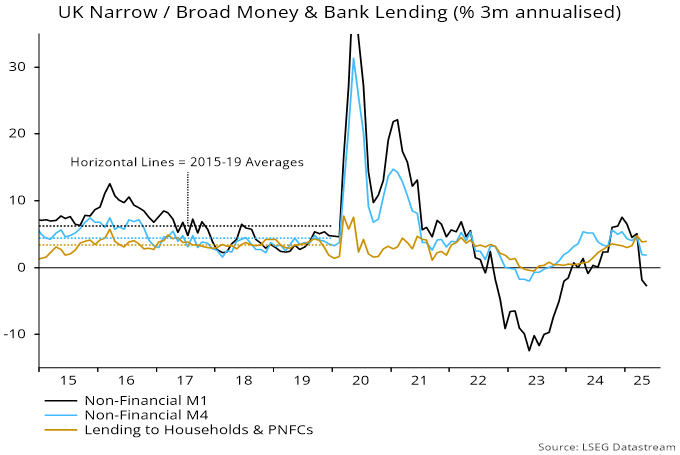

UK money momentum has weakened alarmingly. The broad non-financial M4 measure – comprising holdings of households and private non-financial corporations (PNFCs) – grew by just 1.9% annualised in the three months to May. Non-financial M1 contracted at a 2.7% pace – see chart 1.

Chart 1

Three-month bank lending growth held up but is likely to fall sharply as a large monthly rise in March – related to the end of the stamp duty holiday – drops out of the calculation. Lending typically follows money trends.

It is unusual for narrow money to lag broader measures when interest rates are falling – lower rates reduce the opportunity cost of holding more liquid forms of money, encouraging a shift out of time deposits and savings accounts. 21% of non-financial M1 is non-interest-bearing. The average interest rate on the stock of household time deposits fell by 31 bp between August and May, according to BoE data.

The demand to hold narrow money is driven mainly by the need to finance future spending, so weakness despite rate cuts is ominous for economic prospects. Put differently, money trends support the view here that MPC policy easing has been too slow, providing insufficient support for activity and increasing the risk of an inflation undershoot.

The monetary relapse could partly reflect payback for temporary factors that boosted growth in late 2024 / early 2025.

A jump in money numbers in October appears to have been related to asset sales in anticipation of changes to capital taxes in the Budget at the end of that month. An asset disposal can boost broad money if financing by the purchaser involves – directly or indirectly – an expansion of banks’ balance sheets*. The effect, however, would be expected to reverse as the seller of the asset deployed the proceeds.

Mortgage lending and broad money were boosted in Q1 by front-loading of housing transactions ahead of the end of the stamp duty holiday. Increased activity may also have resulted in a temporarily higher demand for narrow money.

A reversal of these effects may explain broad money stagnation and a narrow money decline in April / May. Still, annual rates of change should be free of such influences and have slowed to 2.5% for non-financial M1 and 3.6% for M4, from recent peaks of 3.4% and 4.8% respectively. Eurozone annual non-financial M1 growth, by contrast, has risen further to 4.3%.

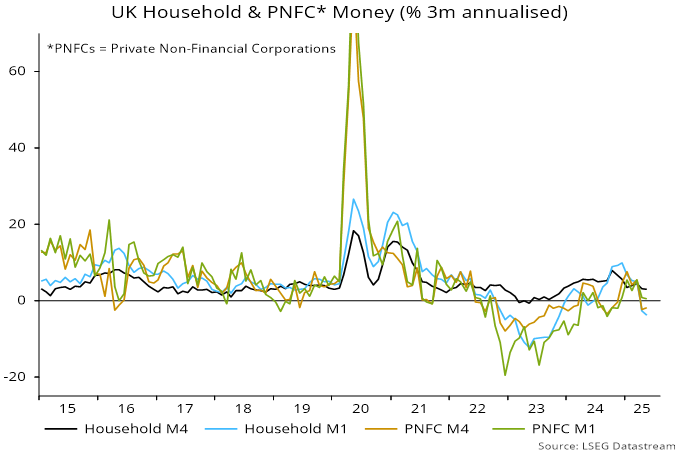

The sectoral breakdown shows that the recent fall in narrow money reflects a switch by households into time deposits / cash ISAs – their aggregate money holdings have continued to expand, though at a slower pace. By contrast, corporate broad money contracted in April / May, consistent with a negative financial impact from NI and minimum wage hikes – chart 2.

Chart 2

The annual rate of change of corporate broad money is back in negative territory, following small positive readings over December-April, suggesting further weakness in employment and fading capex prospects.

*More precisely, an expansion of banks’ domestic lending or net foreign assets, or a fall in their net non-deposit liabilities.