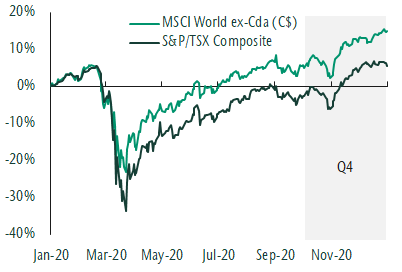

Markets overview

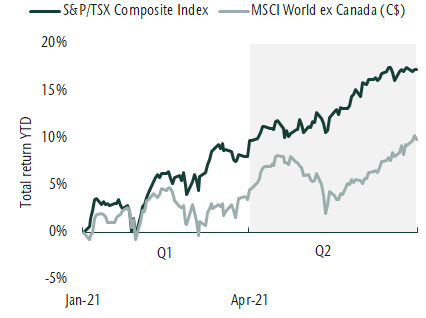

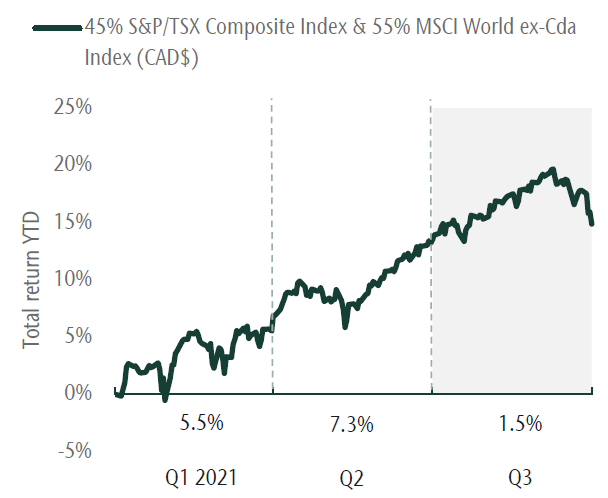

The economic recovery from the pandemic has been strong and more enthusiastic than expected. There is a surge in demand for goods which is contributing to supply shortages and rising inflation. Given the backdrop, policymakers are beginning to reduce the emergency level stimulus that was put in place. The equity market response has been more volatility and lower returns than earlier in the recovery. This is expected given the outlook for more moderate growth and less support from central banks. On the quarter the S&P/TSX Composite Index was up 0.2% and the MSCI World ex Canada (C$) advanced 2.5%. Year to date this brings these market returns to 17.5% and 12.6%, respectively.

More moderate equity returns in Q3

Source: MSCI, Refinitiv

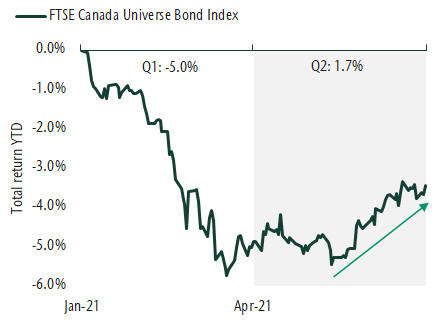

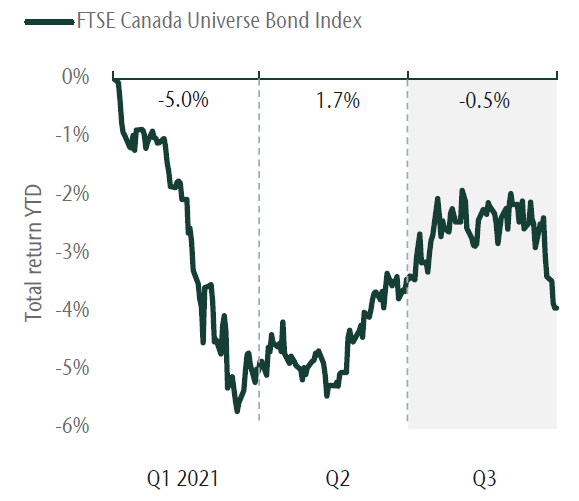

Bonds produced negative returns this quarter and year as yields were affected by both a surge in growth earlier in the year and recent changes to central bank policy. The FTSE Canada Universe Bond Index was down -0.5% for the quarter and down -4.0% for the year. High yield and short bonds, which are less sensitive to changes in yield, generated positive returns.

Bond returns remain negative

Source: FTSE, Refinitiv

Portfolio strategy

Our view is that we are experiencing a strong economic recovery supported by a broadening global restart. At the same time we expect higher inflation and a more muted monetary response going forward. We maintain an overweight to equities but recognize risks are rising. As equity market performance has been strong, we have taken profits. Within equities, we have an overweight to small-cap stocks which will benefit from above trend growth. Within bonds, we have been increasing our high yield exposure which is more attractive than core bonds given their low expected return.

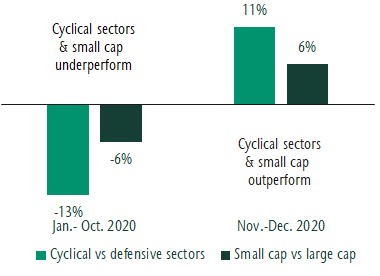

Our portfolio management teams continue to favour more cyclical companies that are levered to the economic recovery. However, given the outlook for slower economic growth, inflation and supply bottlenecks, we are adding companies that can generate strong earnings despite these headwinds. Within fixed income, we have taken profits by reducing exposure to the corporate sector as well as real return bonds that have benefited significantly from higher inflation. Our positioning in portfolios has served clients well and remains attractive as we move into the final quarter of the year.

From the desk of Jeff Guise, Managing Director, Chief Investment Officer, CC&L Private Capital.

This post is for information only and is not intended as investment advice. The views expressed are those of the author at the time of publication and are subject to change at any time.