Here we are, almost halfway through 2023, and we’re seeing many of the same investment themes we saw last year. Large-cap stocks continue to outperform, driven by the usual suspects. The Federal Reserve (the Fed) has continued to raise rates at the fastest pace in history. The US debt ceiling still looms. Meanwhile, weak economic data and a tight lending cycle point towards a recession. Given these factors, it may seem like large-cap investments are a safer choice than small caps. But there’s another side to the story.

What’s really driving the so-called large-cap performance?

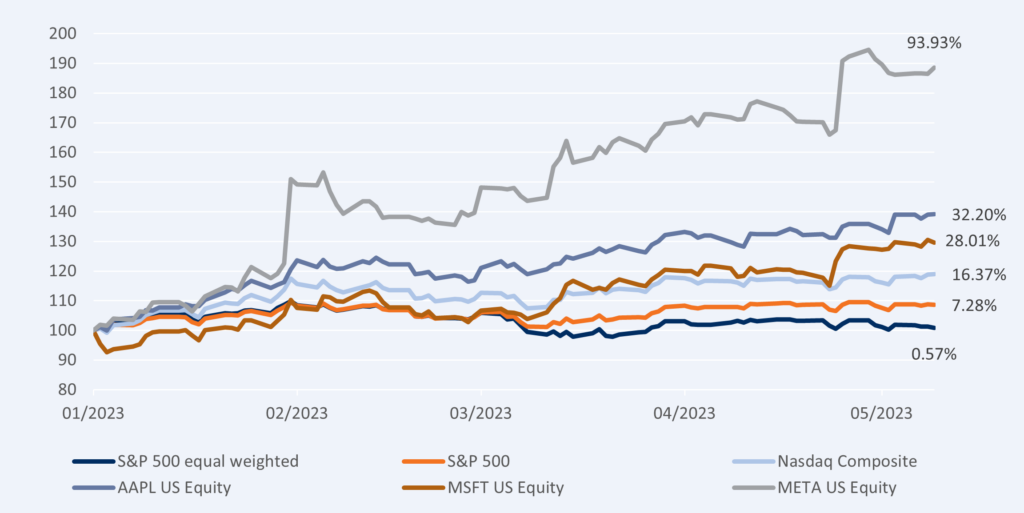

Under the surface, a handful of stocks are responsible for driving most of the S&P 500 Index’s outperformance, which also happen to be the same names driving the Nasdaq Composite Index’s performance. The year-to-date return of an equally weighted S&P 500 stands at a mere 0.57%, nowhere near the 7.28% performance for the S&P 500. As for the Nasdaq, Microsoft, Apple and Meta alone account for approximately 30% of the Index, thus driving its results. We believe large-cap indices currently lack adequate diversification to provide safety in a downturn. Their heavy dependence on a single industry, namely tech, is a vulnerability.

As at May 9, 2023

Large caps seem ready to disappoint

As of March 8, 2023 (the day before the Silicon Valley Bank failure came to light), the Russell 2000 Index was outperforming the S&P 500 by 274 basis points (bps). Understandably, the bank crisis led to significant outflows from small-cap ETFs into large caps, which seemed safer given the circumstances. Consequently, large caps are currently outperforming. However, it’s crucial to bear in mind two key factors. Firstly, the Russell 2000 is still far more diversified (and therefore safer in our view) than the tech-heavy large-cap index. Secondly, we believe patient investors will be rewarded as valuations normalize.

In fact, we anticipate that small caps will make a powerful comeback as large caps lose momentum, driven by the following reasons.

- De-globalization leading to lower margins for large caps: According to Goldman Sachs research, S&P 500 margins have risen by 700 bps since 1990, with 70% of the increase attributed to cost savings on goods and the balance to lower taxes and interest rates. However, with de-globalization on the horizon, we believe it’s just a matter of time before investors reduce their overweight positions in large-cap stocks as their margins dwindle. Instead, they’ll turn to smaller caps, which are poised to benefit from local economies.

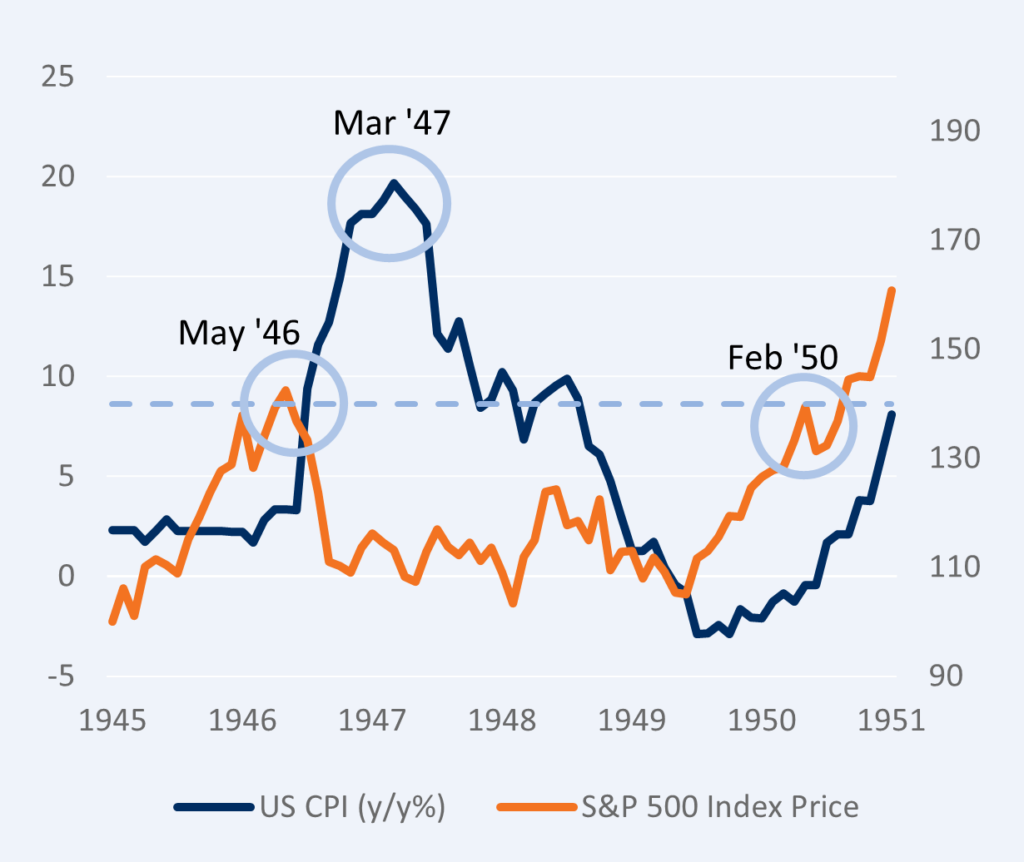

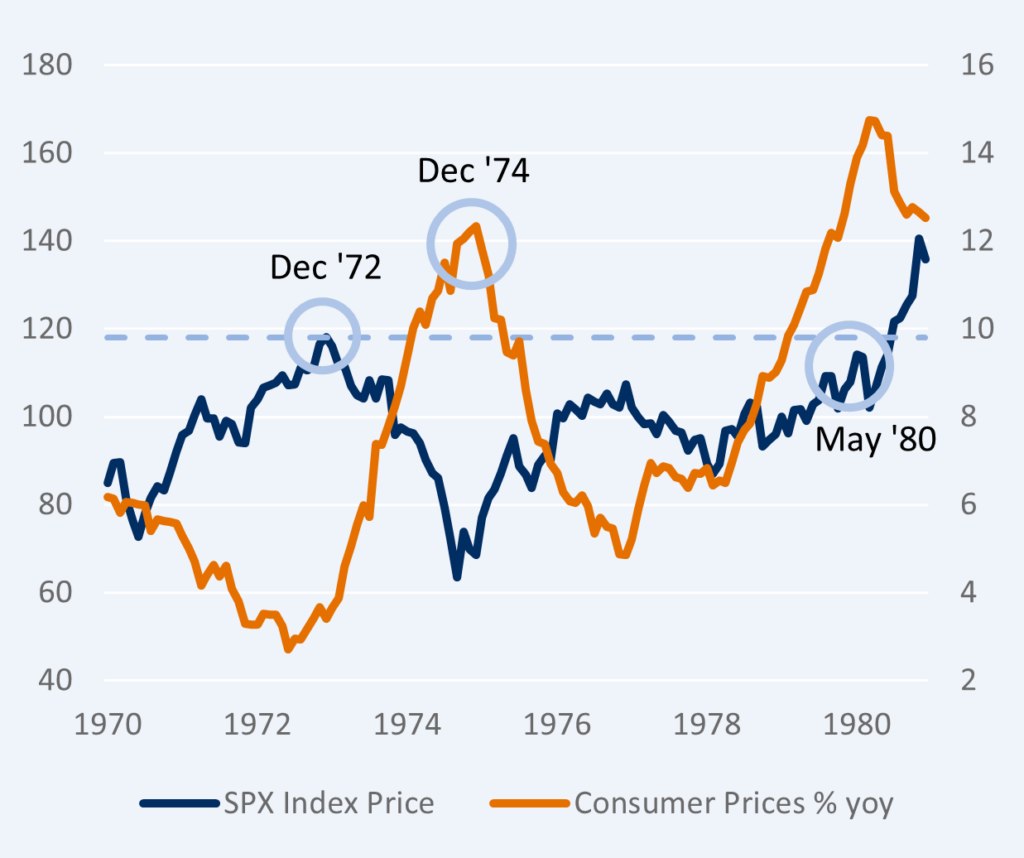

- Historical data shows that periods of high inflation often correlate with stagnant large-cap performance. Take the 1940s and 1970s – two of the worst decades for inflation in the 20th century.

During the post-WWII period, distortions across supply chains and labour markets fueled a 20% spike in US CPI. Large caps went nowhere for the next four years. Similarly, during the stagflation era of the 1970s, large-cap performance remained flat for over five years while quality small-cap stocks emerged as winners.

Large cap equities were flat for >42 months post-WWII

…and for >5 years during the 1970s inflation shock

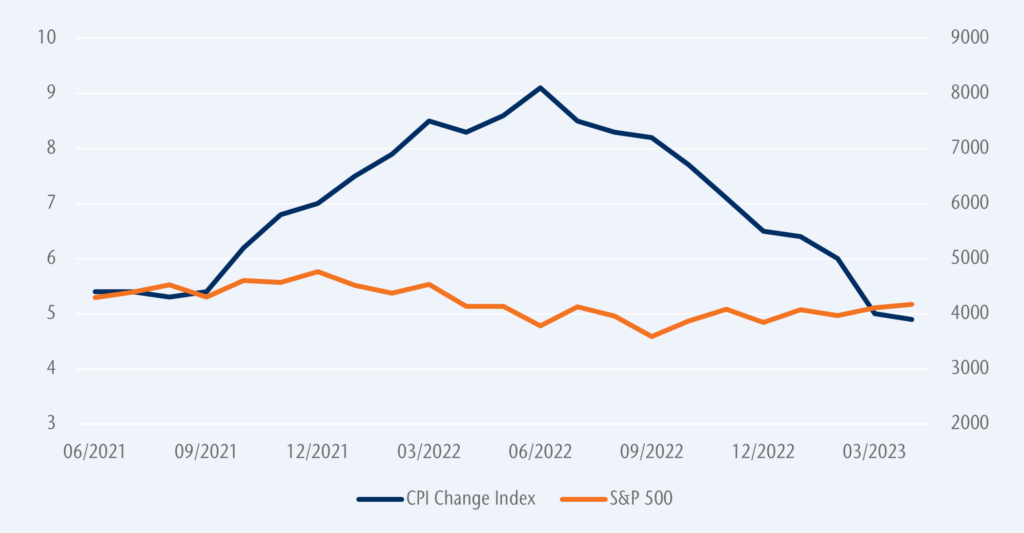

If we look at recent large-cap performance amidst soaring inflation, we find a similar pattern across three different time periods. As Mark Twain famously said, “History doesn’t repeat itself, but it often rhymes.”

S&P 500 vs. CPI Change Index

- Remember the Nifty Fifty stocks of the 1960s? These were the esteemed blue-chip companies of that era – expensive but deemed “safe.” The only problem was, when the tide turned, they plummeted to single-digit multiples almost overnight. Today, the five largest stocks account for 20% of the S&P 500, indicating even worse diversity than the dotcom bubble. It begs the question: where else can they go but down?

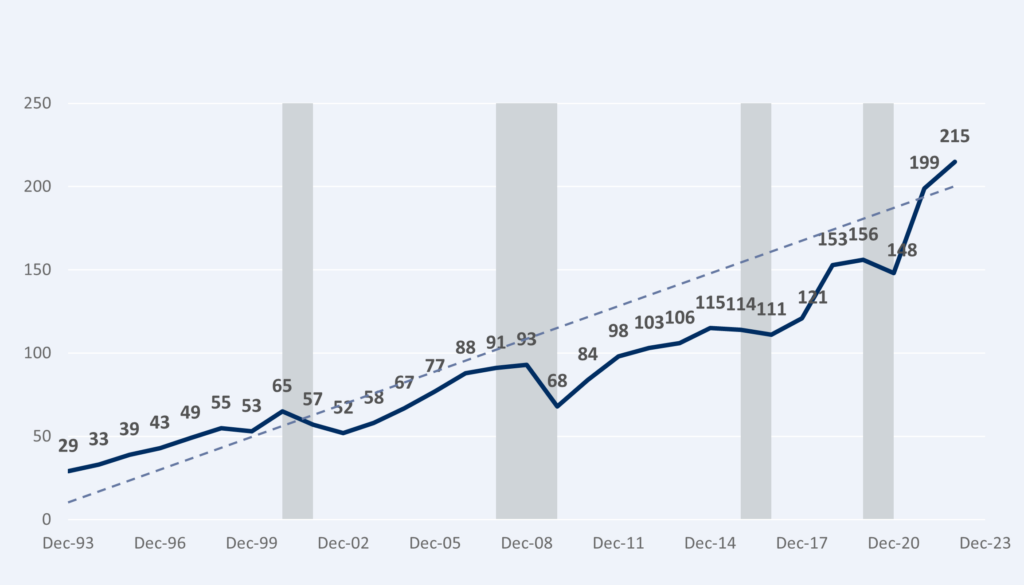

- Analyst estimates for the S&P 500 call for earnings to increase from $204 to $225 (+10%) in 2024. Sounds impressive, right? Yet historically, large-cap earnings do not jump that high coming out of recessions (see chart below). In reality, it was the billions of dollars in stimulus during COVID that propelled S&P 500 earnings to grow at an unprecedented pace. Can we really rely on this trend continuing?

S&P 500 TTM positive operating EPS (log scale) with exponential trend

Grey bars are negative y/y% “industrial production contractions” (R2 = 0.9469)

Take advantage of cheap, high-quality small-cap stocks

For some time now, low-quality stocks have been more expensive than their high-quality counterparts, primarily driven by inexperienced traders. Jefferies reports that lower return on equity (ROE) names are trading at 4.6x sales, a staggering 60% above their long-term average. In contrast, the highest ROE names are trading at 1.2x sales. In our view, this is a clear signal to avoid these low-quality stocks (which are poised to plummet in value) and focus on quality names with strong fundamentals that currently offer attractive buying opportunities.

So, what exactly makes a quality company? While there may be varying definitions of quality among experts, we can turn to research done by Hsu, Kalesnik and Kose who identified seven metrics used by popular index providers to define quality. These metrics are: profitability, earnings stability, capital structure, growth in profitability, accounting quality, payouts and corporate investment.

Quality stocks not only exhibit defensive characteristics but are typically less exposed to macroeconomic influences due to lower operational and business risks. Stronger balance sheets and a consistent track record of predictable profits help mitigate downside risk as well.

The secular case for small caps is intact, with a leadership shift to “old economy” stocks, capex beneficiaries and domestic-focused companies from large caps – all of which bode well for small caps. Valuations of small caps versus large caps currently remain near multi-decade lows, suggesting better returns for small caps over the next decade.

M&A activity is also heating up. While the market overlooks quality small-cap companies, private equity and strategic corporate buyers are capitalizing on the market dislocation to acquire high-quality companies at attractive valuations.

What’s the impact on your portfolio?

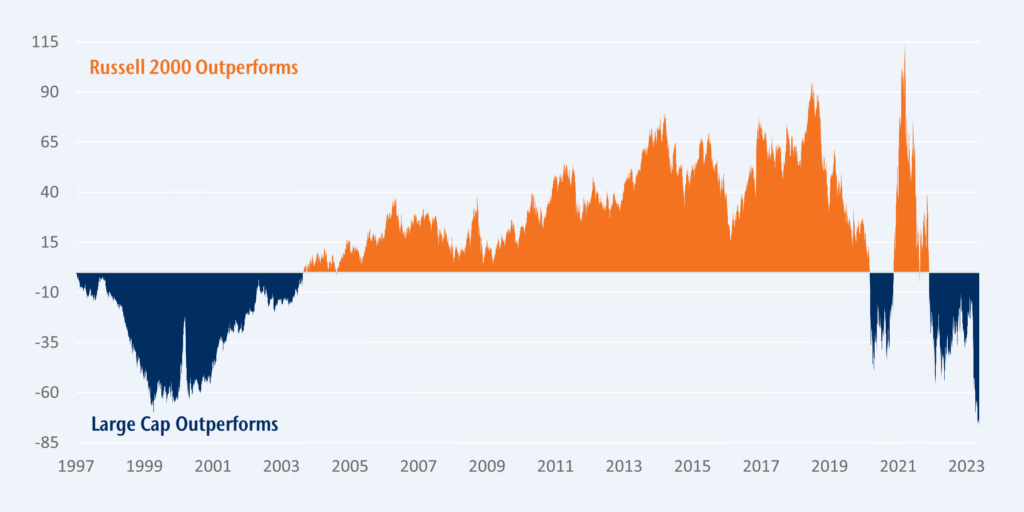

Large-cap and growth stocks have benefitted from the past decade’s zero-rate policy, low inflation and sluggish nominal growth. However, the current macro landscape is ripe for new leadership, which we believe will come from quality small-cap companies. As the chart below shows, large caps seem due to underperform, creating an opportune environment for small-cap leadership. We believe it’s only a matter of time before this transition happens.

Our portfolio consists of market leaders that are outpacing industry growth. These holdings fit the definition of “Quality Small Cap” with strong industry growth, little to no debt and faster earnings growth. Furthermore, they’re trading at a discount compared to their historical valuations.

As the tide turns against large-cap stocks, these companies are poised to benefit. Not to mention, higher interest rates have the potential to benefit our portfolio holdings, enabling them to gain market share and continue to deliver strong and predictable earnings growth.

Large-cap buyers beware; small caps are coming for you.