The global pandemic has caused a sharp, worldwide economic contraction, with supply and demand severely affected across many industries. However, the real estate market was one of the few to experience strong and sustained growth in 2020 and 2021. House prices rose consistently, driven by robust demand and constrained supply.

On the demand side, buyer interest has surged since summer 2020, as people are scrambling to take advantage of low mortgage rates due to fear of missing out. According to the Mortgage Bankers Association (MBA), in the United States (US), the value of mortgage originations for new purchases increased by 13% in 2020, in comparison to 2019, despite the fact that most economic activities were effectively halted in April and May 2020. As America’s biggest generation, millennials have entered their prime years of purchasing power, driving the demand for houses even further. On top of that, as people spend more time at home during the pandemic, demand for bigger spaces increased significantly.

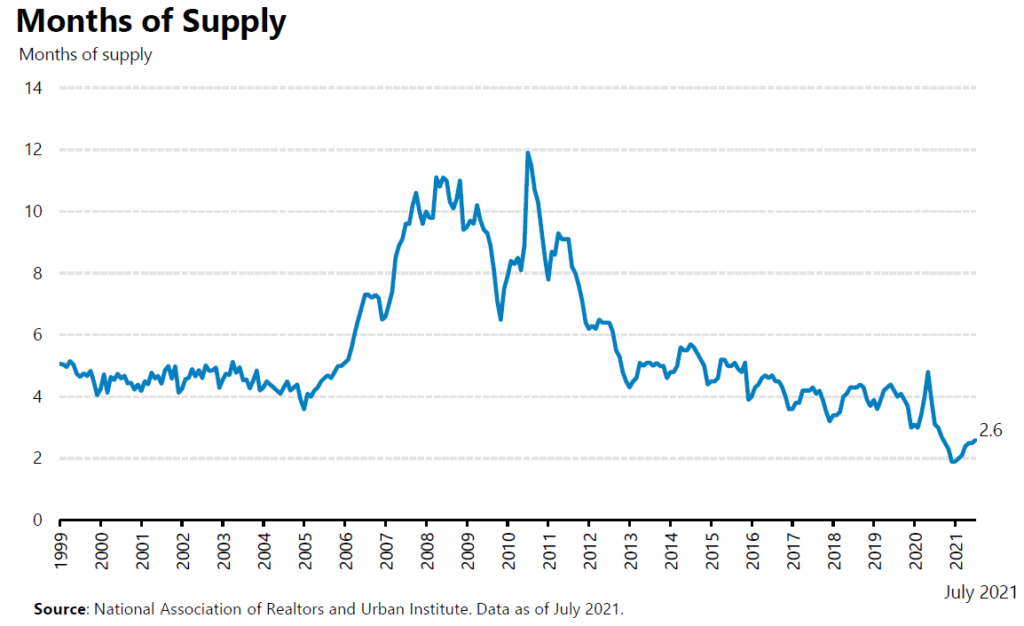

On the other hand, supply has been extremely tight. In the US, months of supply in July 2021 was 2.6, which is an increase from the record low of 1.9 in January 2021, but still at a historically low level. Historically, a balanced market has been defined as 6.0 months of supply. Even before the pandemic, there was a shortage of homes for sale. From 2010 to 2019, the US had the lowest number of homes built than any other decade since the 1960s.[1] From 2010 to 2019, only 5.8 million homes were built, compared to over 27 million homes built from 2000 to 2009. Strong demand for housing in recent years, fueled by low mortgage rates, has exaggerated the imbalance of supply and demand. As a result, house prices keep going up.

The strong residential market is not limited to the US. In the United Kingdom (UK), house prices have been increasing consistently since May 2020. In June 2021, the average house price was £266,000, up 13.2% year over year and 4.5% month over month. This is partially due to the stamp duty holiday introduced in July 2020 to help homebuyers and boost the UK property market during the pandemic. Even though the stamp duty holiday will gradually taper from July 2021, demand still outstrips supply, and prices are expected to stay on the upward trend. One of our holding companies, Savills (SVS LN), has been benefiting from this trend. Founded in 1855, Savills is one of the world’s leading property service providers for both residential and commercial properties. They have a dominant position in many markets across the globe, with more than 600 offices across the Americas, Europe, Asia Pacific, Africa, and the Middle East. In the first six months of 2021, Savills hit record profits thanks to the hot UK housing market, with revenue in the country having increased by 40% year over year.

This housing boom has been positive news for homeowners; CoreLogic analysis shows homeowners with mortgages (roughly 62% of all properties) in the US have seen their equity increase by a total of $1.9 trillion since the first quarter of 2020, an increase of 19.6% year over year. However, it has also reduced housing affordability, and shut a growing number of people out of the housing market. In the US, homeownership has been falling after its previous peak of 69% in 2004.[2] In the second quarter of 2021, homeownership dropped to 65.4%, which is 2.5 percentage points lower than in Q2 2020. The rate varies significantly by race, with the biggest gap observed between non-Hispanic white households and Black households, homeownership rates for which were 74.2% and 44.6%, respectively. If the trend continues, the US homeownership rate will decline to 62% by 2040.

Therefore, it is crucial to increase the supply of affordable homes to meet the needs of future homeowners and renters. Century Communities (CCS US), a top ten national homebuilder and a holding company in our portfolios, focuses on affordable homes. Entry-level buyers represent 80% of their total deliveries. A total of 43% of the homes are under the price of US $250,000, and close to 90% of homes are under the price of US $500,000. In the second quarter of 2021, the company’s home sales revenue increased by 34% to a record $1 billion, and net income increased by 207% to a record $117.9 million. The company has increased their revenue guidance for 2021, and remains confident in its success in the second half of the year.

It’s not just the home buyers, renters also faced a significant amount of financial stress. In the first quarter of 2021, 17% of all renter households in the US reported being behind on rent. This rate is 21% for Hispanic and 29% for Black renters. Several companies in our portfolio contribute to the rental market’s affordability.

Boardwalk Real Estate Investment Trust (BEI-U CN) is one of Canada’s largest multi-residential real estate owners and managers. Founded in 1984, the company owns 33,513 residential suits, concentrated in Alberta, Quebec, Saskatchewan, and Ontario. The REIT is committed to providing the best product quality and experience to their clients, at affordable prices. The average rent is approximately 20% of the average renter’s household income. Thanks to its strong brand of service at affordable prices, Boardwalk has been gaining market share, and maintained an above-market-average occupancy rate.

SBB (SBBB SS) is a Swedish-focused, social infrastructure property company. Of its portfolio, 94% is in rented residential and social infrastructure, including education, senior care, healthcare, and government/municipal buildings. The government backs 88% of the rent. As of Q2 2021, the company invests 27% of its social assets in affordable housing. The average rent levels for SBB’s rent-regulated residential portfolio is about 40% below the rent levels of new productions.

Advance Residence (3269 JP) is the largest residential REIT in Japan. They focus on compact apartments, mainly in Tokyo metropolitan areas; 64% of its portfolio are studio and one-bedroom properties, the rents for which are more affordable. Over 50% of the rents were below JPY 100,000 per month (approximately US $911). As a comparison, a typical mid-range, two-bedroom apartment in Tokyo is about US $1903 per month, according to a Deutsche Bank report.

Affordable housing is part of Goal 11 of the Sustainable Development Goals (SDGs). It’s also central to achieving almost all of the SDGs. The demand for affordable housing keeps growing, given the trend of urbanization and population growth. Investment in this theme will not only allow us to ride the secular trend, but also contribute to a more sustainable and inclusive future.

[1] https://www.statista.com/statistics/1041889/construction-year-homes-usa/

[2] As defined by the US Census Bureau, the homeownership rate is the proportion of households that is owner-occupied.