in PMI new orders from around October – see chart 1.

Chart 1

The fall in real money momentum has been modest but an expected economic slowdown could become more serious than others in recent years, for two reasons. First, the stockbuilding and housing cycles have entered time windows to begin downswings. Secondly, labour markets are showing signs of weakness for the first time since the pandemic recession, raising the risk of self-reinforcing negative dynamics.

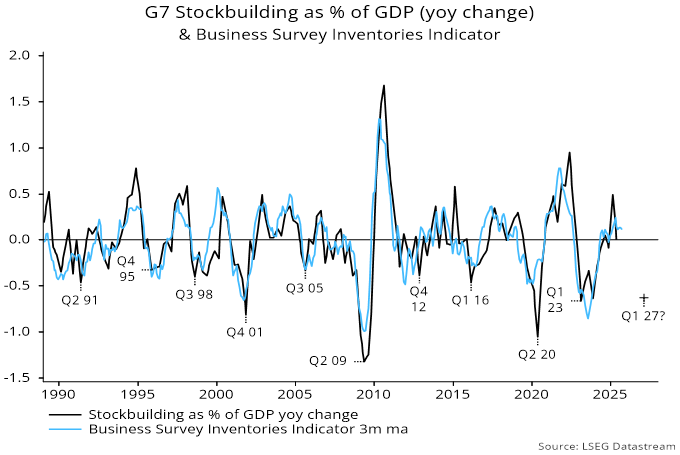

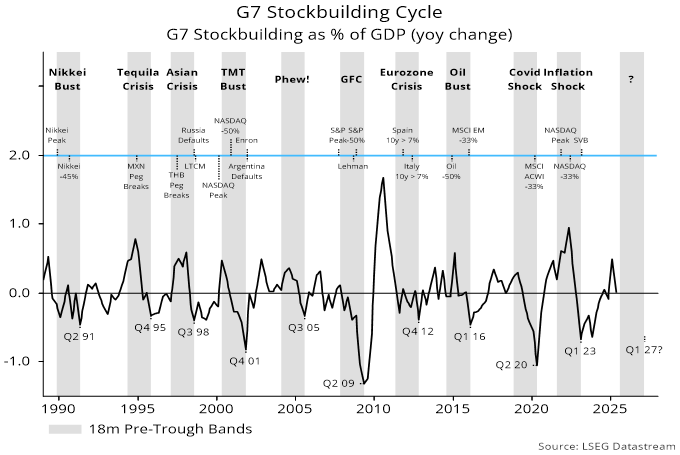

The working assumption here has been that the stockbuilding cycle will reach another low in Q1 2027, implying a four-year current cycle versus a 3.5-year historical average. Recent G7 national accounts stockbuilding data as well as an indicator based on business surveys are consistent with the cycle being at or near a peak – chart 2.

Chart 2

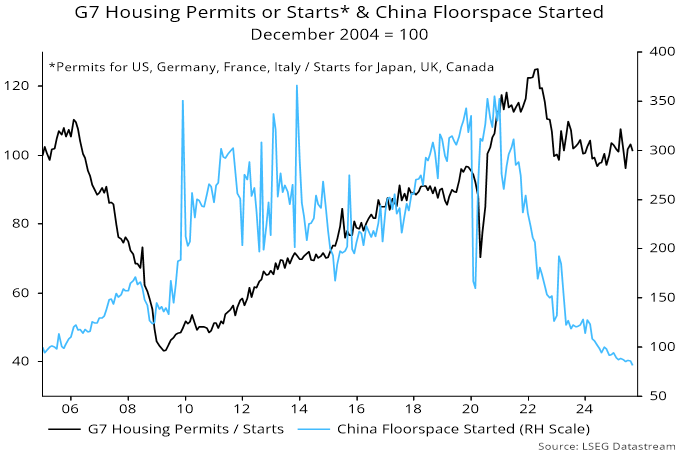

The housing cycle bottomed in 2009 and has ranged between 15 and 25 years historically, averaging 18 years. The pandemic-related money growth surge of 2020-21 appears to have resulted in the current cycle peaking early, in 2022. G7 housing starts or permits have been range-bound since early 2023 but rising unemployment could be the trigger for a break lower. China has been leading in the current cycle and starts are still falling – chart 3.

Chart 3

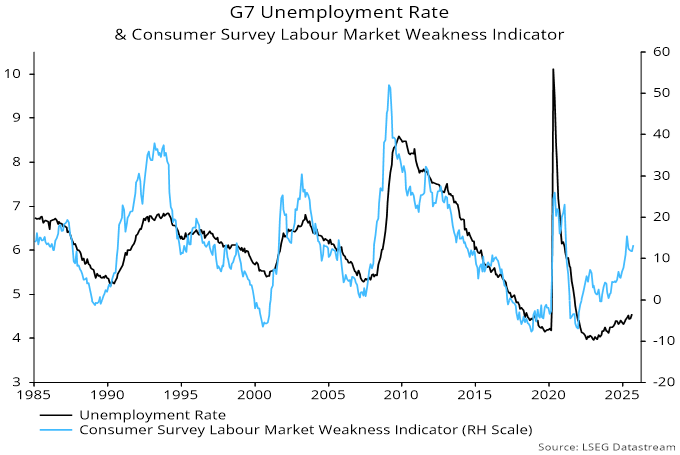

The suggestion that unemployment is on a rising trend is supported by consumer surveys, with a composite G7 indicator of negativity recently reaching a four-year high – chart 4.

Chart 4

Monetary policy easing, if sufficiently dramatic, could short-circuit negative cyclical dynamics. A dramatic move could occur conventionally if additional evidence of labour market weakness is accompanied by a downside inflation surprise, or unconventionally if the Trump administration succeeds in gaining control of the Fed. A large cut in US rates would magnify US dollar weakness, forcing other central banks to follow.

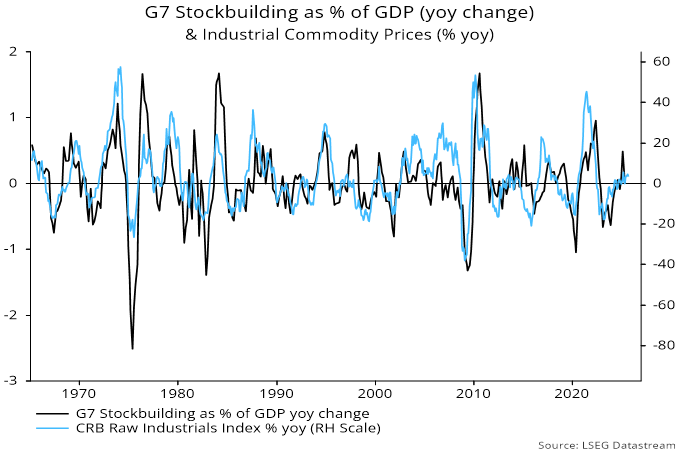

Inflation prospects are judged here to be favourable, at least through early 2027. G7 annual broad money growth remains subdued (4.3% in August versus a 2015-19 average of 4.5%), while stockbuilding cycle downswings are usually associated with weakness in commodity prices – chart 5.

Chart 5

Near-term US inflation numbers, however, will continue to reflect tariff effects. Elsewhere, central bankers focused on fighting the last war may be slow to respond to favourable surprises. As an example of hawkish bias, the ECB has gone on hold despite forecasting below-target inflation.

The alternative route to a large near-term fall in rates – a take-over of the Fed by the executive branch – still seems far-fetched, with the administration lacking scope to push through personnel changes on the necessary scale.

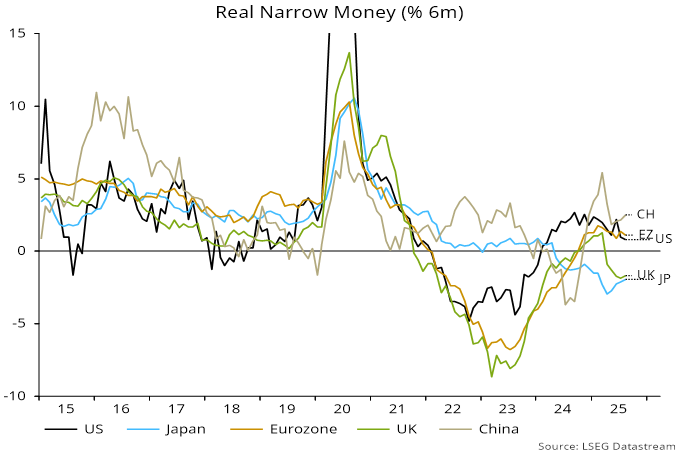

Among major economies, six-month real narrow money momentum is weakest in Japan and the UK, suggesting over-restrictive monetary policies and downside economic risk. Momentum is similar in the US and Eurozone but the US has slipped to a 17-month low, while a Eurozone recovery has stalled since Q1 – chart 6.

Chart 6

The Eurozone story seems to be that higher bond yields triggered by fiscal loosening along with a stronger euro have offset ECB easing. Optimists argue that German fiscal stimulus is only now arriving but the impact could be balanced by an early stockbuilding downswing – the stockbuilding share of GDP rose by 0.7 pp in the year to Q2 and is above its long-run average.

The recent decline in global six-month real narrow money momentum has been driven by the G7 component. Chinese momentum fell back in April-May but has recovered since, giving a modestly favourable signal for economic prospects.

The assumption of a Q1 2027 trough implies that the current stockbuilding cycle has entered its final 18 months. The 18-month windows before previous lows were usually negative for risk assets and marked by credit events or “crises” – chart 7. The possibility of simultaneous housing cycle weakness, as well outsized gains in the upswing phase of the current cycle, suggests greater-than-normal downside.

Chart 7

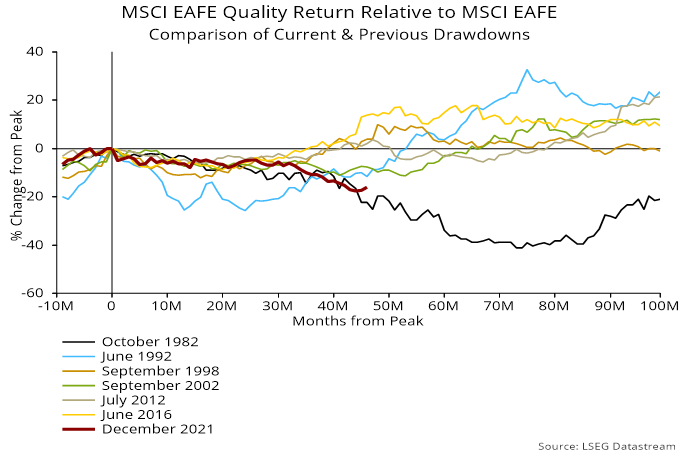

These 18-month windows were usually associated with cyclical equity market sectors underperforming defensives, following outperformance during the upswing (unusually strong in the current cycle). Stylewise, there was a weak tendency for quality to outperform, while momentum lagged its upswing gains significantly. The recent drawdown in relative performance of the MSCI EAFE Quality index versus MSCI EAFE was exceeded in magnitude and duration only in the early 1980s – chart 8.

Chart 8

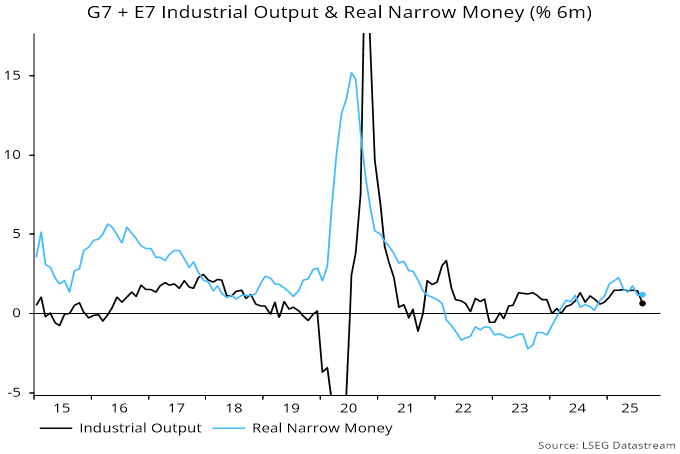

Six-month growth rates of global real narrow money and industrial output have been tracking closely with a small monetary excess on the latest readings – chart 9. The strength of markets appears to reflect a rise in the financial velocity of money more than ample liquidity, suggesting reversibility in the event of a cyclical deterioration in sentiment.

Chart 9

The two monetary conditions historically favouring EM equities – E7 real money growth above the G7 level and global real money growth above industrial output expansion – are currently in place, suggesting EM outperformance in the event of a near-term further rise in markets.