Eurozone services price momentum is “unsticking” as expected, supporting the forecast of sub-2% 2025 inflation.

A post in September suggested that the ECB staff’s latest inflation forecast – like earlier projections – would be undershot.

With November’s favourable surprise, annual headline and core (i.e. ex. energy and food) consumer price inflation are on course to average 2.2% and 2.7% respectively in Q4, versus ECB September central projections of 2.6% and 2.9%.

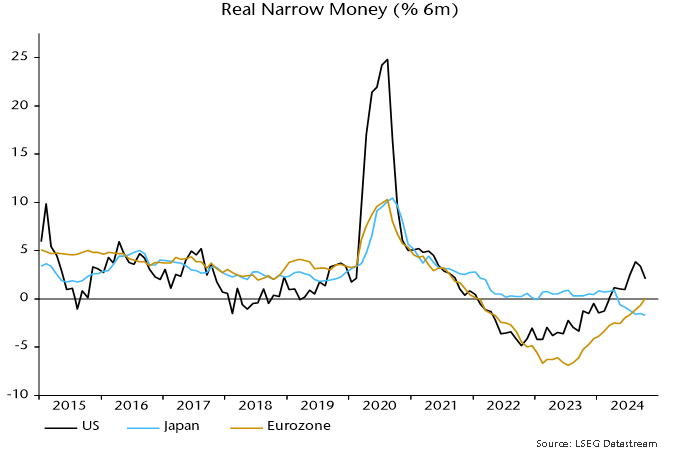

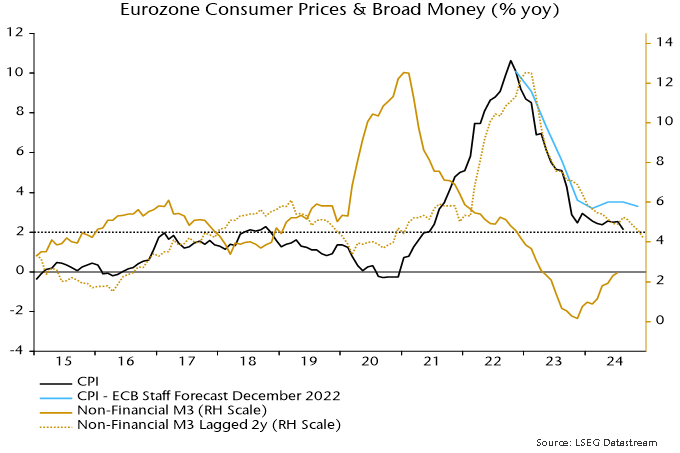

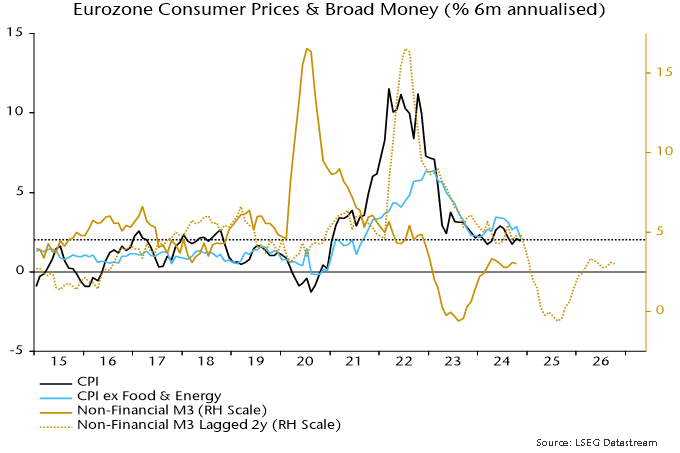

Six-month headline / core momentum is still loosely tracking the profile of broad money growth two years earlier, a relationship suggesting a further decline and undershoot of the 2% target – see chart 1.

Chart 1

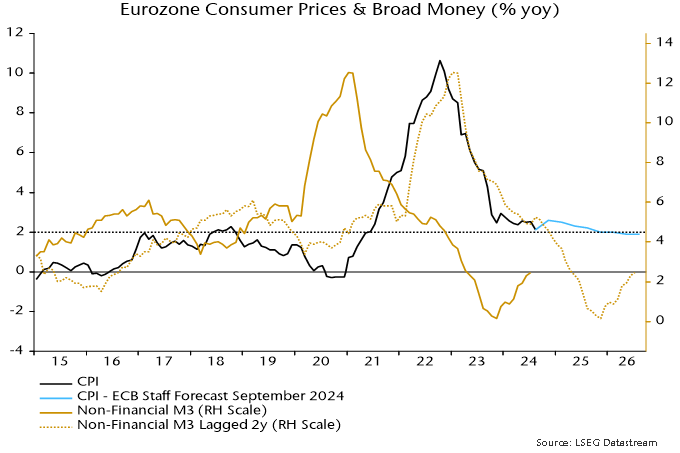

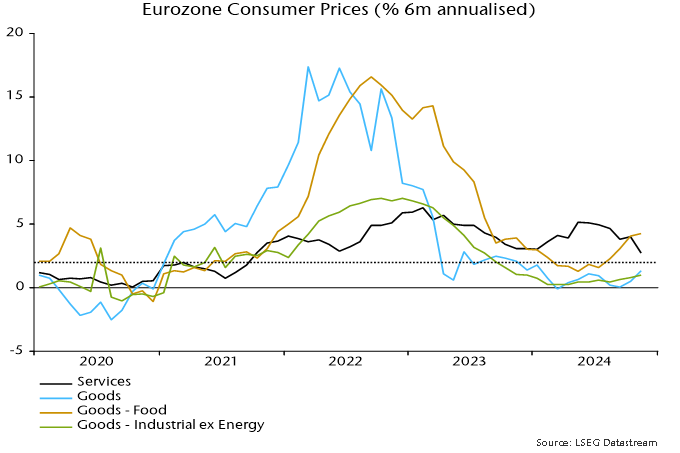

A fall in six-month core momentum to 2.1% annualised in November was driven by a sharp slowdown in services prices, which fell marginally on the month (ECB seasonally adjusted series).

Previous posts questioned central banks’ focus on “sticky” services inflation. Monetary conditions determine aggregate inflation, with the component breakdown partly shaped by “exogenous” factors. Earlier weakness in energy / food and core goods prices suppressed headline inflation while allowing consumers to spend more on services, delaying price deceleration in that sector. The suggestion was that services disinflation would speed up as downward pressure on goods prices eased.

This appears to be playing out: six-month goods momentum has recovered, mainly reflecting food price reacceleration and a slower fall in energy costs, with the headline impact neutralised by a “surprise” services slowdown – chart 2.

Chart 2

The “monetarist” relationship, taken at face value, implies a period of falling prices in 2025. The judgement here is to downplay this possibility and regard the monetary signal as directional rather than giving strong guidance about the level of price momentum.

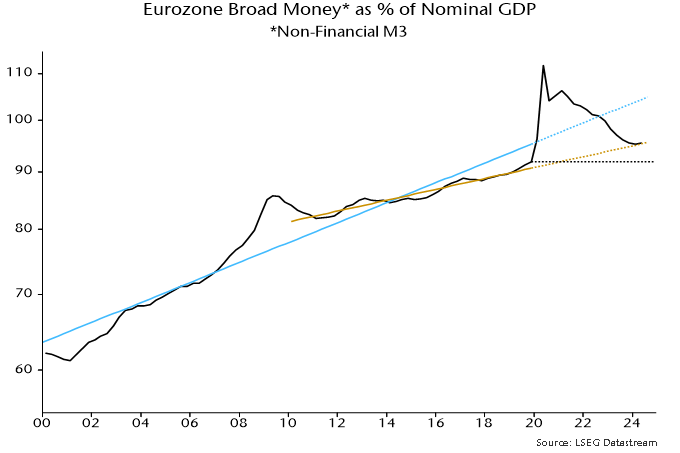

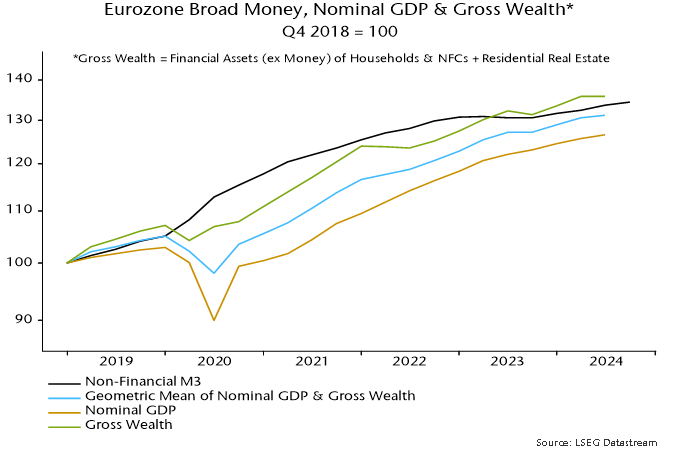

The stock of money could still be above “equilibrium”, implying a cushion against deflation. This question can be addressed using the “quantity theory of wealth” – the idea that asset prices and incomes adjust such that a geometric average of wealth and nominal GDP rises in line with broad money over the medium term.

Chart 3 shows that, using Q4 2018 as a base, nominal GDP has lagged broad money significantly while wealth has slightly outpaced it. The nominal GDP / wealth average was still 2% short of the level implied by the money stock as of Q2 2024.

Chart 3

A small “excess” money cushion, along with recent currency weakness, may head off an extreme scenario but money trends still suggest a sustained inflation undershoot and a need for further policy easing to achieve medium-term realignment.