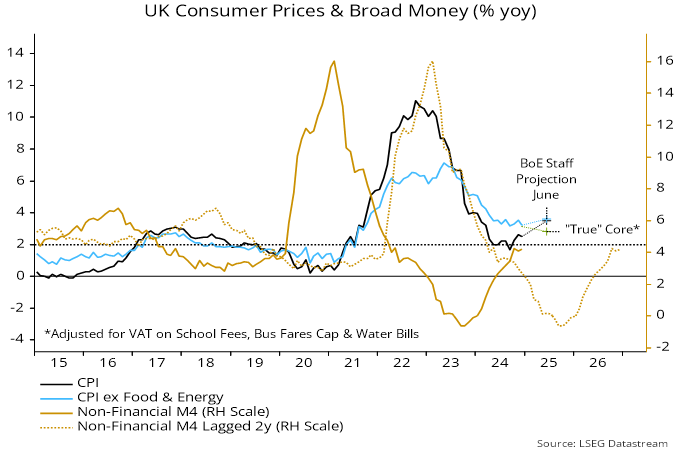

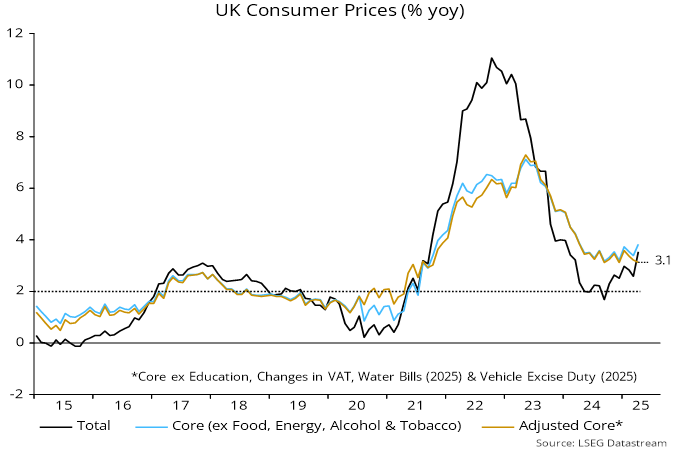

UK April inflation numbers were much less bad than reported.

Annual headline and core CPI inflation rose by 0.9 pp and 0.4 pp respectively from March, to 3.5% and 3.8%. These increases, however, were entirely attributable to hikes in government-controlled prices and vehicle excise duty (VED).

Water and sewerage charges rose by 26% in April versus 8% a year earlier, boosting annual headline and core rates by 0.18 pp and 0.23 pp respectively.

“Other services for personal transport equipment” – a category dominated by VED – rose by 19% versus 4% a year ago, adding 0.22 pp and 0.28 pp to headline and core rates.

The household energy price cap was raised by 4.7% versus a 12.4% fall in April 2024, boosting the headline rate by 0.65 pp.

Summing the above, official actions added 1.05 pp to the headline rate and 0.51 pp to core – more than the actual March-April increases.

Accordingly, the adjusted core rate calculated here fell from 3.2% in March to 3.1%, equalling its recent low (in December and September 2024) – see chart 1.

Chart 1

This measure, moreover, takes no account of Easter timing effects, which may have further inflated the April outturn. For example, air fares rose by 27% last month versus 7% in April 2024, implying a 0.13 bp lift to annual core.

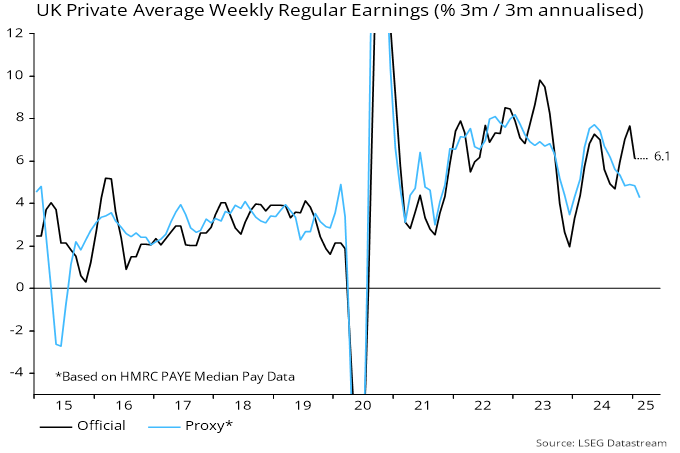

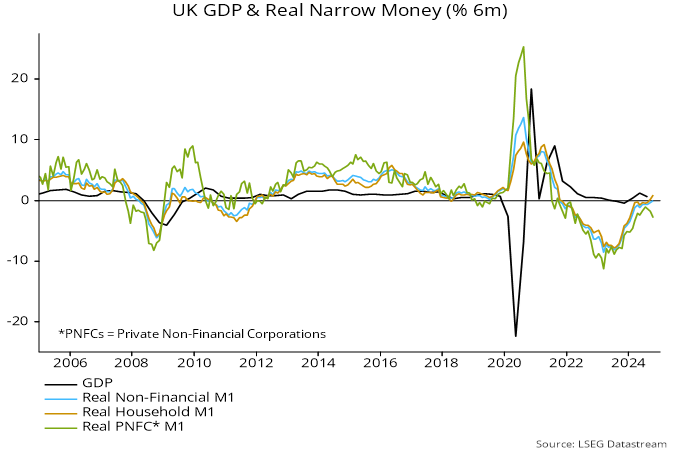

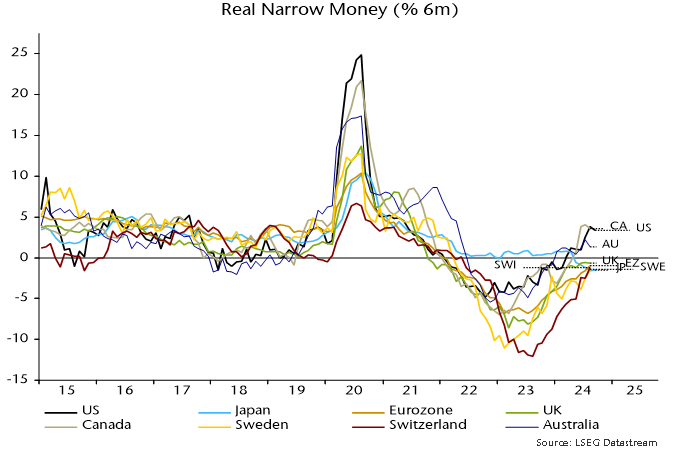

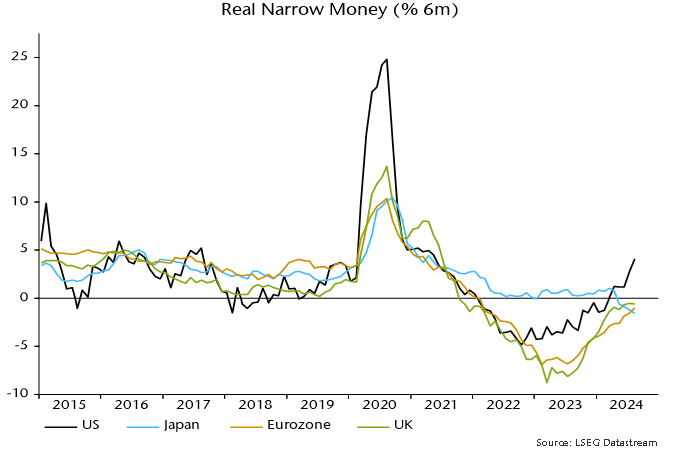

Underlying softening is consistent with lagged money trends and sterling appreciation – the effective rate is currently 3% above its 2024 average level and 7% higher than in 2023.

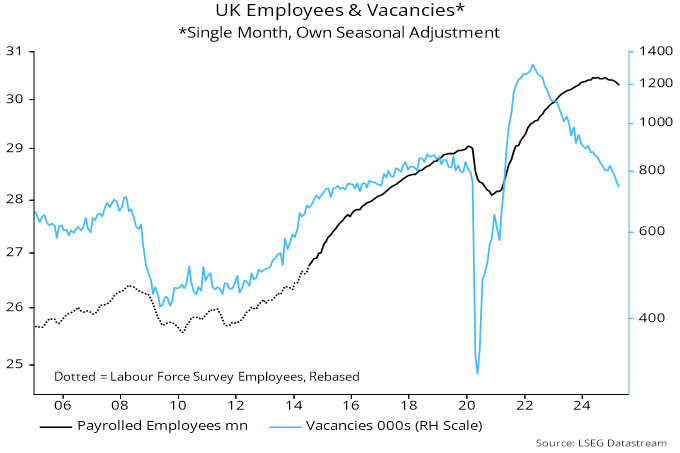

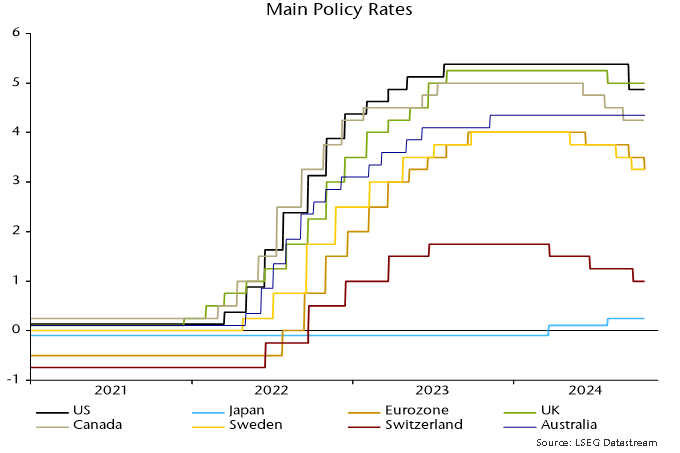

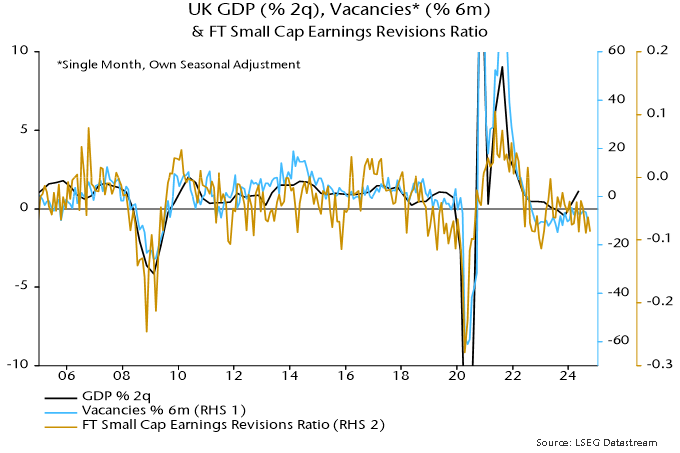

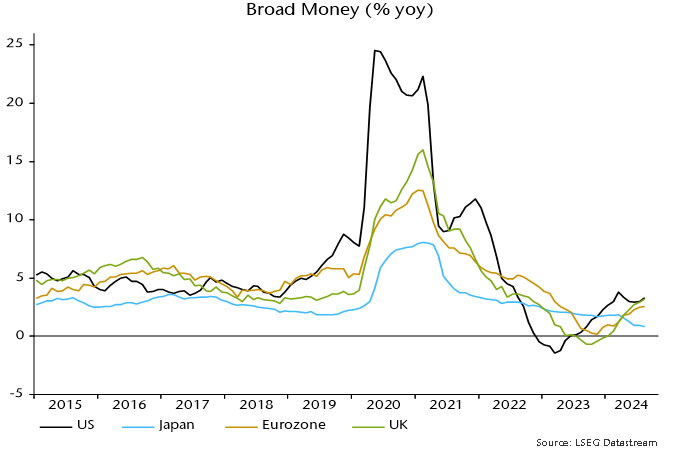

The MPC is concerned that another inflation pick-up, although unrelated to monetary policy, will generate “second-round” effects. Still-subdued money growth, currency strength and a weakening labour market argue for a relaxed view.