Recent economic data have been interpreted as supporting the view that global growth is showing “resilience” in the face of significant shocks, in turn suggesting scope for central banks to continue to dial up hawkishness.

This reading of the data is disputed here while monetary trends continue to signal a high probability of a recession by end-2022 followed by a sharp inflation drop in 2023-24. Central bankers ratcheting up interest rate expectations are as off-beam now as they were when engaging in outsized stimulus in 2020-21.

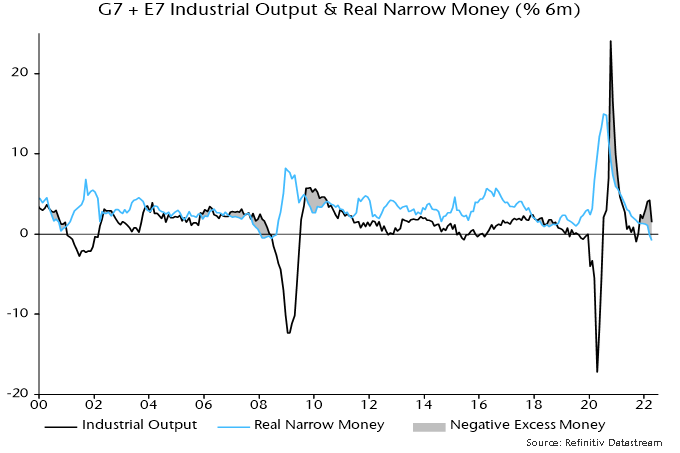

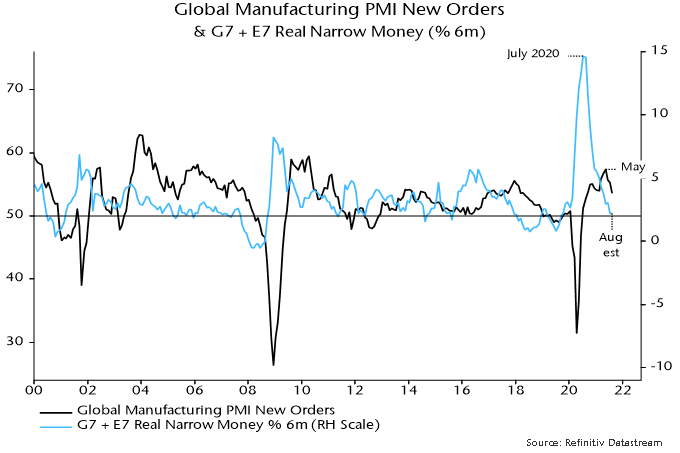

Additional April monetary data confirm that the six-month change in global real narrow money moved deeper into negative territory and has now undershot a low reached in June 2008 as the financial crisis and associated recession escalated – see chart 1.

Chart 1

The comparison with June 2008 is relevant in other respects. The two-year Treasury yield surged from 1.35% to 3.05% between March and June as the oil price spiked above $140 and markets priced in significant Fed tightening. The next move in the Fed funds rate, then 2.0%, was an October cut, by which time the two-year was back below 1.5%.

The fall in global real money momentum in late 2021 / early 2022 reflected rising inflation. Nominal money weakness has been the driver more recently.

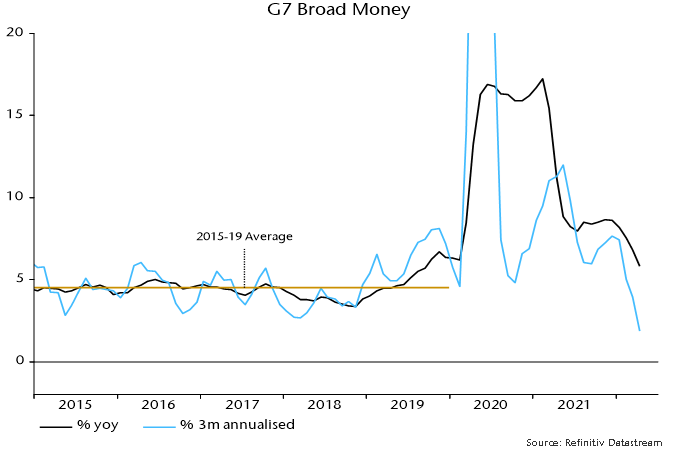

With Canada yet to report, three-month growth of G7 broad money is estimated to have fallen to 1.9% annualised in April – chart 2. Annual expansion is likely to have moved down to around 5% in May, close to the pre-pandemic average, based on weekly US data and a sizeable base effect.

Chart 2

Annual broad money growth peaked in February 2021, suggesting that a fall in CPI inflation will start in 2023-24 rather than later this year, assuming a typical lead time of about two years. An “optimistic” view is that the transmission mechanism has been accelerated by supply-side shocks, implying an earlier but higher inflation peak and a faster subsequent slowdown.

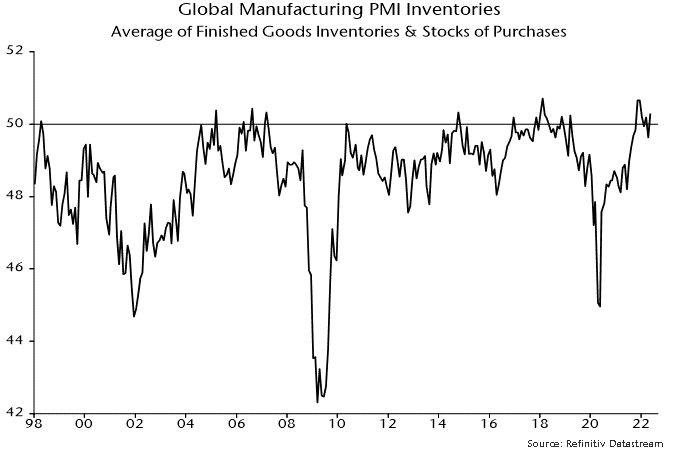

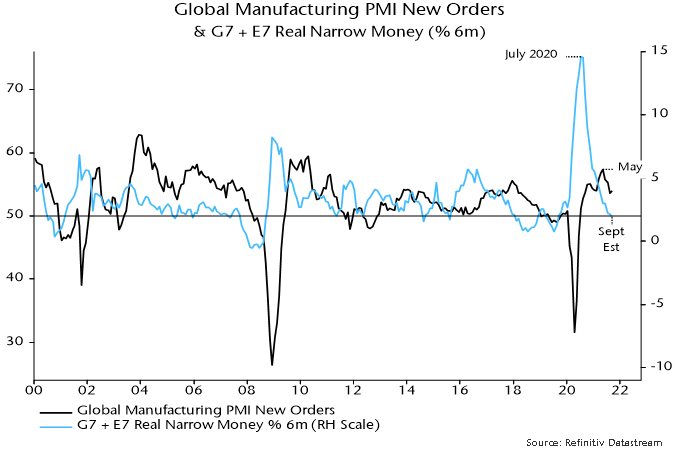

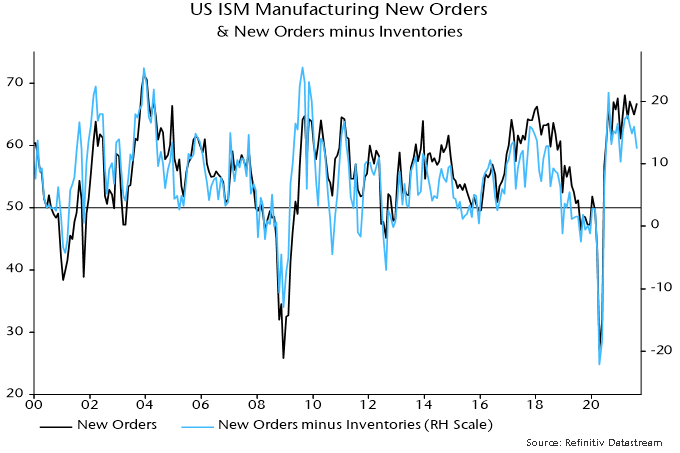

Recent news giving apparent support to the view that the global economy is displaying “resilience” includes May rises in new orders indices in the global PMI and US ISM manufacturing surveys. Both indices, however, are well down on three months earlier and the May recoveries were associated with further strength in stockbuilding – chart 3. A moderation of inventory accumulation – and likely eventual liquidation – will act as a major and sustained drag on order flow.

Chart 3

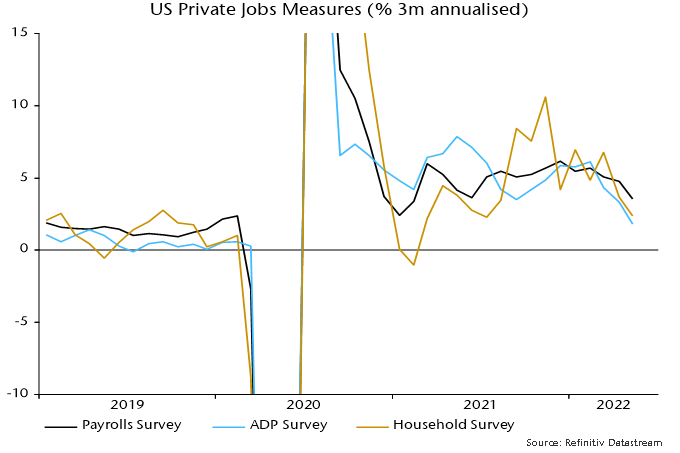

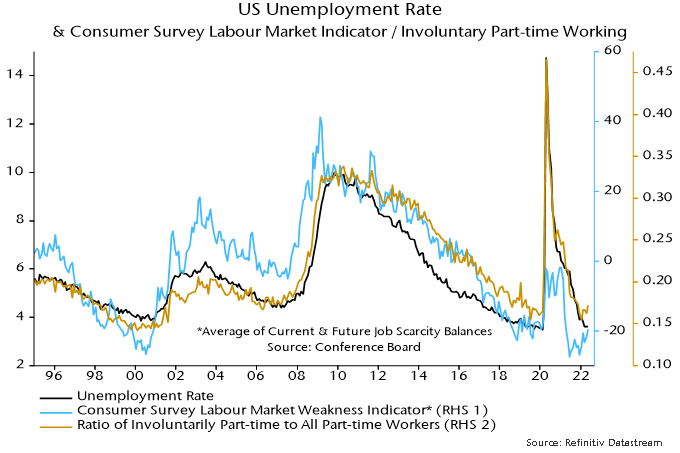

US payrolls growth beat expectations in May but alternative ADP and household survey employment measures have slowed sharply over the latest three months – chart 4. Meanwhile, weaker labour market responses in the Conference Board consumer survey and a rise in involuntary part-time working suggest that a sideways move in the unemployment rate in May is the precursor to an upturn – chart 5.

Chart 4

Chart 5

Recent UK monetary trends are consistent with a medium-term return of inflation to target, implying that the Bank of England should hold policy even though current inflationary pressures will be slow to fade and the consensus will claim that it is “behind the curve”.

The alternative would be to exacerbate a severe squeeze on real money balances that – on the view here – already guarantees a GDP recession.

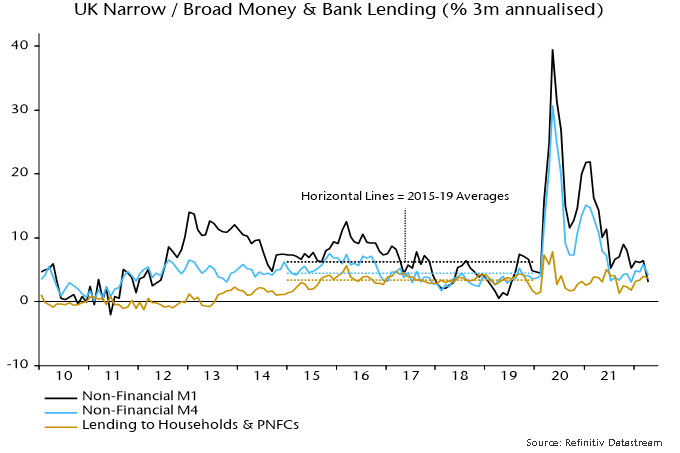

Satisfactory inflation performance in the five years before the pandemic was a consequence of low and reasonably stable money growth. Three-month expansion of the preferred broad aggregate here, non-financial M4*, averaged 4.4% annualised, mostly fluctuating between 2% and 7% – see chart 1.

Chart 1

The covid shock arguably warranted policy action to move money growth temporarily to the top of this range. Instead, the Bank’s grotesquely miscalibrated QE programme drove three-month growth to 31% annualised in May 2020. A subsequent sharp slowdown was followed by a rise to a second peak of 15% in January 2021 following an incomprehensible decision to extend QE in November 2020.

Three-month growth, however, has been back inside the pre-pandemic range since July last year – it was 4.2% annualised in April.

Monetary trends have yet to reflect fully recent policy tightening. The April-only numbers hint at further weakness: non-financial M4 rose by only 0.2% on the month, while non-financial M1 was flat.

The latest three-month increase of 4.2% annualised may overstate underlying growth because of retail investors switching out of mutual funds into bank and building society deposits in response to recent market losses. A broader savings measure including National Savings, foreign currency deposits and retail mutual funds grew by an estimated 2.9% annualised in the three months to April**.

A further rise in consumer price momentum, meanwhile, has intensified the squeeze on real money balances. Non-financial M4 and M1 fell by 3.4% and 3.3% (not annualised) respectively in the six months to April – chart 2.

Chart 2

Although three-month money growth has been running at a target-consistent pace for several quarters, the usual “long and variable lag” suggests that a normalisation of inflation may be delayed until late 2023 or 2024.

Economists were last week debating whether Chancellor Sunak’s latest cost of living support package would add to inflationary pressures. The net cost of £10 billion equates to only 0.4% of non-financial M4, i.e. the package won’t shift the dial on monetary trends and, by extension, inflation prospects even if fully financed via the banking system (unlikely).

*M4 holdings of the household sector and private non-financial corporations. **This assumes zero net purchases of retail mutual funds in April, following net sales in February and March.

Incoming monetary data continue to give an ominous message for near-term global economic prospects while suggesting major inflation relief in 2023-24.

Fed numbers released on Tuesday confirm that the US broad money aggregate tracked here* fell month-on-month in April, resulting in the three-month change turning marginally negative. Weekly data on currency in circulation, commercial bank deposits and money funds suggest another decline in May.

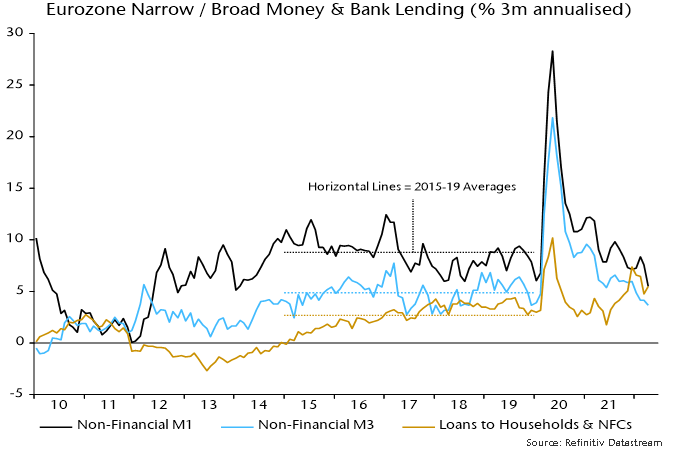

Monthly growth in Eurozone broad money**, meanwhile, was today reported to have fallen to 0.1% in April, pulling three-month expansion down to 3.7% annualised – see chart 1.

Chart 1

Three-month growth rates of narrow and broad money are now below pre-pandemic averages (i.e. over 2015-19). The ECB should wait to see if money growth rebounds before hiking rates but appears to be set on hawkish autopilot, with potentially disastrous consequences.

Three-month growth of loans to households and non-financial corporations remains solid but is below its peak and expected here to slow further as demand for inventory financing falls off and higher mortgage rates curb housing credit.

The slower expansion of broad money than lending mainly reflects a fall in banks’ net external assets – the counterpart of a basic balance of payments deficit – and an increase in their capital reserves. The Ukraine conflict is likely to have boosted capital outflows while causing banks to become more risk-averse. ECB purchases of government securities remained substantial in the three months to April, at the equivalent of 0.7% of broad money, or 2.7% at an annualised rate. Further monetary weakness is likely as this support ends.

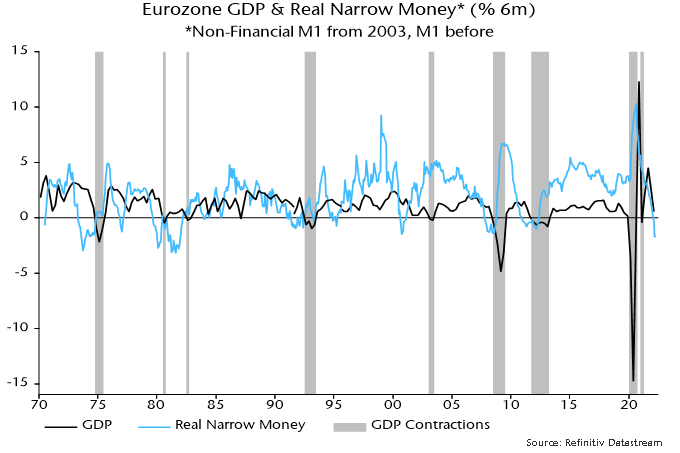

The slump in US and Eurozone nominal money growth implies a severe squeeze on real money balances, given current high inflation – consumer prices rose by 9.9% and 10.9% annualised respectively in the three months to April.

The current six-month rate of contraction of Eurozone real narrow money was exceeded only in 1973-74 and the early 1980s. Smaller declines in 1991, 2007 and 2011 also foreshadowed recessions – chart 2. There is stiff competition for the prize of worst recent official forecast but the March ECB staff projection that Eurozone GDP would grow by 4% annualised in Q2 / Q3 is a strong contender.

Chart 2

*”M2+” = M2 + large time deposits at commercial banks + institutional money funds **Non-financial M3

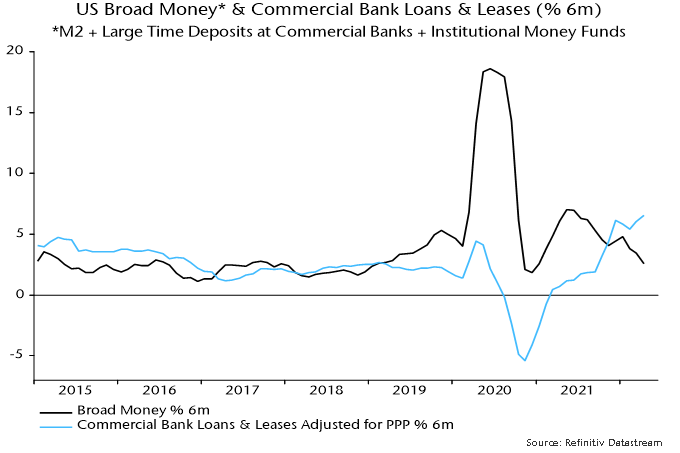

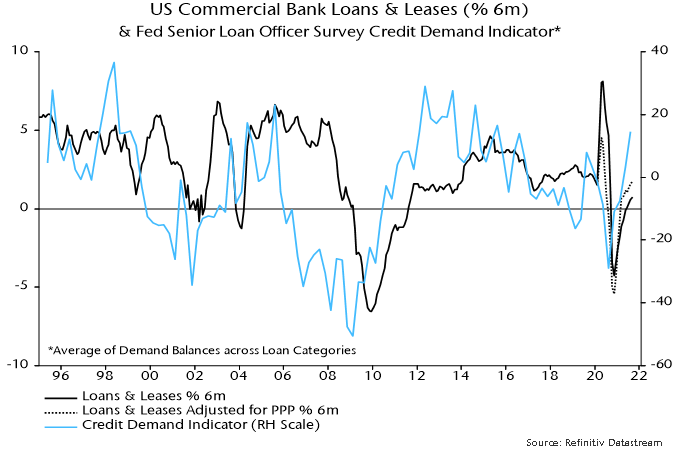

US broad money growth has slowed significantly despite a strong pick-up in bank lending expansion. How has this occurred and does lending strength portend a rebound in money growth?

The broad money aggregate calculated here* rose by 2.6% (5.2% annualised) in the six months to April, down from 4.5% (9.2%) in the prior six months – see chart 1. All the growth over the last six months occurred over November-January: the aggregate has flatlined over the last three months.

Chart 1

The monetary slowdown contrasts with further strength in bank lending. Commercial bank loans and leases, adjusted for Payment Protection Program forgiveness, grew by 6.5% (13.5% annualised) in the six months to April, up from 3.3% (6.6%) in the previous six months.

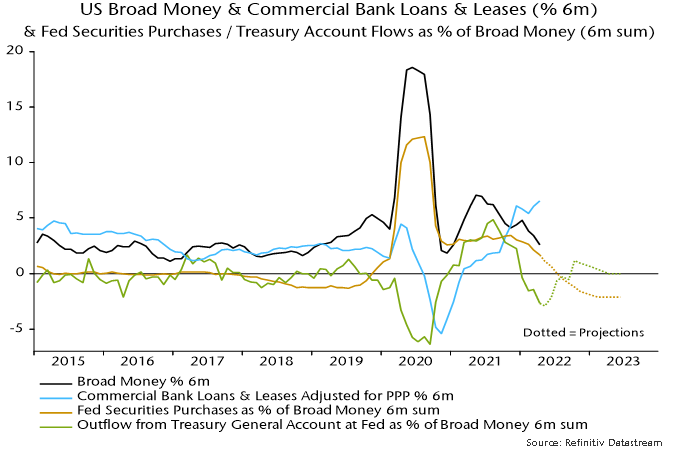

Q. What happened to the additional deposit money created by the expansion of banks’ loan books?

A. It was mostly diverted into the coffers of the US Treasury.

Political wrangling over raising the debt ceiling resulted in the Treasury running down its cash balance at the Fed from over $800 billion in mid-2021 to below $100 billion by December. This monetary injection boosted broad money growth late last year.

Since the ceiling was raised in December, the Treasury has “overfunded” the federal deficit to replenish its cash balance, which currently stands at over $900 billion.

The monetary inflow to the Treasury amounted to 2.7% of broad money in the six months to April – chart 2.

Chart 2

The monetary slowdown has also reflected – to a lesser extent – the wind-down of QE: securities purchases by the Fed were 1.7% of broad money in the six months to April, down from 3.4% in the prior six months.

Adding together the effects of QE and changes in the Treasury’s cash balance, there was a net monetary withdrawal of 1.0% of broad money in the six months to April, following an injection of 6.2% in the previous six months. This reversal more than offset the monetary impact of stronger bank lending expansion.

What happens next?

The Treasury’s latest financing projections assume a cash balance of $650 billion at end-September, representing a fall of about $310 billion from its level at end-April.

The Fed, meanwhile, plans to reduce its securities holdings at a monthly pace of $47.5 billion starting in June rising to $95 billion in September. This suggests cumulative QT of about $330 billion over the six months to October.

In combination, QT and changes in the Treasury’s cash balance may, therefore, result in a net monetary withdrawal of only about $20 billion, or 0.1% of broad money, in the six months to October, down from $280 billion or 1.0% in the six months to April.

In terms of the combined influence of the Treasury and Fed, QT effectively started in January and is about to slow temporarily before stepping up later in the year – assuming no further change in the Treasury’s cash balance beyond the expected fall to $650 billion and an ongoing $95 billion per month reduction in the Fed’s securities holdings.

Will a temporarily reduced “public sector” drag allow broad money growth to recover into H2?

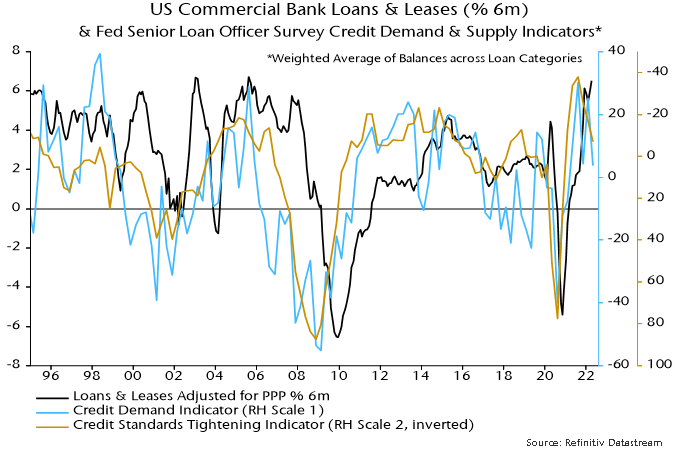

The forecast here is that this small positive will be outweighed by a slowdown in bank lending. Corporate credit demand has been boosted by inventory financing but the stockbuilding cycle is now entering a downswing. Higher mortgage rates will cool demand for real estate loans, while banks may rein back on consumer lending as economic prospects deteriorate.

The suggestion of a lending slowdown is supported by the April Fed senior loan officer survey: the aggregate credit demand indicator fell sharply while the net percentage of banks tightening loan standards rose for a third successive quarter – chart 3.

Chart 3

*”M2+” = M2 + large time deposits at commercial banks + institutional money funds. M2 = currency + demand deposits + other liquid deposits + small time deposits + retail money funds. April estimated.

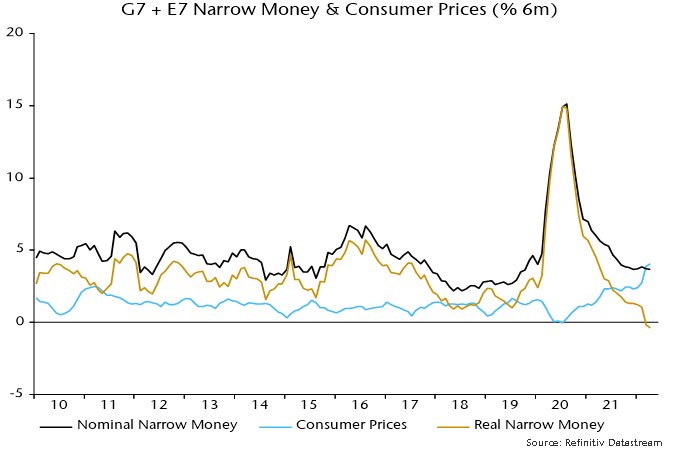

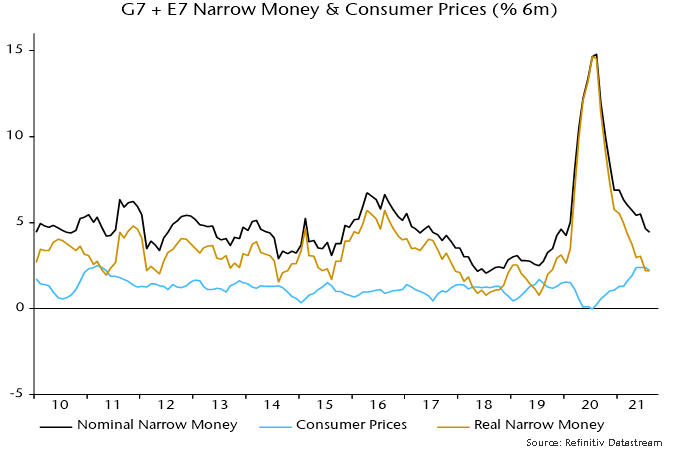

Global* six-month real narrow money momentum turned negative in March and is estimated to have fallen slightly further in April, based on monetary and CPI data covering two-thirds and 90% of the aggregate respectively – see chart 1.

Chart 1

Current weakness is more pronounced than before the 2001 recession and almost on a par with early 2008 before the escalation of the financial crisis.

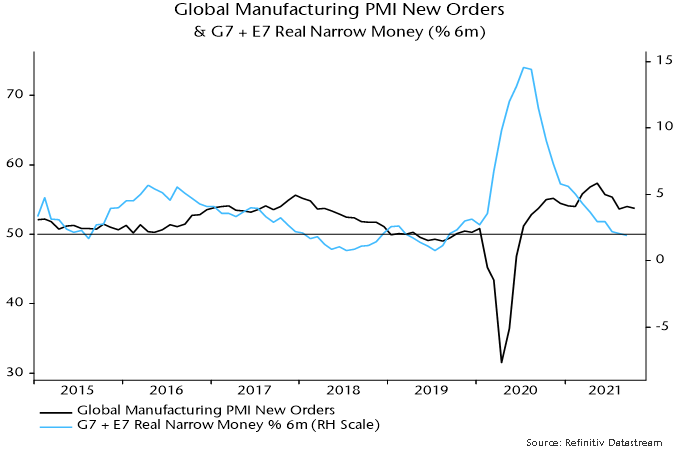

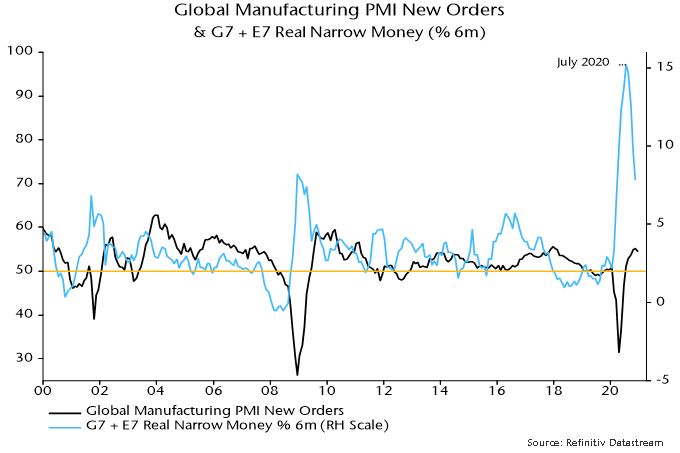

The leading relationship with the global manufacturing PMI new orders index suggests a sizeable further decline in the latter with no recovery before Q4. A move below 45 would confirm a recession.

The further fall in real narrow money momentum in April reflected another rise in global six-month CPI inflation, with small CPI slowdowns in the US and Eurozone more than offset by pick-ups in China, Japan (Tokyo data) and the UK (estimated), among others – chart 2.

Chart 2

Six-month nominal narrow money growth has been moving sideways since December. With CPI inflation probably peaking, real money momentum could be bottoming. Any recovery, however, could be limited by a renewed nominal money slowdown as central bank policy tightening proceeds.

*G7 plus E7. E7 defined here as BRIC plus Korea, Mexico and Taiwan.

Additional monetary data confirm an earlier estimate here that global (i.e. G7 plus E7) six-month real narrow money growth fell slightly further in September, reaching its lowest level since August 2019 – chart 1. Allowing for the usual lead, the suggestion is that global industrial demand momentum – proxied by the manufacturing PMI new orders index – will weaken into end-Q1 2022 and possibly beyond.

Chart 1

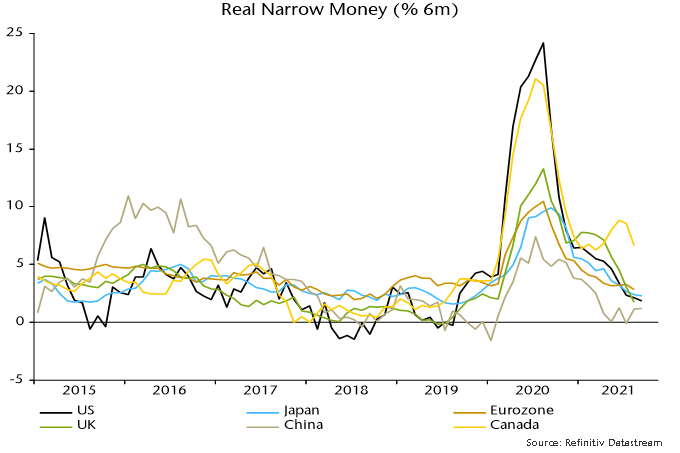

Real narrow money is growing at a similar pace in the US, Japan, Eurozone and UK, i.e. there is no longer a monetary case for expecting superior US economic and asset price performance – chart 2.

Chart 2

Real narrow money growth remains relatively strong in Canada (one month behind), Australia and Sweden. Economic and / or inflation data have been surprising positively in all three cases, triggering policy shifts by the BoC and RBA – will the currently dovish Riksbank be next to capitulate?

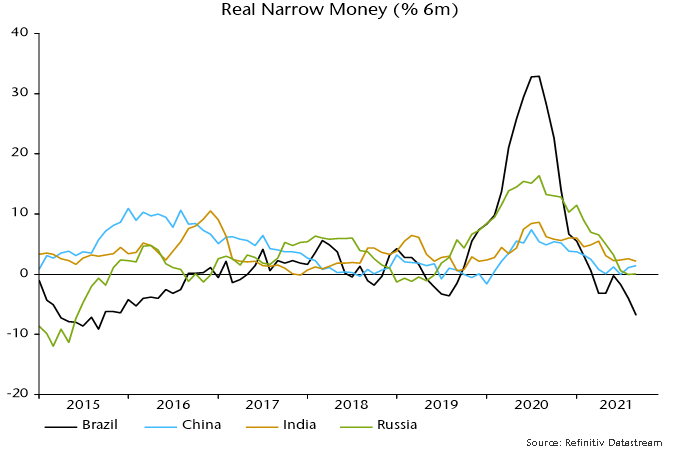

Real money growth remains lower in the E7 than the G7, partly reflecting drags from Russia and Brazil, where monetary policies may have been tightened excessively – charts 3 and 4.

Chart 3

Chart 4

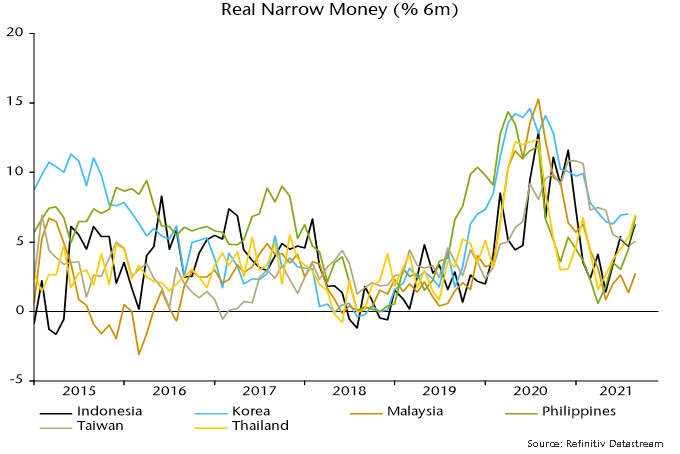

Money trends are perkier in EM Far East economies. Real narrow money growth remains relatively strong in Korea / Taiwan and has ticked up recently, while there have been notable rebounds in Indonesia, the Philippines and Thailand, partly reflecting reopenings – chart 5.

Chart 5

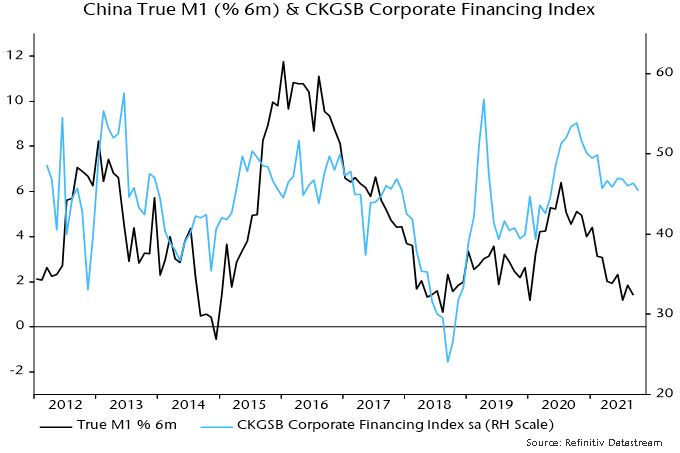

Will China be next? The worry has been that Evergrande fallout would lead to a tightening of credit conditions, aborting an incipient recovery in money growth due to modest policy easing since Q2. The October Cheung Kong business survey was hopeful in this regard: the corporate financing index (a gauge of ease of access to external funds) fell slightly but remains at a normal level – chart 6.

Chart 6

Monetarists have a straightforward response to the ongoing debate about whether global inflation is shifting to a permanently higher level: it won’t if global broad money growth reverts to its pre-covid norm.

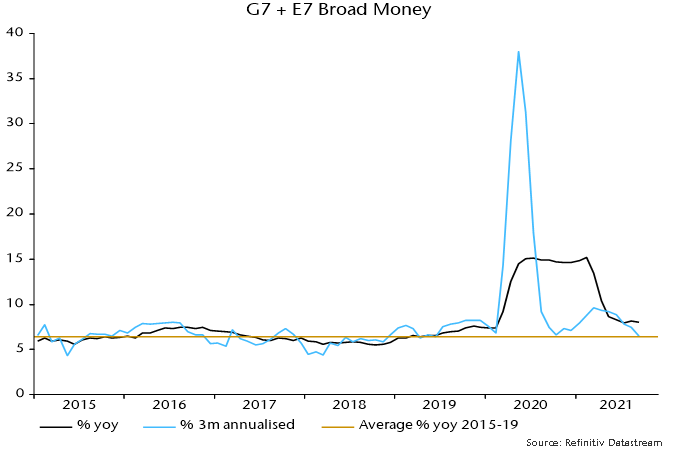

While annual growth remains elevated, G7 plus E7 nominal broad money expanded at a 6.5% annualised rate in the three months to September, in line with the 2015-19 average – chart 7. Central banks won’t need to raise interest rates by much to contain inflation if this pace is sustained.

Chart 7

Money growth has slowed despite ongoing QE, suggesting a risk of an undershoot as these programmes wind down. The more likely scenario, however, is that a pick-up in bank lending provides offsetting support.

US commercial bank loan growth continues to firm, with the recovery underappreciated because of the distorting effect on headline data of PPP loan forgiveness – chart 8. The July Fed senior loan officer survey had signalled stronger credit demand; an October survey is due shortly.

Chart 8

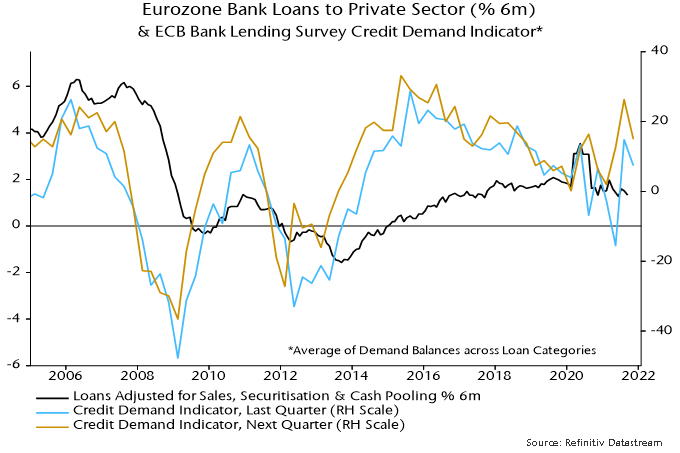

The corresponding ECB survey has already been released and showed a pull-back in credit demand indicators, although they remain in hopeful territory – chart 9. Actual loan growth, however, has remained modest / stable.

Chart 9

Investors appear to be in more optimistic mood about economic prospects, judging from recent relative strength of equities versus bonds and cyclical versus defensive sectors.

This revival of cyclical optimism is not supported by monetary trends. Global six-month real narrow money growth is estimated to have fallen slightly further in September, having reached a 22-month low in July and moved sideways in August – see chart 1. (The September estimate is based on monetary data covering 70% of the aggregate and near-complete inflation data.)

Chart 1

The fall in real money growth into July was the basis for a forecast here that global industrial demand momentum – proxied by the manufacturing PMI new orders index – would slow further into early 2022. The weak September reading, if confirmed, suggests that the slowdown will extend through end-Q1.

The rise in cyclical optimism is not attributable to policy news: the US spending bills remain stalled in Congress and more central banks are signalling hawkishly. PBoC officials last week played down the prospect of policy easing despite weak economic data.

The most likely explanation for the cyclical rally is growing evidence that supply chain blockages are easing. The global manufacturing PMI suppliers’ delivery times index bottomed in June / July, recovering marginally in August / September (lower readings = longer delivery times). October flash reports this week may show a further increase.

Industrial output momentum will rebound as sectors hobbled by supply constraints – autos in particular – normalise production. This pick-up, however, will be short-lived if demand growth continues to slow, as suggested by monetary trends.

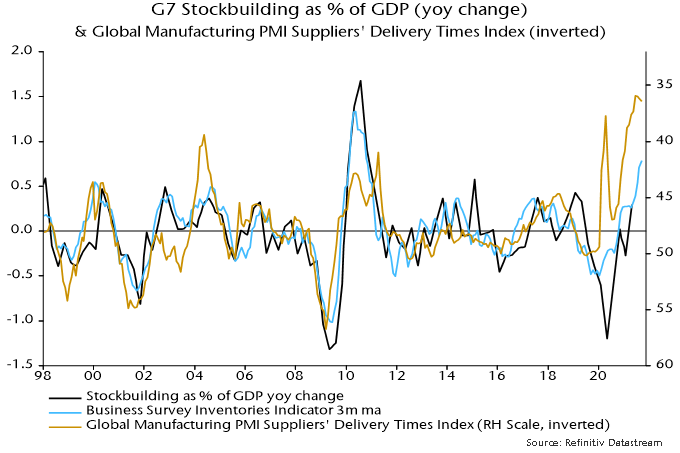

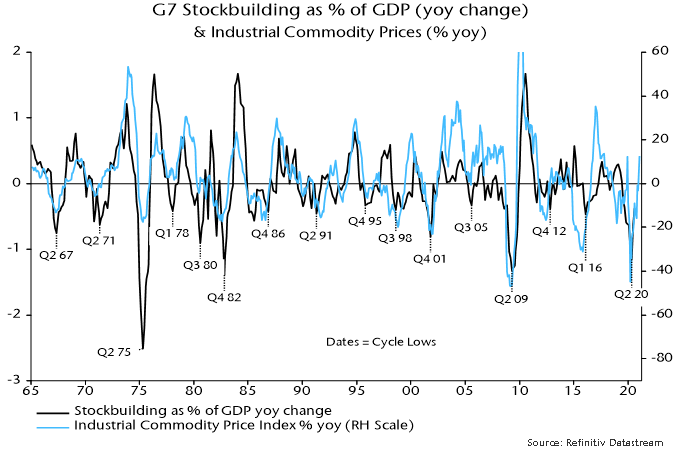

The easing of supply pressures, moreover, carries its own warning for demand prospects. The PMI delivery times index is inversely correlated with the rate of change of G7 stockbuilding – chart 2. Recent long delivery delays reflect not only pandemic-related disruption but also a scramble to boost inventories following intense destocking. The easing of blockages, therefore, is indirect evidence that the demand growth boost from the stockbuilding cycle is at or near a peak.

Chart 2

The global six-month real narrow money growth estimate for September incorporates further falls in the US / Japan and a stable Chinese reading – chart 3. The US / China gap – which surged last year, warning of divergent economic / equity market prospects – has almost closed. Eurozone and UK September monetary data will be released on 27 and 29 October respectively. Canadian numbers appear with a one-month lag: real money growth remained relatively strong in August (just released), suggesting that the Bank of Canada will be under pressure to hike rates soon.

Chart 3

The forecasting approach employed here – relying on monetary and cycle analysis – turned positive on the global economy and risk markets in early Q2 2020 but is giving a more cautionary message at the start of 2021. The suggestion is that underlying economic momentum will slow temporarily while monetary support for markets has diminished, together raising the risk of a correction. The central view remains that global growth will be strong over the course of 2021 as a whole but with the adverse corollary of a significant pick-up in inflation into 2022.

The monetary aspect of the forecasting approach can be summarised as “real money leads the economy while excess money drives markets”. Six-month growth of real (i.e. inflation-adjusted) narrow money in the G7 economies and seven large emerging economies (the “E7”) was weak at the start of 2020 but surged from March, correctly signalling a strong rebound in global economic activity during H2.

Real money growth, however, peaked in July, falling steadily through November, the latest data point – see chart 1. Turning points in real money growth have led turning points in the global manufacturing PMI new orders index – a key coincident indicator – by 6-7 months on average historically, suggesting that the PMI will move lower in early 2021. The level of money growth remains high, arguing against economic weakness (except due to “lockdowns”), but a directional shift in activity momentum could act as a near-term drag on cyclical assets.

Chart 1

“Excess” money refers to an environment in which actual real money growth exceeds the level required to support economic expansion, with the surplus likely to be invested in markets. Two gauges of excess money are monitored here: the gap between six-month growth rates of G7 plus E7 real narrow money and industrial output, and the deviation of year-on-year real money growth from a long-run moving average. Historically, global equities performed best on average when both measures were positive, worst when they were negative, and were lacklustre when they gave conflicting signals.

Following a joint positive signal (allowing for data release lags) at end-April 2020, the measures became conflicting again at end-December – year-on-year real money growth remains well above its long-run average but six-month growth fell below that of industrial output in October / November. Markets, therefore, may no longer enjoy a monetary “cushion” against unfavourable news, including the expected PMI roll-over.

The expectation here is that markets will become more volatile but risk assets are unlikely to be outright weak – any sizeable set-back would probably represent another buying opportunity. As noted, real money growth remains at an expansionary level and may stabilise soon, while the cycle analysis is giving a positive economic message for the next 12+ months, as explained below.

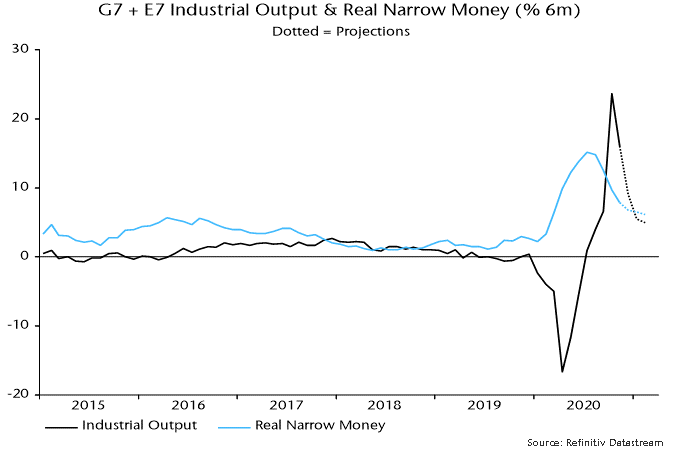

The cross-over of six-month real narrow money growth below industrial output growth, moreover, could prove short-lived, with output momentum about to fall back sharply as positive base effects fade. Assuming a stabilisation of monthly money growth, a positive differential could be restored as early as January – see chart 2 – in which case the assessment of the monetary backdrop for markets would shift back to favourable from Q2.

Chart 2

The cycle analysis provides a medium-term perspective and acts as a cross-check of the monetary analysis. There are three key economic activity cycles: the stockbuilding or inventory cycle, which averages 3.5 years (i.e. from low to low); a 9-year business investment cycle; and a longer-term housing cycle averaging 18 years. These cycles are essentially global in nature although housing cycles in individual countries can sometimes become desynchronised.

The cycle analysis was cautionary at the start of 2020, reflecting a judgement that the stockbuilding and business investment cycles were in downswings that might not complete until mid-year. The covid shock magnified but ended these downswings, with both cycles bottoming in Q2 and entering a recovery phase in H2. With the housing cycle still in an upswing from a 2009 low, all three cycles are now acting to lift global economic momentum.

The next scheduled cycle trough is a low in the stockbuilding cycle, due to be reached in late 2023 if the current cycle conforms to the average 3.5 year length. The downswing into this low would probably start about 18 months earlier, i.e. around Q2 2022. The cycle analysis, therefore, is giving an “all-clear” signal for the global economy for the next 15-18 months, implying that any data weakness – such as suggested by monetary trends for early 2021 – is likely to be minor and temporary.

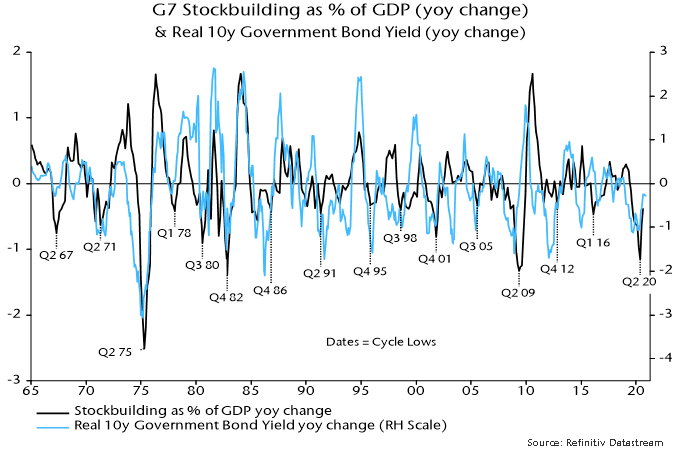

Financial market behaviour is strongly correlated with the stockbuilding cycle in particular. Cycle upswings are usually associated with rising real government bond yields and strong commodity markets – see charts 3 and 4 – as well as low / falling credit spreads and outperformance of cyclical equity sectors. The latter three of these trends, of course, were in place during H2 2020 and may extend during 2021 after a possible Q1 correction. A surprise to the consensus in 2021 could be a rebound in real bond yields, which would challenge current equity market valuations and could favour “value”.

Chart 3

Chart 4

To sum up, monetary data in early 2021 will be important for the strategy assessment here. The current monetary backdrop and possible weaker near-term economic data suggest reducing cyclical exposure relative to H2 2020 but a stabilisation or revival in real money growth would support the positive message from the cycle analysis, arguing for using any setback in cyclical markets to rebuild positions in anticipation of a strong H2.

Consumer price inflation rates are widely expected to rise during H1 2021, reflecting recent commodity price strength, a reversal of temporary tax cuts (Germany / UK) or subsidies (Japan), and base effects. The policy-maker and market consensus is that this will represent a temporary “cyclical” move of the sort experienced regularly in recent decades. The suspicion here is that it will prove more lasting and significant, because the monetary backdrop is much more expansionary / inflationary than before those prior run-ups.

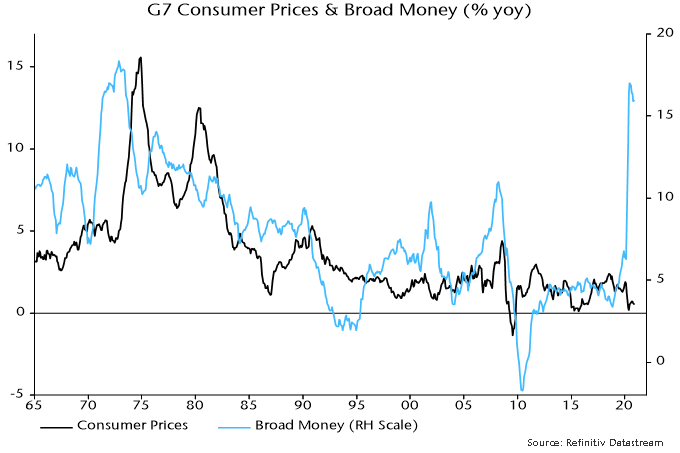

Broad rather than narrow money trends are key for assessing medium-term inflation prospects. This is illustrated by Japan’s post-bubble experience: narrow money has grown strongly on occasions but annual broad money expansion never rose above 5% over 1992-2019, averaging just 2.1% – the monetary basis for sustained low inflation / mild deflation. Similarly, G7 annual broad money growth averaged only 3.7% in the post-GFC decade (i.e. 2010-19).

2020 may have marked a transformational break in monetary trends. G7 annual broad money growth peaked at 17.0% in June, the fastest since 1973 – see chart 5. Monthly growth has subsided but there has been no “payback” of the H1 surge. At the very least, this suggests a larger-than-normal “cyclical” upswing in inflation in 2021-22. Ongoing monetary financing of large fiscal deficits may sustain broad money growth at well above its levels of recent decades, embedding the inflation shift.

Chart 5

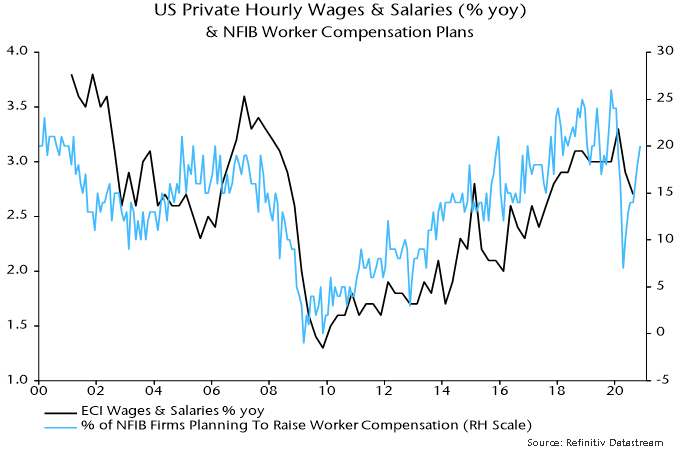

The consensus view that an inflation pick-up will prove temporary rests on weak labour markets bearing down on wage growth. Unemployment rates adjusted for short-time working / furlough schemes, however, fell sharply as the global economy rebounded in H2 2020 and structural rates have probably risen – labour market “slack”, therefore, may be less than widely thought and much lower than after the 2008-09 recession. The slowdown in wages to date has been modest and some business surveys are already hinting at a rebound – see chart 6.

Chart 6

Commentators who take seriously the prospect of a sustained inflation rise often argue that real bond yields would take the strain by moving deeper into negative territory, the view being that central banks will cap nominal yields. Such a scenario would be bullish for risk assets but probably overstates the power of the policy emperors. Pegged official rates and a QE flow currently running at about 10% of the (rapidly rising) outstanding stock of G7 government bonds per annum could prove insufficient to offset selling by existing holders in the event of an unexpected inflation surge.

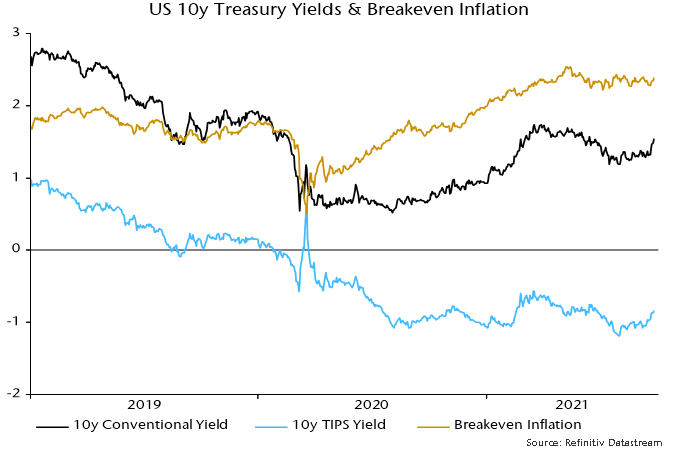

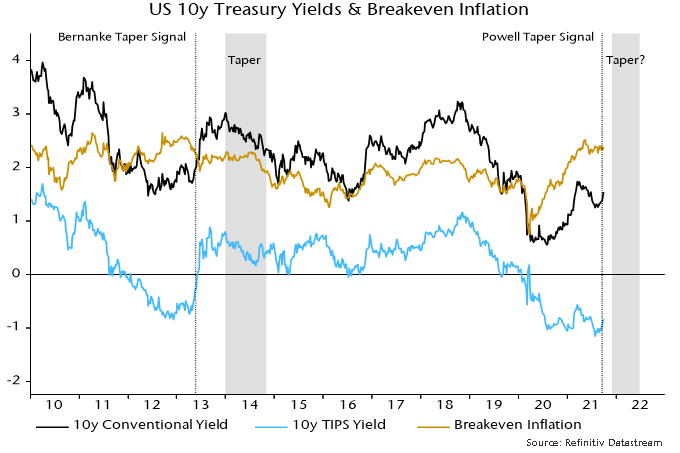

US Treasury yields have risen sharply since Fed Chair Powell’s signal last week of a likely tapering decision at the November or December FOMC meeting. The move higher mainly reflects an increase in real yields, with inflation break-evens range-bound – see chart 1.

Chart 1

The reaction recalls a surge in nominal and real yields when former Chair Bernanke signalled that the Fed was considering tapering in Congressional testimony on 21 May 2013. Inflation breakevens, which had been falling into the announcement, declined further before recovering – chart 2.

Chart 2

Bernanke’s signal was a catalyst for real yields – which had reached negative levels similar to recently – to return to positive territory. The yield surge triggered a short-lived “risk-off” move in markets, focused on emerging markets and credit (the “taper tantrum”).

The market response spooked the Fed, causing the taper decision to be delayed until December 2013. When tapering finally started in January 2014, nominal and real yields embarked on a sustained decline. Inflation breakevens moved sideways but also fell later in 2014.

Cyclical sectors of equity markets outperformed defensive sectors between Bernanke’s May announcement and the start of tapering in January.

The view here, though, is that investors should be cautious about drawing parallels between 2013-14 and now.

The economic backdrop is a key difference. The global manufacturing PMI new orders index was about to embark on a significant rise as Bernanke gave his taper signal in May 2013 – chart 3. So it is difficult to disentangle the taper effect on yields from the usual correlation with cyclical momentum.

Chart 3

Economic momentum is slowing currently, with money trends suggesting a further PMI decline into early 2022.

This suggests that 1) the yield increase won’t mirror 2013 because the taper announcement effect is offset by a weakening cyclical backdrop, and 2) any rise in real yields could be dangerous for cyclical assets because – in contrast to 2013 – a higher discount rate is unlikely to be balanced by positive economic / earnings news.

Partial data indicate that global six-month real narrow money growth was little changed in August, following July’s fall to a 22-month low. Allowing for the usual lead, the suggestion is that the global economy will continue to lose momentum into early 2022, with no reacceleration before late Q1 at the earliest.

Global PMI results for August were consistent with the slowdown forecast, with the manufacturing new orders index falling for a third month – see chart 1.

Chart 1

The US ISM manufacturing new orders index unexpectedly rose in August but this appears to have been driven by a rise in inventories: the new orders / inventories differential, which often leads, fell to its lowest since January – chart 2.

Chart 2

The US, China, Japan, Brazil and India have released monetary information for August, together accounting for 70% of the G7 plus E7 aggregate calculated here*. CPI data are available for all countries bar the UK and Canada.

The stability of six-month real narrow money growth in August conceals a further slowdown in nominal money expansion offset by a small decline in CPI momentum – chart 3.

Chart 3

Previous posts discussed the possibility that real money growth would rebound during H2 2021, warranting optimism about economic prospects for 2022 and supporting another leg of the “reflation trade”. The monetary data have yet to validate this scenario.

The real money growth rebound scenario depended importantly on a pick-up in China in response to recent and prospective policy easing. Chinese six-month real narrow money growth does appear to have risen slightly in August** but there were offsetting declines in the US, Japan and Brazil – chart 4.

Chart 4

*The US number is estimated from weekly data on currency in circulation and commercial bank deposits. **The household demand deposit component is estimated pending release of full data.