À l’échelle mondiale, les investisseurs ont adopté les actions mondiales à petite capitalisation comme source de diversification boursière. Malgré son nom, cet univers se compose en grande partie de sociétés dont la capitalisation boursière est supérieure à un milliard de dollars américains et il comprend un nombre croissant de titres bien connus dans de nombreux marchés locaux et dont certains jouissent d’une notoriété de marque mondiale.

Principaux avantages des petites capitalisations mondiales

| Moins petites qu’on ne le croit | Plus de 2 600 sociétés mondiales à petite capitalisation ont une capitalisation boursière supérieure à 1 G$ US |

|---|---|

| Ampleur et profondeur | Le titre le plus important ne représente que 0,2 % de l’indice et la diversification sectorielle est supérieure à celle des autres grands indices |

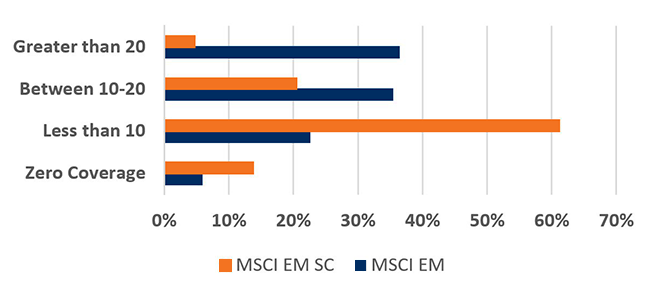

| Occasions d’alpha | Les marchés mondiaux d’actions à petite capitalisation sont moins prisés par les analystes de recherche que les marchés boursiers développés à grande capitalisation, de sorte que les recherches indépendantes menées par des gestionnaires actifs ouvrent la voie à des possibilités de valeur ajoutée. |

L’univers des petites capitalisations

Les actions mondiales à petite capitalisation offrent aux investisseurs la possibilité de profiter d’un éventail d’occasions incomparable. L’indice MSCI Monde à petite capitalisation regroupe des sociétés à petite capitalisation de 23 pays développés. Comparativement aux titres canadiens, les occasions mondiales à petites capitalisations ne sont pas si petites. Au 31 décembre 2022, 2 643 sociétés affichaient une capitalisation boursière supérieure à 1 G$ US. L’indice composé S&P/TSX ne comptait que 209 sociétés de cette envergure.

La part du titre le plus important au sein de l’indice mondial des petites capitalisations n’est que 0,2 %. En revanche, le titre le plus important de l’indice composé S&P/TSX à la fin de 2022 représentait 6,3 % de l’indice.

De plus, les 15 actions les plus importantes de l’indice du marché boursier canadien constituaient 45 % de l’indice, tandis que les 15 titres les plus importants de l’indice mondial des actions à petite capitalisation en représentent moins de 3 %. Il faudrait que les 627 titres les plus importants atteignent une pondération indicielle de 45 % au sein de l’indice mondial des titres à petite capitalisation, ce qui met en évidence l’éventail beaucoup plus vaste des occasions de placement offertes par l’univers des titres mondiaux à petite capitalisation.

Les sociétés mondiales à petite capitalisation sont généralement bien connues sur leur marché local et certaines jouissent d’une notoriété de marque mondiale. Par exemple : L’Occitane, le fabricant, distributeur et détaillant de produits de soins de la peau et de beauté naturels et biologiques; Samsonite, la plus connue et la plus grande société de bagages de voyage au monde; IWG, qui offre des solutions d’espaces de travail à court terme (et à long terme) partout dans le monde; ainsi que des marques bien connues comme Regus.

Les avantages que comportent les actions mondiales à petite capitalisation au chapitre de la diversification vont au-delà des titres individuels. Tandis que les secteurs de la finance, de l’énergie et des matériaux dominent les principaux indices canadiens (voir la figure 1), les marchés des actions mondiales à petite capitalisation offrent une meilleure représentation sectorielle. De fait, les secteurs de la consommation discrétionnaire (p. ex., sociétés de restauration, de produits de luxe et de voyage) et de la santé y occupent une place plus importante.

Figure 1 – Avantages de la diversification que procure le marché des petites capitalisations

| Indice MSCI Monde à petite capitalisation (%) | Indice composé S&P/TSX (%) | |

| Énergie | 5,0 | 18,1 |

| Matériaux | 7,6 | 12,0 |

| Industrie | 19,4 | 13,3 |

| Consommation discrétionnaire | 12,5 | 3,7 |

| Biens de consommation de base | 4,7 | 4,2 |

| Soins de santé | 10,7 | 0,4 |

| Finance | 14,3 | 30,8 |

| Technologies de l’information | 10,8 | 5,7 |

| Services de communication | 2,8 | 4,9 |

| Services aux collectivités | 3,2 | 4,4 |

| Immobilier | 8,9 | 2,6 |

| Total | 100 | 100 |

Sources : MSCI et Thomson Reuters Datastream. Données au 31 décembre 2022

Au cours des 10 dernières années, l’indice des actions mondiales à petite capitalisation a enregistré le meilleur rendement, mais avec une volatilité plus élevée (figure 2). Comme pour tous les marchés, il est important de comprendre les risques de placement.

Figure 2 – Risque et rendement sur une période de 10 ans (terminée le 31 décembre 2022)

Sources : MSCI et Thomson Reuters Datastream. Remarque : Les rendements des indices sont exprimés en dollars canadiens.

Comprendre les risques

Bien que les gestionnaires actifs puissent atténuer les risques grâce à leurs recherches et à une sélection minutieuse de titres, pour ce qui est des titres mondiaux à petite capitalisation, les investisseurs doivent tenir compte de ce qui suit :

- Risque de liquidité : Il faut parfois plus de temps pour négocier une action à petite capitalisation qu’une action à grande capitalisation.

- Manque d’information : Même si la propriété plus élevée des initiés, associée aux actions mondiales à petite capitalisation, s’arrime aux intérêts des investisseurs, il peut en résulter un manque de transparence et d’information, ce qui n’est pas le cas des placements dans les actions mondiales à grande capitalisation.

- Accès au crédit : Les petites sociétés n’ont pas le même accès aux marchés du crédit que les grandes entreprises, ce qui peut parfois limiter leur capacité à réaliser leur potentiel.

Reconnaître les avantages potentiels

Voici quelques avantages potentiels des petites capitalisations mondiales qui permettent de compenser les risques :

- Potentiel de croissance : Les investisseurs qui sont en mesure de repérer la prochaine génération de petites sociétés qui connaissent une croissance rapide et qui deviennent de grandes sociétés seront largement récompensés.

- Meilleure harmonisation des intérêts : En règle générale, les sociétés mondiales à petite capitalisation exercent leurs activités dans des secteurs plus spécialisés et les initiés y détiennent une participation plus élevée, de telle sorte que les propriétaires et les actionnaires partagent les mêmes intérêts.

- Potentiel de diversification sectorielle : Les investisseurs peuvent profiter de la meilleure représentation des secteurs de la consommation discrétionnaire et de la santé qu’offre l’indice des actions mondiales à petite capitalisation. Par exemple, les habitudes de consommation indiquent que le secteur de la consommation discrétionnaire devrait bien se comporter à long terme. Le secteur de la santé devrait également profiter du vieillissement de la population dans les pays développés.

- Occasion de valeur ajoutée : Les analystes externes ne font pas autant de recherches sur les sociétés à petite capitalisation. Par conséquent, les gestionnaires qui privilégient une gestion active ont une meilleure chance de surpasser l’indice de référence lorsqu’ils repèrent des actions dont le cours ne reflète pas pleinement leur valeur intrinsèque ou leur potentiel de croissance. Selon la base de données d’eVestment, 71 % des gestionnaires de l’univers des actions mondiales à petite capitalisation à gestion active ont surpassé l’indice MSCI Monde à petite capitalisation au cours de la période de cinq ans terminée le 31 décembre 2022.

- Occasion de contrebalancer les effets du style : À la fin de 2022, plus de 4 425 sociétés faisaient partie de l’indice MSCI Monde à petite capitalisation. L’ensemble plus vaste d’occasions a donné lieu à un nombre accru de stratégies mondiales à petite capitalisation offertes par des gestionnaires de placements systématiques (quantitatifs). Grâce à une approche systématique, un gestionnaire de placement est en mesure de profiter d’une étendue de connaissances à l’égard d’un vaste univers de sociétés, comparativement à la portée des connaissances associées aux gestionnaires fondamentaux, qui se concentrent sur la sélection d’un plus petit nombre de sociétés dans lesquelles investir. Pour ce qui est des autres marchés boursiers, les investisseurs qui peuvent intégrer plusieurs gestionnaires dans une catégorie d’actif peuvent profiter des styles systématiques et fondamentaux complémentaires.

Pourquoi investir dans les actions mondiales à petite capitalisation

Ces dernières années, la concentration de l’indice des actions mondiales à grande capitalisation des marchés développés a augmenté. L’intégration d’une composante d’actions mondiales à petite capitalisation dans les portefeuilles peut offrir une source de diversification complémentaire, un plus vaste éventail d’occasions de sociétés faisant l’objet de moins de recherche à l’externe, et par conséquent offrir la possibilité de dégager des rendements supérieurs à ceux de l’indice au moyen d’une gestion active.