The Bank of Japan’s attempt to withdraw policy accommodation is understandable but misguided. Monetary weakness suggests that the economy is on course to return to deflation.

The BoJ’s difficulties stem from the inflationary policy mistake of the Fed and other G7 central banks in 2020-21. Subsequent tightening to correct this error works partly by boosting currencies to export inflation to – and import disinflation from – countries with responsible policy-making, including Japan.

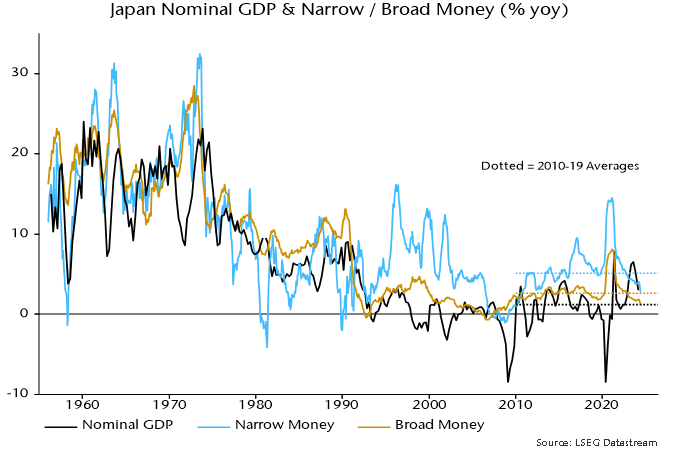

What about Japan’s home-grown inflation? This was minor and is fading fast. Annual broad money growth peaked in 2020-21 at 8.1% in Japan versus 24.5%, 12.5% and 16.0% in the US, Eurozone and UK respectively. Japanese growth was back at its pre-pandemic (i.e. 2010-19) average by end-2022.

A bumper 5.08% pay award in the spring Shunto is an echo of an inflation pick-up driven mainly by a weakening yen. Most workers are non-unionised / employed by SMEs and will receive smaller increases. Falling inflation, slowing profits and a softening labour market suggest a much lower award next year.

The latest money numbers are ominous. Broad money M3 fell by 0.1% in both April and May, following the BoJ’s removal of negative rates in March. May weakness was driven by f/x intervention– record yen-buying of ¥9.8 trillion last month equates to 0.6% of M3.

Annual M3 growth slumped to 1.3% in May, the lowest since the GFC and half the 2010-19 average, suggesting a fall in annual nominal GDP growth below its respective average of 1.2% – see chart 1.

Chart 1

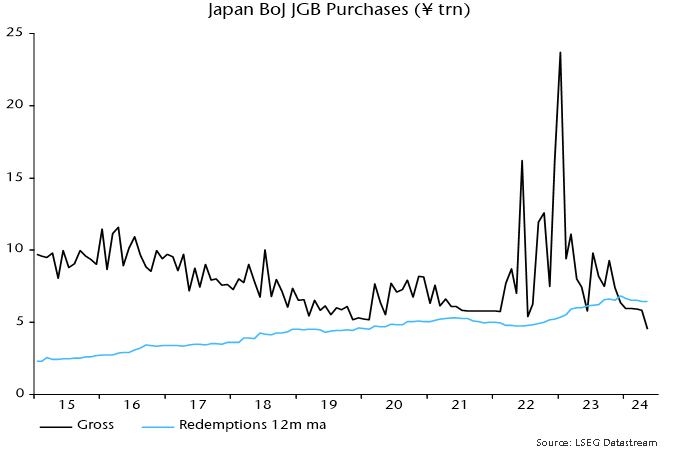

The BoJ, meanwhile, had moved towards QT before the June MPC announcement of a reduction in JGB purchases from July, with gross buying in May well below the run-rate of redemptions – chart 2.

Chart 2

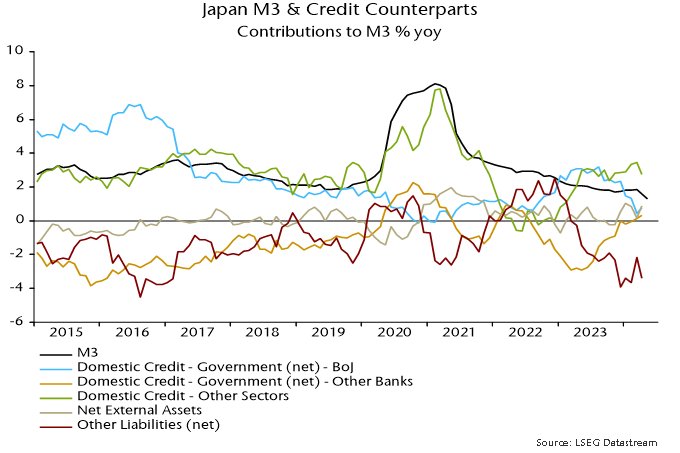

Monetary weakness contrasts with respectable bank lending expansion – commercial bank loans and leases rose by an annual 3.0% in May. The contribution to money growth, however, has been offset by a combination of increased non-deposit funding, reduced BoJ JGB buying and, in May, a fall in net external assets due to f/x intervention – chart 3*.

Chart 3

What should the BoJ do? A monetarist purist would argue for reversing policy tightening and accepting the currency consequences. Likely further yen weakness, however, would prolong current high inflation – a significant cost to balance against the benefit of avoiding a medium-term return to deflation.

The least bad option may be to signal tightening but delay meaningful action in the hope that a dovish Fed shift will lift pressure off the currency soon. This could be a reasonable description of the BoJ’s recent behaviour.

*Note: the counterparts analysis is available through April.