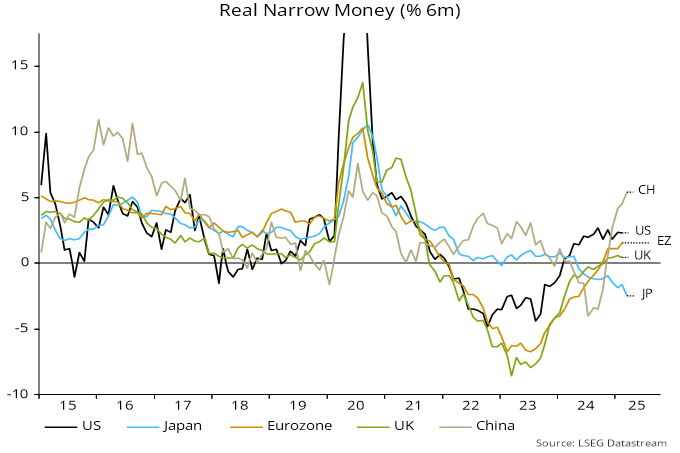

Monetary trends suggest that China’s economy is better placed to withstand tariff damage than Japan’s.

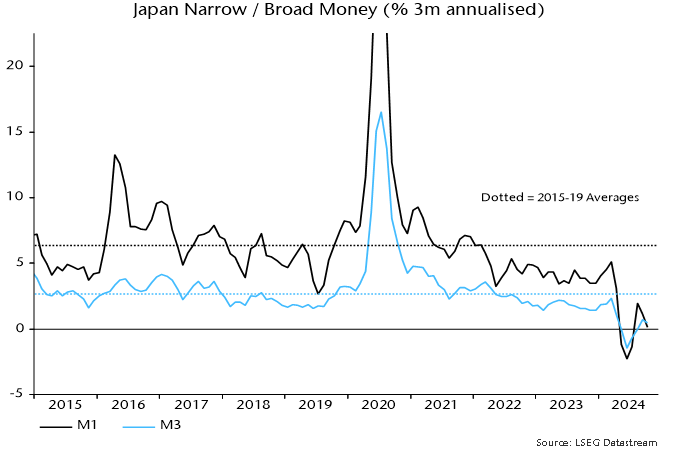

Chinese six-month real narrow money momentum rose further in March, reaching its highest level since August 2020. Japanese momentum moved deeper into contraction – see chart 1. (US March numbers will be released next week, with Eurozone / UK data the following week.)

Chart 1

Inflation divergence has contributed to the wide gap but it mainly reflects nominal money trends: Japanese narrow money is contracting even in nominal terms.

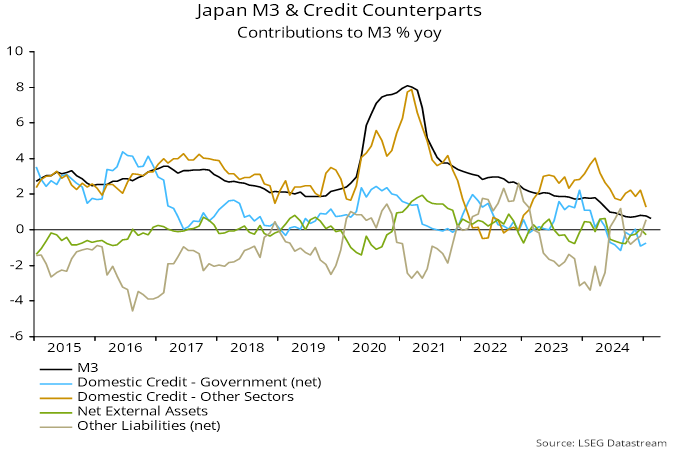

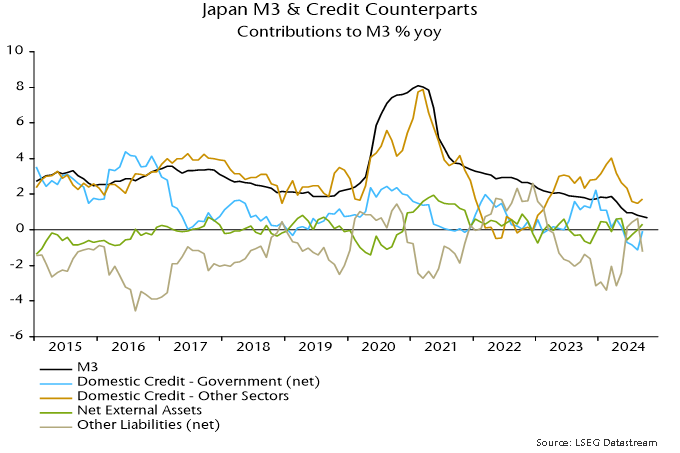

The Japanese fall is partly explained by money-holders switching out of sight deposits (included in narrow money) into time deposits (excluded), which now pay modest interest. Still, broad money trends are also weak: M3 grew by just 0.5% at an annualised rate in the six months to March. Broad money expansion has been dragged down by BoJ QT and a fall in bank lending to non-bank financial corporations.

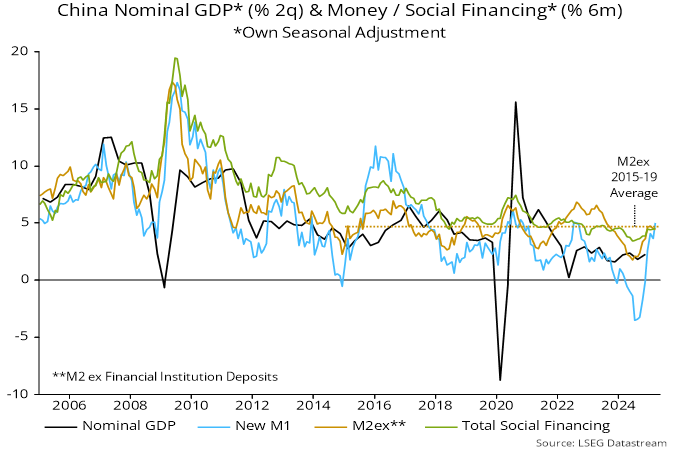

By contrast, six-month growth of Chinese broad money – on the preferred definition here excluding deposits held by financial institutions – was stable in March at a level close to the 2015-19 average. This pace was associated with solid nominal GDP expansion – chart 2.

Chart 2

Broad money trends have been supported by PBoC and state bank purchases of government bonds issued to finance fiscal stimulus measures. In addition, six-month growth of bank lending has revived recently, despite a drag from debt swap operations (under which funds raised through bond issuance are used to repay bank loans of government-related entities).

Previous posts suggested that Japanese monetary weakness would be reflected in downside economic and inflation surprises. The composite PMI output index fell sharply last month, to well below levels in the US, Eurozone, UK and China.

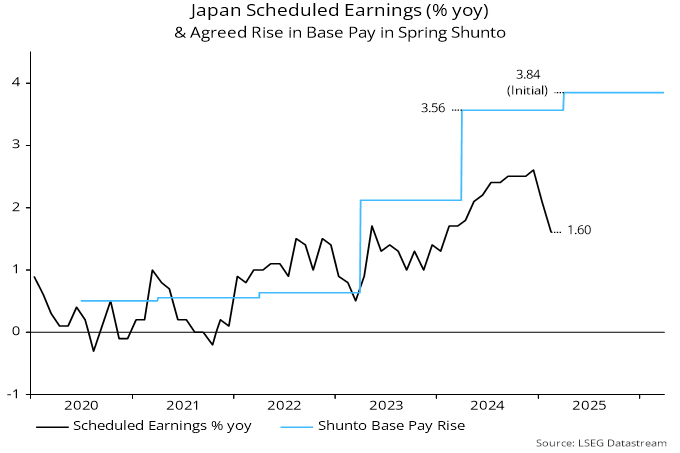

Annual growth of scheduled earnings, meanwhile, undershot expectations in February. Inflation believers have been relying on a developing wage-price spiral but bumper headline pay awards in the spring Shunto may not be representative of trends across the whole economy – chart 3.

Chart 3