Recent market movements have been driven by a decline in bond yields and a repricing of a more optimistic scenario, where growth is resilient and inflation figures are falling fast. While mid-term trends look supportive, persistently high inflation could point to later interest rate cuts than markets currently expect.

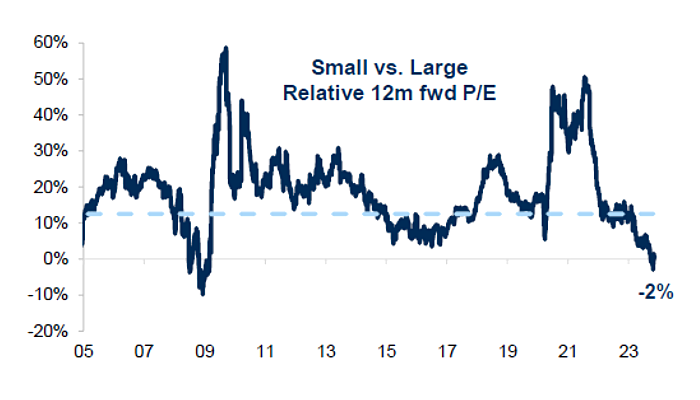

Small caps shine in Europe

We believe that growth will remain steady in 2024 despite potential economic contractions in some regions during the first half of the year. European small caps continue to look attractive compared to their larger counterparts. As illustrated below, small caps are near their largest historical discount relative to large caps. Several industries still trade at very low valuations and could benefit from a potential re-rating. We believe the end of the destocking phase combined with lower interest rates should help in regaining momentum for European small caps.

P/E of STOXX small caps vs STOXX large caps

Source: Goldman Sachs.

Wage growth: a silver lining

Real wage growth is another indicator showing positive signs. An increase in wage growth could be beneficial for consumers and the broader economy. Companies’ responses to growing labour costs will be a key determinant for financial markets in 2024. Companies with strong pricing power should be able to raise prices again. Others might scale back labour, cut investments or accept lower profits. In summary, we expect earnings growth to be erratic and modest in 2024.

Factor investing in a dry liquidity climate

Regarding factor investing, liquidity has dried up in 2023 and small caps are underinvested in compared with other asset classes. According to JP Morgan, small caps in Europe have experienced their worst 23-month outflows in the last 15 years. However, November’s positive inflows may indicate a shift toward a more optimistic sentiment. A return to more normalized monetary policy should gradually improve liquidity and investment flows during 2024. Much like the adage “cash is king,” investors are likely to continue rewarding companies with decent dividends and buybacks.

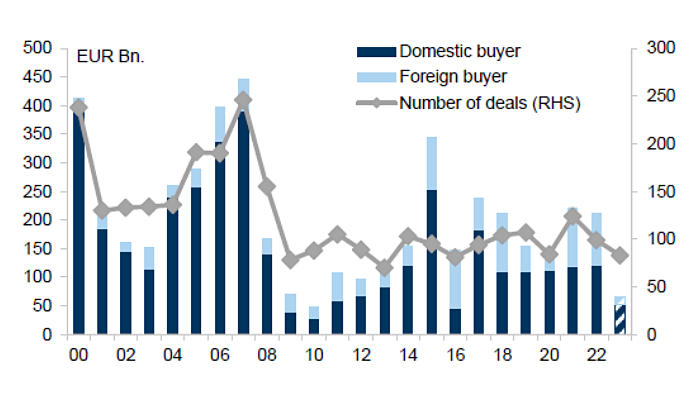

M&A: the untapped potential for small caps

M&A activity is another potential catalyst that would favour smaller companies. M&A in 2023 has been low, as shown by the chart below, with a 70% decrease primarily due to fewer foreign buyers. Corporate sentiment, equity valuations and monetary conditions are key drivers of M&A activity. Reasonable equity valuations along with a normalizing monetary policy should enhance corporate sentiment toward M&A. With positive sentiment and plenty of balance sheet resources, a potential pickup in M&A could greatly benefit smaller companies.

Sources: Goldman Sachs, Bloomberg.

Navigating tomorrow’s market

As small caps gain traction and M&A activity hints at resurgence, the market presents a complex puzzle. The real insight emerges in piecing together these fragments to understand where the next wave of growth will come from.

As winter approaches, homeowners are confronted with the need to turn on their heating systems and the higher costs of additional heating. This winter, many US consumers will likely pay even more to heat their homes because of surging fuel prices and colder weather forecasts.

The National Energy Assistance Directors Association predicts increased winter heating expenditures across the board, with electricity up 1.2%, propane 4.2% and heating oil 8.7%. Natural gas is expected to be down 7.8%. Air conditioning and heating are by far the biggest sources of home energy use, comprising 51% of household energy bills. A main reason energy bills spike in winter is due to inadequate insulation.

This is where Installed Building Products (IBP) comes in – and why we’ve invested in this company. This week, we’ll share insights into our investment process and approach to selecting companies like IBP that we believe are poised to generate shareholder value.

Who is Installed Building Products (IBP)?

Founded in 1977 and based in Columbus, Ohio, IBP is one of the largest insulation installers in the US. In the late 1990s, the company embarked on an ambitious acquisition strategy to expand its reach nationally. IBP went public in 2014, at which point it was generating $432 million in revenue with earnings of 2 cents a share. Last year, its revenue reached $2.6 billion with adjusted earnings of $8.95 per share.

Besides insulation, which makes up 60% of its revenue, IBP has diversified into complementary building products (waterproofing, fireproofing, garage doors, rain gutters and more) for both the residential and commercial construction markets.

Target market

Combined single family and multifamily insulation market has a ~$6 billion total addressable market (TAM).

Complementary products add another $4 billion TAM ($1.4 billion for garage doors, $1.1 billion for shower shelving and mirrors, $800 million for window blinds and $700 million for gutters).

Amount of insulation per home is increasing due to a greater focus on energy efficiency and stricter energy codes.

IBP’s largest competitor is TopBuild (they each rank #1 or #2 in different markets).

IBP has a cost advantage

Industry suppliers lack power. The fiberglass insulation manufacturing industry is highly consolidated, with four players accounting for all sales (Owens Cornings 40%, CertainTeed 20%, Knauf 20%, Johns Manville 20%). While the supplier concentration would suggest high pricing power, insulation manufacturing is a capital-intensive business with high fixed costs. Ovens cannot be easily shut on and off. As a result, manufacturers are incentivized to run their lines at high capacity to cover their fixed costs and get leverage. This makes the industry more competitive despite its concentration. Given IBP’s scale, it can buy insulation foam at a larger discount than smaller competitors and save big on costs.

IBP’s growth strategy

Organic growth is achieved through increasing penetration in developing markets.

On average, an established IBP branch generates ~$4,400 per residential permit versus $2,200 for a new developing branch.

Inorganic – M&A is part of IBP’s expansion story and it aims to acquire ~$100 million of revenue annually.

Strengths

Leading positions in insulation installation, with a 28% market share up from 5% in 2005.

M&A has been a part of its growth strategy since 1990.

Scale = ability to buy product cheaper than smaller competitors.

Weaknesses

Distribution arm is relatively small when compared to peer TopBuild.

No centralized ERP = branches could be competing for the same business.

Complementary products have lower margin due to current lack of scale.

Opportunities

Complementary products.

Capacity to penetrate developing markets.

Increasing residential building codes = higher revenue per unit.

Threats

Weakness in US residential markets.

Current supply constraints cap organic growth.

Supply shortage (COVID-19 period) or explosion/fire at a supplier plant (2018) can temporarily increase cost of raw material.

IBP management

IBP’s management, led by CEO Jeff Edwards since 2004, is a key part of the business’s success. Edwards, who joined the company in 1994 and became chairman in 1999, is one of its largest shareholders.

When we first spoke to Jeff and he walked us through how he built the business, we quickly realized he was a visionary leader with a solid plan for future growth.

He told us how he saw potential in the niche sideline of foam insulation. His rational was simple: every home, every building, needs insulation. He was not looking to reinvent the industry, but rather focused on delivering the best service to builders while acquiring successful businesses in various cities. The sales pitch to targets was also simple: being part of IBP means they can do what they like and not be bogged down by functions that aren’t core to their business, like insurance, human resources, accounting and payroll.

In 1994, IBP made its first acquisition with Freedom Construction in Columbus, Ohio, followed by several more in the ensuing years. The rest as they say is history.

Unseen value beyond the walls

Investment potential often lies hidden in plain sight, like the insulation in our walls. IBP has all the characteristics we look for in an investment: a small-cap company with what we believe to be tremendous growth potential with low debt, rapid revenue and earnings growth compared to its industry, and strong management.

Insulation may not be exciting, but not only does it conserve energy and reduce bills, it also represents a notable sector in our investment landscape. How often do investors overlook the potential in the ordinary and what opportunities might we uncover by paying closer attention to what others may miss?

A year ago in our December 2022 Outlook, we made a case for investing in Canada. Acknowledging that, like many other countries, Canadians accumulated debt to become homeowners in the low interest rate decade prior to the pandemic, there were many positives to admire about the country’s long-term prospects. We believed that Canadian asset markets were well positioned to benefit from these positives. One of the standout reasons was the reshaping of Canada’s demographic pyramid with a large influx of new immigrants.

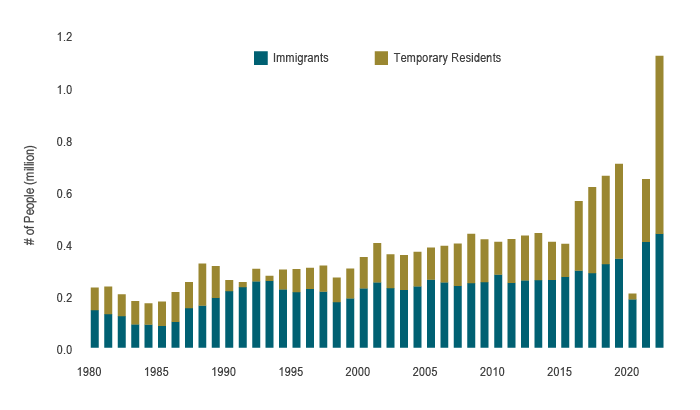

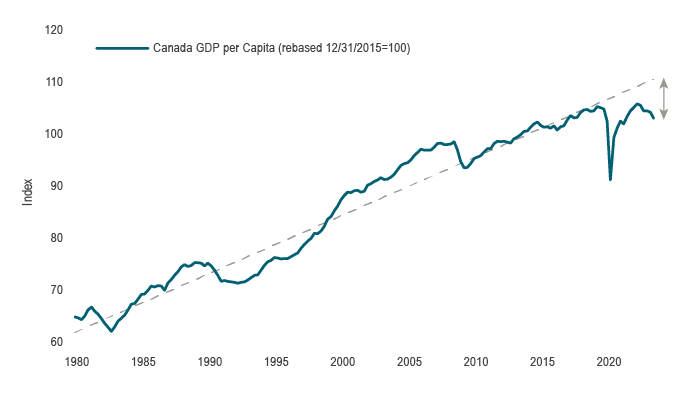

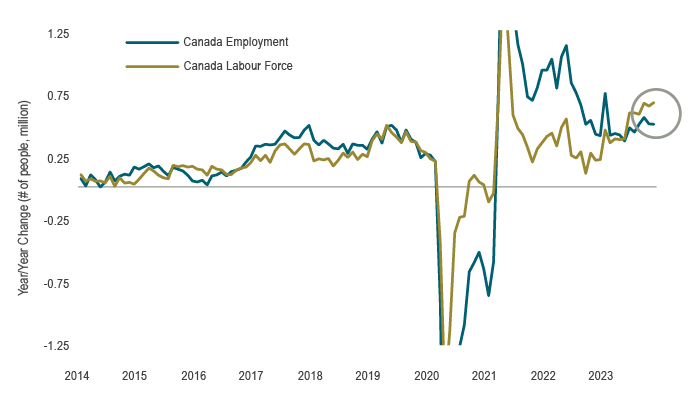

Over the past year, tightening monetary policy has produced its intended effect, and real GDP in Canada will likely grow by a modest 1.2% in 2023 according to the Bank of Canada (BoC). Economic activity is indeed softening through lower consumer spending and business investment, with both taking a hit from higher interest rates. By contrast, Canada’s population is expected to expand by nearly 3% in 2023, the strongest immigration rate in decades (see Chart 1). In total, the population will expand by more than 1 million people – net births contributing about 5%, immigration 40% and the balance non-permanent residents. Taking these together, GDP per capita has not only failed to return to its long-term trend in the post-pandemic expansion but is falling outright and opening up a material gap to our potential (see Chart 2). It is worth exploring the issue of population growth’s outsized impact on Canada, and particularly in the different ways it has been skewing data.

Chart 1: Population surging in recent years

Source: Statistics Canada, Macrobond

Chart 2: While GDP is holding in, per capita activity is falling

Source: Statistics Canada, Macrobond

Data in the context of population growth

There are many reasons for the high inflation over the past few years, with services prices under particular pressure recently through rising wages. The job vacancy rates across the country more than doubled to 6% in the last year compared to the pre-pandemic period, and the influx of new workers has been a welcome source of labour supply. Today, the labour market continues to produce remarkably steady job gains, some 20 months after the start of a record fast rate hike cycle. In November, 25k net new jobs were created, a respectable gain that is above the long-term historical average and continuing a trend that saw average monthly gains of 39.1k year to date. On the flip side, Canada’s population growth casts the job gains in a different and less favourable light as the economy needs to generate a net new 56k jobs each month, in line with the labour force growth, just to prevent a rise in the unemployment rate (see Chart 3). While the data suggest still tight labour markets under normal conditions, the recent surge in population implies at best a balanced labour market today. Indeed, jobs are being filled now and job vacancy rates are now down 2 percentage points from the highs in 2022 to just 3.6% last month, the top end of the pre-pandemic range.

Chart 3: More people joining labour force than finding jobs

Note: Y-axis excludes volatile period during the pandemic.

Source: Statistics Canada, Macrobond

Across housing markets, Canada is well understood to have an affordability problem as home prices compared to incomes top global ranking tables, while home equity comprises an unusually large component of household net worth in the country. Many have attributed this issue to low housing supply. However, construction activity has actually surged in recent years with housing starts averaging some 267k over the last 3 years, 40% above the long-term average (already an achievement given the shortage of skilled trades in the sector). Even so, the new supply has not grown enough to meet the new demand and done little to alleviate the affordability issue. This is particularly true as new residents are only adding to the peak Millennial age cohort that is arriving at the prime household formation age of 32. This imbalance has left cities dealing piecemeal with trying to create supply where possible and forming more robust housing policies. As a result, this sector that is traditionally the most highly sensitive to interest rates may see very little impact through the expected slowdown.

As noted above, only about half of the newcomers are actually immigrants that stay. Understanding this difference may be important given non-permanent residents, comprised of students or those on temporary work visas, may create some further volatility in the data. This is because this group may actually exhibit pro-cyclical characteristics with the economy. For instance, should the labour market soften, workers of all types will be shed, leading many on temporary work visas to search for work elsewhere or return home. Additionally, student visas may slow as overdue government oversight will see a cracking down on sketchier educational institutions and fraud. To put it simply, a strong economy will bring new entrants, but a recession may be exacerbated If some of these new, less permanent residents choose to leave.

As mentioned above and discussed last year, there are many reasons we remain positive on the outlook for Canada. One that is very much not top of mind, but that we believe will become increasingly important, will be that the population growth will dramatically alter the demand for services beyond shelter. Governments may be forced into a renewal of spending on services, buildings and infrastructure, including hospitals, schools, roads and airports, all of which will compound other business investment over the coming years. Indeed, one of our longstanding secular themes has been the significant capex that we anticipate will evolve out of the adoption of artificial intelligence integration, green energy transformation and global supply chain reconstruction. All of this could go far in providing support to reverse what has been a dismal period of productivity.

Capital Markets

More recently, financial markets have been in a cheery mood. November was a banner month for public market assets across the board. After three straight months of negative returns in Canadian equities, the S&P/TSX Composite Index rallied 7.5% in November. That monthly gain was exceeded only five times in the post-Global Financial Crisis era. Every one of the 11 sector groups was in the black this month, led by a massive 27.4% gain in information technology. That strong gain was seen across both large and small cap stocks, with the former outperforming the latter, and cyclical sectors of the market outperforming more defensive sectors. While the November equity market gains were broad based, market breadth has been quite uneven through the year. In the US, there has rarely been a year where the strong returns were generated by so few individual stocks. The S&P 500 Index, weighted by market capitalization, has surged 20.8% year-to-date, thanks primarily to the narrow leadership of mega cap tech stocks; meanwhile the equal weighted S&P 500 Index is up by a much smaller 8.1%. Commodity prices were mixed. Notably oil prices eased back, as WTI fell 5.1% m/m to US$75/bbl and dropped further into early December. Meanwhile, precious metals prices surged to a 6-month high, rising 2.6% in the month. Gold hit an all-time high towards the end of the month, as the US dollar finally lost momentum. Following a surge off the July lows, the dollar broadly depreciated in November.

The shift in sentiment was spurred early in the month by the FOMC meeting and gained momentum with softer US CPI data in combination with Q3 GDP that was revised up to an astonishing 5.2% q/q annualized pace, more than 1.5 years after rate hikes began. This led the market narrative to shift firmly into a soft landing camp. As a result, interest rates began to reflect the likelihood that central bank rate hikes have peaked and that a slowdown is on the way. In Canada, 2-year and 10-year bond yields dropped by about 0.5% while credit spreads tightened materially despite a pickup in issuance. Combined, this led the FTSE Canada Universe Bond Index up 4.29% in November and the Long Bond Index up an astounding 8.54%. The latter marked the highest monthly return for the index since 1982. Similarly, the US Aggregate Bond Index returned 4.53%, its best monthly return since May 1985. The positive returns across both fixed income and equity markets drove traditional 60/40 balanced to post the best monthly returns since November 2020, when markets absorbed the positive COVID vaccine news. Through all that good news, one message to note is that we believe markets remain in a state of higher uncertainty and volatility.

Portfolio Strategy

Indeed, the market narrative remains in constant, rapid flux. Risk assets were displeased with higher interest rates through the summer and fall, and bond markets pushed yields higher than warranted. Once a peak in short term rates appeared at hand, interest rates have tumbled just as forcefully, shepherding in a year-end all-asset rally across public market assets. The risks from here appear to be skewed to the downside, and thus our balanced portfolios continue to underweight equities and hold cash as we anticipate earnings to come under some pressure with the slowdown in the economy. Canadian fundamental equity portfolios are selectively investing in companies with favourable valuations while maintaining a high-quality bias. Fixed income portfolios are increasingly positioning for a move toward normalization in the yield curve while remaining cautious on credit.

Much of the market direction now depends on the ability for policymakers and the economy to hit the soft landing narrative that the markets have now priced in. This in turn hinges on labour markets striking a balance from here. This is true both for the need to limit wage gains and the follow on to services prices in the CPI, and the ability for people to hold on to jobs and sustain spending. To properly assess the economic status quo of Canada, it must be acknowledged that population growth has had an outsized influence. The changing demographic profile of the country will alter short term demand dynamics for labour as well as housing. Data will appear more favourable in absolute terms, but in many ways it will be less optimistic considering the positive population shock. The influx has been beneficial from a labour supply perspective and importantly for future infrastructure development. We are optimistic about the longer run outlook for the economy, but we are expecting to see a rockier cyclical period over the next few quarters. We will explore this further in our year-ahead Forecast to be published in January. From everyone at CC&L, we thank you for your support and wish you a festive holiday season and a prosperous New Year.

Summary

Treasury yields retreated through the month on inflation data that undershot market expectations (in line with our forecasts), with stocks and bonds celebrating the news.

We remain cautious and view the exuberance with scepticism, and expect a weakening global economy and earnings downgrades to test the bulls.

On a brighter note, rapid disinflation and the prospect of rate cuts in 2024 will precipitate a recovery in money numbers that could be the signal to tilt away from current defensive positioning.

Institutional quality is key to unlocking development

Analysis of qualitative macro factors in emerging markets is a cornerstone of our process, which is critical to identifying the potential for downside shocks that can wipe out investor returns (irrespective of how attractive a company’s fundamentals may appear). Given the relative fragility of institutions in EM, politics can have an outsized impact on a country’s progress up (or down) the development ladder, with elections often serving as critical junctures.

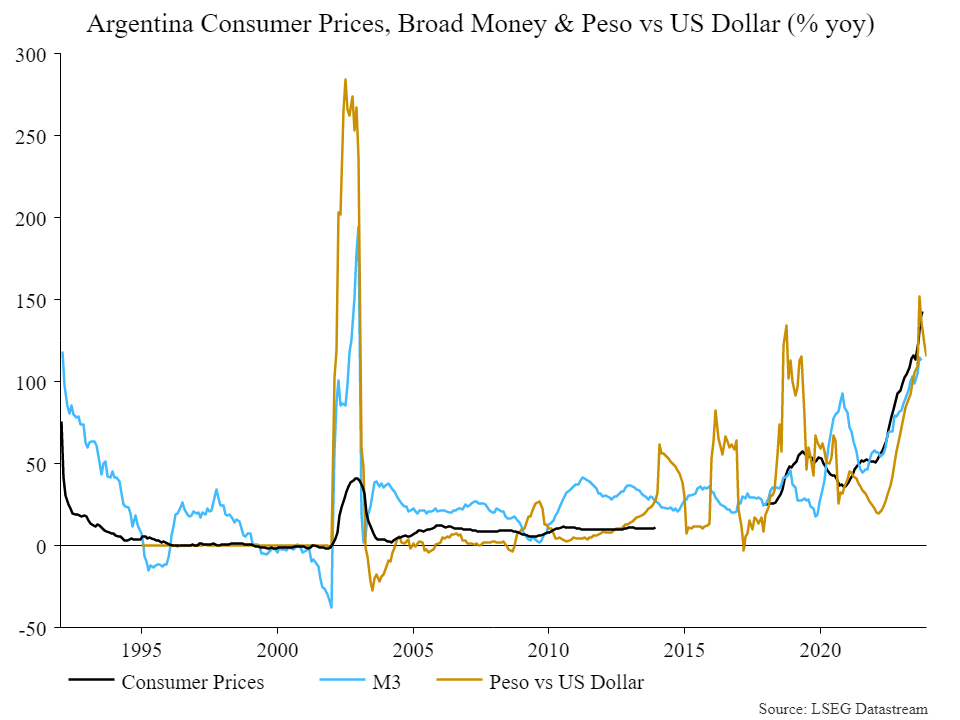

This month we saw the conclusion of national elections in Argentina, with right-wing libertarian and economist Javier Milei crushing the incumbent Perónists on a platform of radical economic reform. While markets have celebrated the development, does Milei’s election truly represent a structural turning point given the institutional forces that stand in his way?

Argentina a case study of the vicious cycle

A hundred years ago, Argentina was one of the richest countries on the planet, with the young and dynamic South American country outstripping the likes of even France and Germany. The rise and dominance of the left-wing populist Perónists in the 20th and 21st centuries (interrupted by a succession of military juntas in the 1970s and 80s) put an end to this.

For us, Argentina’s downward spiral from such an enviable position to today underlies the importance of institutional quality as the key determinant of whether a country climbs or slides down the development ladder. Vicious and virtuous circles of development (where political and economic institutions become either more extractive or inclusive) can form momentum that is hard to break. For EM investors in particular, who deal with countries with relatively more fragile institutions than DM counterparts, it pays to be mindful of what kind of cycle is at play in a country.

The book “Why Nations Fail” by Acemoglu and Robinson provides an excellent summary of these vicious/virtuous circles:

“Rich nations are rich largely because they managed to develop inclusive institutions at some point during the past three hundred years. These institutions have persisted through a process of virtuous circles. Even if inclusive in a limited sense to begin with, and sometimes fragile, they generated dynamics that would create a process of positive feedback, gradually increasing their inclusiveness. England did not become a democracy after the Glorious Revolution in 1688. Far from it. Only a small fraction of the population had formal representation, but crucially, she was pluralistic. Once pluralism was enshrined, there was a tendency for institutions to become more inclusive over time, even if this was rocky and uncertain process.” (Why Nations Fail, p364)

Clearly nothing of the sort occurred in Argentina over the last century. Instead, a confluence of economic and political crises from the 1930s onwards saw the country follow nearly half a century of growth with a lapse into domestic upheaval, the rise of Perónism and extreme political choices that fuelled a vicious circle causing Argentina to backslide.

Rise of the Perónists

While it is possible for countries to grow under extractive institutions, this will begin to falter at more advanced levels of development. Improving institutional quality is essential to break through to the next level.

“It is true that Argentina experienced around fifty years of economic growth, but this was a classic case of growth under extractive institutions. Argentina was then ruled by a narrow elite heavily invested in their agricultural export economy … [involving] no creative destruction and no innovation. And it was not sustainable.” (Why Nations Fail, p385)

Becoming Minister of Labour in 1943 following a military coup, Juan Domingo Perón was elected president in 1946. He then set about attacking Argentina’s institutions much as the previous military junta had done before him. He started by gutting the Supreme Court to remove any checks to his power, and sidelined the main opposition party by arresting its leader. The Perónists emerged as a new elite which shaped extractive institutions to their benefit.

“The Perónists won elections thanks to a huge political machine, which succeeded by buying votes, dispensing patronage, and engaging in corruption, including government contracts and jobs in exchange for political support. In a sense this was a democracy, but it was not pluralistic. Power was highly concentrated in the Perónist Party, which faced few constraints on what it could do, at least in the period when the military restrained from throwing it from power.” (Why Nations Fail, p385)

Is Milei’s election a critical juncture?

Following 28 of the last 40 years under Perónist rule, the country today battles its worst economic crisis in two decades as inflation spirals, poverty rates climb and – in the words of President-elect Javier Milei – the peso “melts like ice cubes in the Sahara.” Such is public frustration for perpetual economic catastrophe that Argentinian voters dumped the incumbents for libertarian rockstar economist Milei, who attracted 56% of the second-round vote, the most votes garnered by any candidate since 1983.

Source: NS Partners & LSEG Datastream

Milei campaigned on the promise of radical change and economic shock therapy. This includes dollarising the economy and eliminating the politicised central bank, putting the “chainsaw” to public spending, privatising state-owned companies, along with a host of controversial conservative social and libertarian reforms. Clearly, breaking the vicious cycle in play in Argentina will require radical policy change. Well implemented dollarisation could indeed work (with a deep recession) to restore economic order, working to reduce inflation, increase consumer buying power, and stabilise the economy in a way that enables better long-term economic planning while attracting foreign investment.

This sounds great in theory and markets have cheered the election results, but can Milei actually translate his victory into policy that passes through parliament when his party holds just 39 of 257 seats in the lower house and 8 of 72 in the senate? An alliance with centre-right former president Macri and his Republican Proposal party still won’t constitute a governing majority, but it will boost the chances of pushing through the reform agenda. For this to happen, however, it is likely that compromises will need to be made with Macri’s moderates and other neutrals. Will Milei, a libertarian firebrand who has gained so much popularity from demonising the political elite, be able to stomach a watered-down agenda?

How do we implement development theory in EM investing?

Our approach to macro analysis is not to place bets on such uncertain outcomes, but instead to assess the direction of travel and mark conviction in that country up or down accordingly. If Milei can beat the odds, then Argentina may gradually emerge as a hunting ground for investment opportunities.

For now, the reality is that powerful structural forces suffocate the country’s potential and make for a fragile environment that can easily wipe out investors lacking a robust approach to accounting for macro risk.

An Opportunity to Foster Mutual Benefit and Support Sustainable Development

This article was originally published in Issue 33 of the Journal of Aboriginal Management (JAM), it focuses on the theme Infrastructure: Building a Better Tomorrow.

Indigenous participation in infrastructure projects promotes the economic empowerment of communities while also contributing to a project’s overall success and sustainability. In this article, we delve into some of the ways Indigenous communities can participate in infrastructure investments, and we highlight the benefits that such partnerships can create.

Infrastructure projects are typically large-scale physical assets that meet a basic human need. These assets are essential to the well-being of communities and critical to the functioning of local economies. Infrastructure encompasses projects such as roads, bridges, schools, hospitals, water distribution and treatment as well as power generation and electricity transmission. The development and construction of these assets require significant investment and involve numerous stakeholders. The importance of infrastructure projects to communities, and their long-term nature and size, necessitate a responsible investment approach to secure and maintain a social license to operate.

Stakeholder engagement plays a pivotal role in ensuring that investments incorporate a wide range of perspectives and create positive outcomes. Ultimately, responsible investment is about generating financial returns while also considering the broader impact on society and the environment. An inclusive approach to engagement is essential in ensuring that all relevant parties are consulted.

There is a growing recognition of the importance of including Indigenous peoples as key stakeholders in infrastructure projects, ensuring their rights, cultural heritage, and economic interests are respected and supported. This is particularly critical in countries such as Canada where many infrastructure projects directly impact Indigenous lands and territories, as well as their peoples and communities.

This increased awareness – combined with more intentional inclusivity on behalf of government and business – should help to facilitate greater participation in the responsible development of further sustainable infrastructure projects in Canada. However, it is important that these efforts are focused on a desire for true understanding of Indigenous perspectives and priorities, as well as genuine relationship building that seeks to achieve mutual benefit. Such an approach fosters transparency while also promoting collaboration and consensus-building, which can lead to better decision-making and outcomes.

Collaboration Fosters Mutual Benefits and Sustainable Development

Positive partnerships provide a promising path towards more inclusive investment opportunities that facilitate the economic empowerment of Indigenous communities while also supporting the development, construction, and operation of high-quality and sustainable infrastructure projects.

Increased Indigenous participation can contribute to reconciliation efforts by encouraging Indigenous business development, self-determination, and positive socio-economic outcomes. The steady cash flows generated by infrastructure investments can provide Indigenous partners with funds to address any number of objectives such as housing, healthcare, education, recreational facilities, community centers, economic development and cultural revitalization – or anything that the community values and sets as a priority.

Engaging Indigenous communities also helps to protect the value of infrastructure investments by mitigating some of the associated risks, helping to avoid or address conflicts and legal challenges early while supporting smoother and more efficient project development and operations.

Scott Munro, Deputy Chief Executive Officer of the First Nations Financial Management Board, highlighted this well in his article on evolving ESG standards (JAM 32): “How well a business considers and respects Indigenous rights will determine how its enterprise value is impacted. As well intended and beneficial as these projects maybe, if corporations fail to demonstrate to investors and lenders that they have the free, prior, and informed consent of the Indigenous people who are being impacted, conflict is a certain outcome. Projects may get delayed or encounter costly litigation, and businesses will face reputational loss and discontent shareholders.”

In addition to mitigating some of the risks associated with infrastructure projects, the active involvement of Indigenous communities from the beginning stages of project planning brings valuable local knowledge and perspectives to the table. Indigenous communities possess deep understanding of their lands, resources, and traditional practices. These perspectives contribute to better project design, deeper insight into areas of archaeological significance, sustainable resource management, biodiversity preservation, and more robust environmental impact assessments while also promoting effective environmental monitoring and maintenance.

Collaboration enhances the sustainability of projects and strengthens stewardship efforts by incorporating Indigenous perspectives and practices that have been proven to be environmentally harmonious and resilient over generations. It can lead to more successful outcomes for both the project and the communities involved, fostering collaboration, trust, and shared prosperity.

Indigenous Opportunities in Infrastructure

There are several different ways in which Indigenous communities can participate in infrastructure projects. This includes direct involvement through equity ownership stakes, revenue sharing and other mutually beneficial arrangements, as well as less direct participation through financial investments in public infrastructure companies or private infrastructure funds.

Most commonly, participation is formalized through some form of a negotiated benefit agreement that governs the relationship between the Indigenous community and the infrastructure project. These agreements outline specific benefits and compensation that Indigenous communities will receive in exchange for their support or consent for a project, ensuring their interests are codified and acknowledged as part of the project’s ongoing operations. Successful agreements facilitate community consultation and approval by addressing community social, economic and environmental objectives while also ensuring an equitable distribution of project costs and benefits. Benefits can include financial compensation, employment opportunities, skills training, and community development initiatives.

Equity ownership stakes provide a means for Indigenous communities to share directly in the economics of infrastructure investments. By having ownership in a project, communities receive profits and participate in aspects of the decision-making processes. Revenue sharing agreements are another way in which Indigenous communities can participate in a share of the profits generated by an infrastructure project and can provide an important source of revenue. Both of these types of agreements can empower Indigenous communities economically, foster job creation, and improve resource access.

In addition to equity ownership stakes and royalty payments, there may also be other mutually beneficial arrangements that can be explored. It’s important to recognize that the needs, values and ambitions of each Indigenous community are unique in the same way that each infrastructure project is distinct. While there are benefits to leveraging past experience and best practices, there is no one-size-fits-all approach. Each discussion needs to begin from a place of respect for Indigenous communities and a willingness for open dialogue to reach a place of understanding and productive collaboration.

CC&L Infrastructure’s Focus on Shared Value and Strong Partnerships

CC&L Infrastructure invests in infrastructure assets with attractive risk-return characteristics, long lives, and the potential to generate stable cash flows on behalf of a wide variety of clients — including Indigenous trusts, public and private pension funds, life insurance companies, financial institutions, foundations and endowments, and high-net worth individuals.

As long-term asset owners and stewards of client capital, CC&L Infrastructure focuses on managing its assets responsibly. This includes a systematic approach to evaluating material environmental, social, and governance factors. We believe this approach improves our ability to manage risk, protect the value of our investments, and enhance long-term investment returns.

Our firm has a long history of working alongside Indigenous partners. We worked with local First Nations on our first investment more than 15 years ago, and today over half of the Canadian infrastructure assets in our portfolio collaborate with Indigenous communities in some fashion. This includes several run-of-river hydroelectric facilities and solar projects where our Indigenous partners have a direct equity investment alongside us.

CC&L Infrastructure is a part of Connor, Clark & Lunn Financial Group Ltd., an employee-owned, multi-boutique asset management firm whose affiliates collectively manage over CAD$110 billion in assets.

2024 is shaping up to be a historically significant year for elections, with around half of the world’s population having the opportunity to vote. An estimated 76 countries will hold elections in 2024, including eight of the 10 most populated (Bangladesh, Brazil, India, Indonesia, Mexico, Pakistan, Russia and the US). Europe will witness the most election activity, with 37 countries voting, followed by Africa with 18.

US elections: The world watches

The US election in November, when voters will choose the next president, the entire House of Representatives and a third of the Senate, is expected to dominate headlines. The most likely scenario is a rematch between President Joe Biden and Donald Trump.

The shifting focus of Europe’s political landscape

The European Parliament elections are in June and the topic of migration will likely be at the forefront of debates. If current trends persist, the EU could see the highest number of asylum applications since the 2015-16 refugee crisis. Once thought of as a solution to labour shortages, migrants are increasingly being viewed by some European politicians as a security threat, despite ongoing worker shortages. This could lead to a meaningful political shift toward stricter immigration controls.

Dutch elections: A sign of the times?

The Netherlands’ snap elections on November 22 were perhaps a glimpse of what is to come, with the far-right Freedom Party led by Geert Wilders winning unexpectedly. No party achieved more than 25% of the vote, necessitating coalition talks that could stretch well into 2024. In addition to a strict stance on immigration, the Freedom Party campaign included higher taxes on banks, which negatively impacted Dutch bank stocks the following day. However, the Amsterdam Stock Exchange remained stable after the election due to the pending coalition formation.

Poland’s election results as a market catalyst

Poland’s October elections saw a major upheaval, with the long-ruling nationalist party being replaced by pro-Europe parties, lifting Polish markets the following day.

From voting booths to market trends

That is not to say all elections wield the same influence. Russia’s elections are unlikely to challenge Vladimir Putin’s stronghold. Brazil and Turkey will hold local or municipal elections, while the EU will elect its next parliament.

India, the world’s largest democracy, is likely to see Modi’s party re-elected in May despite some recent discontent. Indonesia will also hold elections early in the new year.

Taiwan’s January elections, important for their geopolitical implications, are expected to see the pro-independence party maintain control. It remains to be seen how the country’s relationship with China will develop from there.

Understanding the election effect on markets

US Bank reports that the S&P 500 Index typically experiences lower returns due to investor uncertainty before US presidential elections, with stronger returns in the following year regardless of the election outcome. Notably, returns tend to be higher when an incumbent party is re-elected and when one party wins decisively, suggesting larger policy changes.

Investing smart in election years

We believe our diversified portfolio is especially critical in periods of uncertainty. Election outcomes can heavily influence economic policies, affecting taxation, regulations and economic reforms. These changes have the power to shape various sectors and industries in profound ways. Safeguarding your investments by diversifying across different securities and industries is a wise strategy.

The role of quality companies

Quality companies that demonstrate enduring strength, guided by capable management and driven by long-term secular trends are well-equipped to weather the market’s ups and downs. Their resilience and adaptability often become key to their sustained success, offering a more grounded perspective for investors looking beyond the immediate horizon of shifting politics.