In our last commentary, we discussed Germany’s recent infrastructure bill worth EUR500 billion to be deployed over twelve years. A key component of this bill is climate-led investments, worth one-fifth of the total budget, which finances the energy transition and climate protection measures. Examples of these measures include energy-efficient building renovations, development of electric mobility infrastructure, expansion of the hydrogen industry, promotion of energy efficiency, technologies to decarbonize industrial operations, etc.

Many countries have implemented clean energy plans to mitigate climate risk. Norway generates almost 100% of its electricity from renewable sources, primarily hydropower. Other leaders in renewable energy adoption include Sweden, Costa Rica, the UK, Iceland, New Zealand and Germany, etc.

A lesser known, but much bigger investment plan, is Japan’s Green Transformation (GX) policy worth JPY150 trillion (over USD1.1 trillion) to be executed over ten years. It was announced in February 2023 with many detailed targets across energy, transport, construction, industry and finance. Its goal is to achieve carbon neutrality by 2050 and transform the country’s economy toward clean energy.

In our Sustainable Global Small Cap Strategy, clean energy and sustainable infrastructure are among the major themes. We have witnessed the strong growth of some holdings benefiting from these mega trends. Below are a few examples:

- Boralex Inc. (BLX CN) develops, builds and operates renewable energy power facilities (wind, hydroelectric, solar and thermal). It owns and operates about 100 wind power stations, 15 hydroelectric plants, a dozen solar power stations and two energy storage facilities. Its combined installed capacity has more than doubled in the past five years to over 3.1 GW, with 8 GW in the pipeline. Major markets are Canada, France, the United States and the UK.

- Aecon Group Inc. (ARE CN) is a Canadian construction company, providing a range of services to private and public sector clients in infrastructure, mostly in North America. In 2024, 59% of its revenues and 78% of backlog were tied to sustainability projects from renewable energy (hydroelectric, geothermal, solar) to energy transition (nuclear, battery storage, energy transmission and grid modernization) and water management (supply, distribution and wastewater treatment). As of March 31, 2025, it had a record-high backlog of CAD9.7 billion.

- Nexans SA (NEX FP) is a global leader in cable systems and services. It is strategically focusing on the electrification market. 75% of sales generated from products and services contribute to energy transition and efficiency. Well-known for its high-voltage transmission cable and subsea cable, Nexans specializes in power generation, transmission, distribution, infrastructure, telecommunication, mobility services and more. As of March 31, 2025, it had a record-high backlog of EUR8.1billion. Major markets are Norway, France, Germany and Canada.

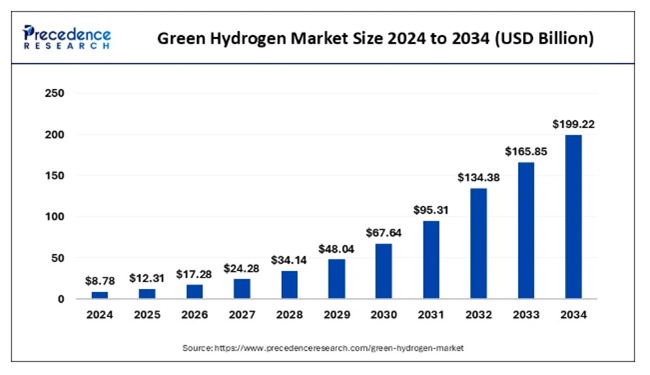

Within the theme of sustainability is the growing industry of green hydrogen. The global green hydrogen market size is currently estimated at over USD12 billion in 2025 and is expected to expand at a CAGR of 41% from 2025 to 2034.

There are national policies in place that favour green hydrogen: Germany’s hydrogen strategy targets at least 10 GW production of green hydrogen by 2030; the UK’s hydrogen strategy requires at least half of its 10 GW target to come from green hydrogen by 2030; Japan’s hydrogen strategy focuses on achieving carbon neutrality by 2050 through the widespread adoption of hydrogen across various sectors.

There are three main types of electrolysis used for green hydrogen production: Proton Exchange Membrane (PEM), Alkaline and Solid Oxide. Advantages of PEM electrolysis specifically are that it uses a solid polymer electrolyte membrane and operates at higher current densities, making it suitable for dynamic and intermittent renewable energy sources. Major players in the PEM segment include Plug Power, Nel Hydrogen, Cummins and, one of our holdings, ITM Power PLC (ITM LN).

ITM Power is a pure-play in green hydrogen and manufactures electrolyzers based on PEM technology; it’s known for its work with Linde on large-scale PEM electrolyzers. Germany is its biggest market generating 37% of total sales, followed by the UK, Austria, Australia and rest of Europe.

Countries prioritizing initiatives for renewable energy, sustainable infrastructure and electrification will look to work with companies specializing in these sectors. We feel that the holdings within our Sustainable Global Small Cap Strategy are well positioned to benefit from this global effort toward a greener future.