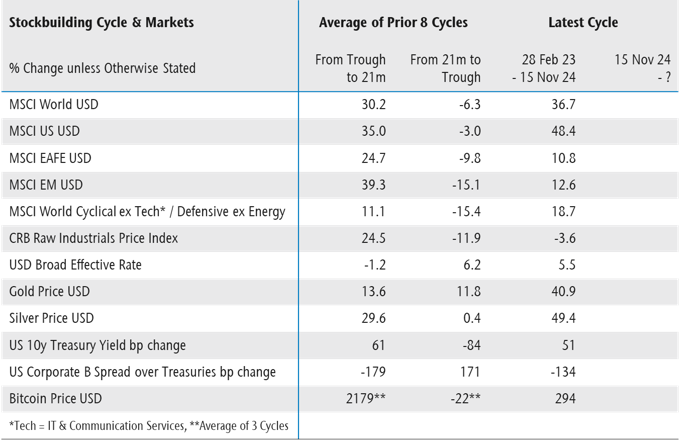

November results confirm a September low in global manufacturing PMI new orders, with money trends suggesting a further rise through spring 2025, subject to tariff distortions.

The baseline scenario described in previous posts was that global industrial momentum – proxied by the manufacturing PMI new orders index – would bottom out in late 2024 and recover weakly into H1 2025. A manufacturing upturn was expected to be offset by loss of services momentum, with associated labour market weakness combining with favourable inflation news to support faster monetary policy easing.

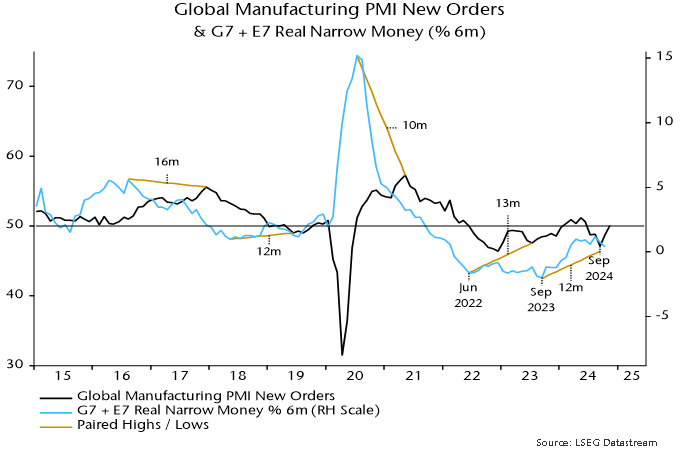

The manufacturing part of the story is on track. The forecast of a late 2024 PMI new orders low was based on a recovery in global six-month real narrow money momentum from a trough in September 2023, taking into account a recent average interval of about a year between turning points in the two series. The new orders index reached a 22-month low on schedule in September, recovering solidly in October / November – see chart 1.

Chart 1

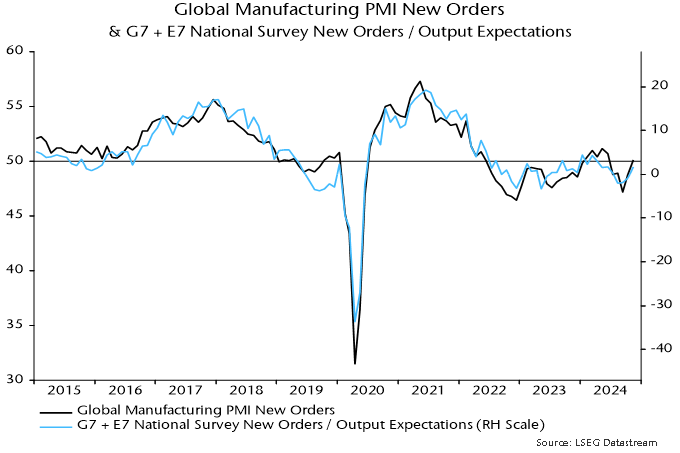

The turnaround has been mirrored by an alternative indicator based on national business surveys, although this bottomed one month earlier in August and has recovered by slightly less – chart 2.

Chart 2

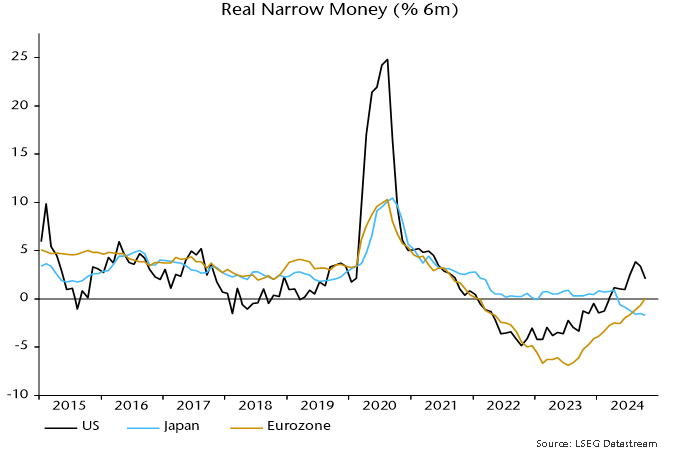

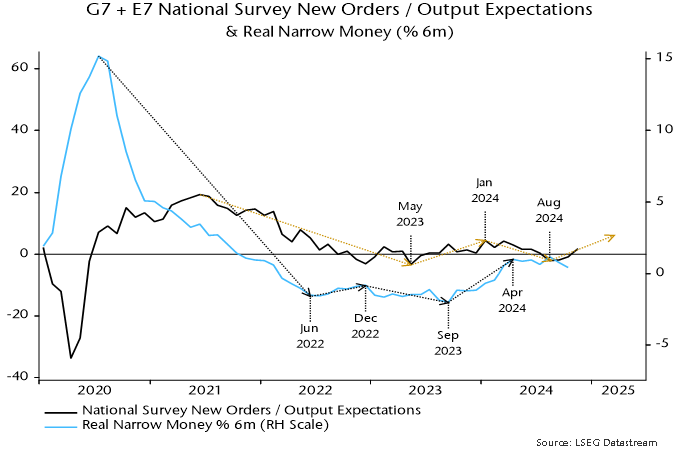

Chart 3 highlights the recent relationship between swings in six-month real narrow money momentum and directional changes in the alternative indicator. Real money momentum recovered between September 2023 and April 2024 but has since stalled at a weak level by historical standards, falling back in September / October.

Chart 3

Assuming that the lead time remains at about a year, the suggestion is that a rise in the survey indicator / PMI new orders will level off in spring 2025, falling short of prior historical peaks.

Forecast uncertainty is higher than normal because tariff threats are distorting behaviour. Accelerated stockbuilding could result in a stronger near-term pick-up and earlier peak with a subsequent normalisation – or worse if threats crystallise.