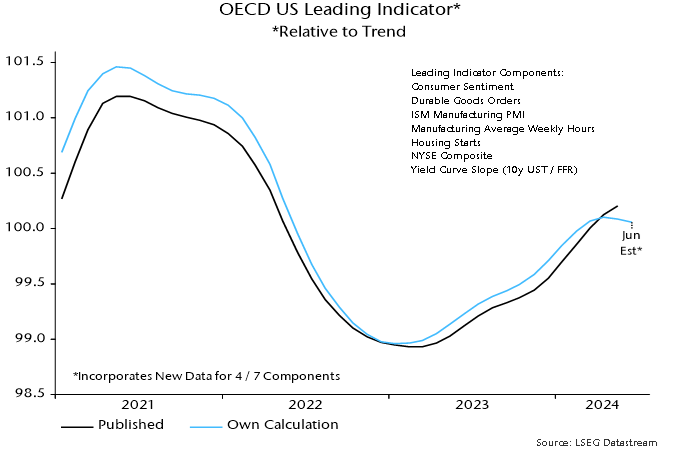

A recovery in the OECD’s US composite leading indicator could be reversing, in which case recent underperformance of cyclical equity market sectors versus defensives could extend.

The OECD indicator receives less attention than the Conference Board US leading economic index but its historical performance compares favourably.

The correlation coefficient of six-month rates of change is maximised with a two-month lag on the OECD indicator, i.e. the OECD measure slightly leads the Conference Board index.

The OECD indicator recovered from early 2023, signalling that recession risk was (temporarily?) receding. The Conference Board index continued to weaken, although the rate of decline slowed.

The latest published numbers show the OECD measure still rising in May. New information, however, is available for four of the seven components. An updated calculation suggests that the indicator peaked in April, with small declines in May and June – see chart 1.

Chart 1

A firmer indication will be available at the end of next week, following release of data on the remaining three components – durable goods orders, the ISM manufacturing PMI and manufacturing average weekly hours.

The suggested stall in the OECD leading indicator recovery has coincided with larger month-on-month declines in the Conference Board measure in April and May.

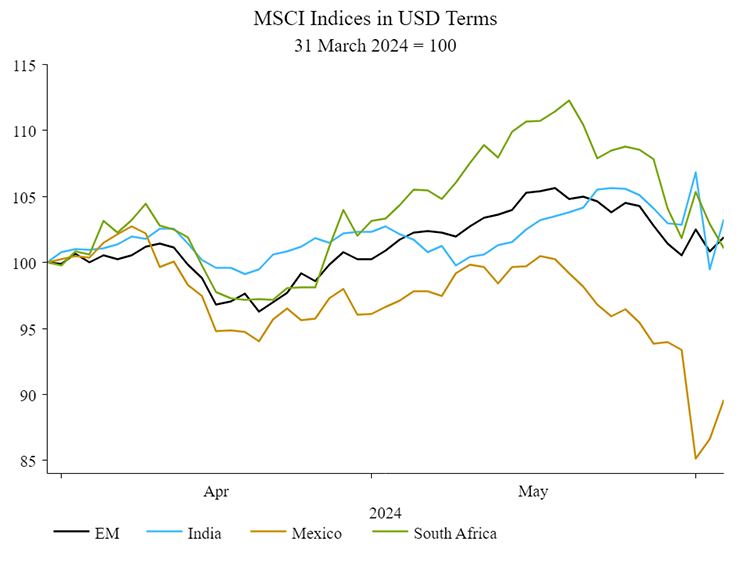

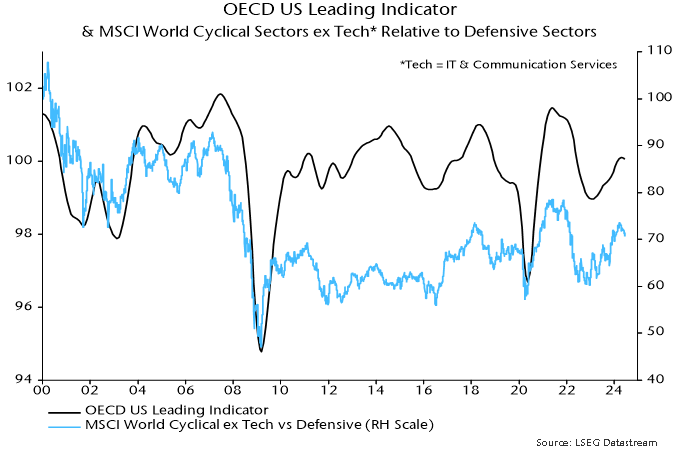

The price relative of MSCI World cyclical sectors, excluding tech, versus defensive sectors has mirrored movements in the OECD US leading indicator historically – chart 2. A rally in the relative peaked in late March, consistent with the suggestion of an April leading indicator top.

Chart 2

Source: PitchBook.

Source: PitchBook. Source: Statista.

Source: Statista.