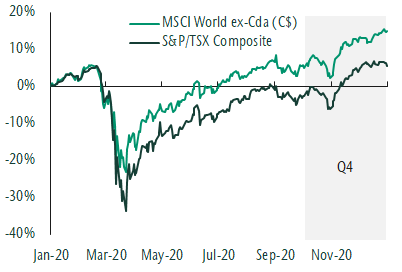

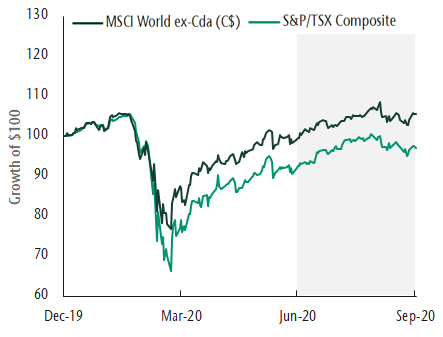

Markets overview

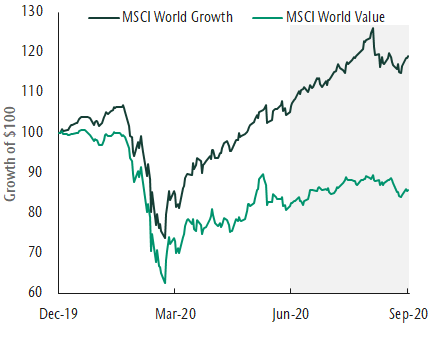

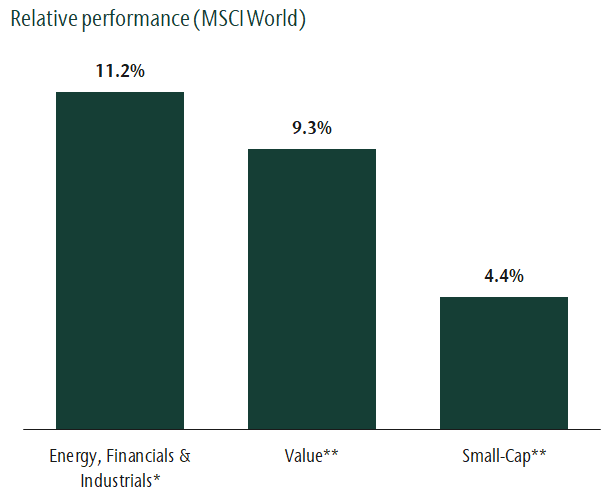

Equity markets reached new highs this quarter as virus cases declined and market signals suggest that the global economic recovery remains strong (despite lockdowns). Support for the recovery has come in the form of monetary and fiscal stimulus and in March the US passed another significant fiscal package. This quarter the S&P/TSX Composite Index was up 8.1% and the MSCI World ex Canada (C$) advanced 3.5%. Stronger performance from the Canadian market reflects a higher weighting to cyclical sectors like energy, financials and industrials which have benefited from an acceleration in global growth expectations. Within equity markets value and small-cap stocks have outperformed which is a rotation away from areas that performed well for most of 2020.

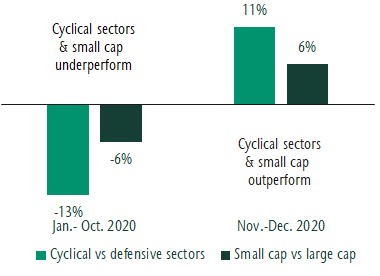

Stocks led by economically sensitive segments

*Energy, financial and industrial sector average return less the average return of the remaining sectors. **Returns are relative to the growth and large-cap benchmarks, respectively, using corresponding MSCI World benchmarks. Quarterly return ending March 31, 2021. Source: MSCI, Refinitiv

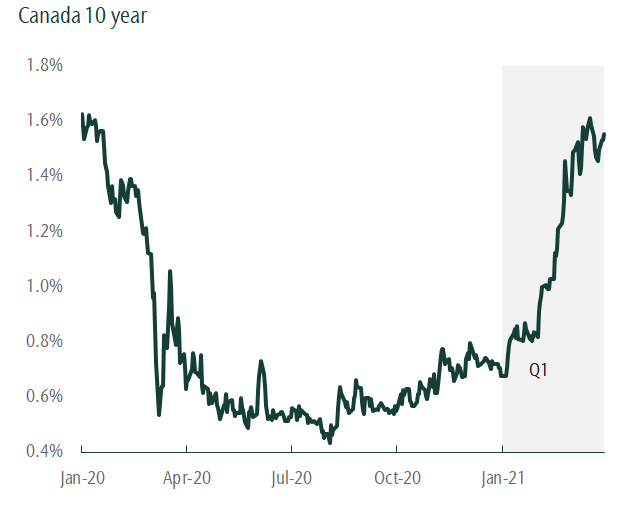

Bond yields rise

Stronger economic growth and accommodative policy led to a selloff in bonds and a spike in yields across maturities. The result of increased yields was a negative return for the FTSE Canada Universe Bond Index of -5.0%, the worst quarterly performance since the first quarter of 1994. Government and provincial bonds were most affected while declines in corporate were more muted.

Our thoughts

We believe the global economy and corporate earnings will continue to recover as more businesses gradually resume normal operations and government stimulus provides continued support. Portfolios are positioned to benefit from this improving outlook. As such, our asset mix positioning remains overweight equities. However, strong performance from equities relative to bonds led us to rebalance this quarter to maintain our desired exposure. Within equities we have an overweight to small-cap stocks and maintain an allocation to value stocks. This quarter we also increased our emerging markets position. Within bonds, allocations to short bonds and high yield have protected portfolios in a period of rising yields. This asset mix positioning has served us well this quarter and remains attractive in the current environment.

Our portfolio management teams have selectively positioned portfolios to more cyclical assets that are expected to benefit from continued improvements in the economy. Our equity teams have taken gains in some businesses that have benefited from COVID-19 and bought companies that can outperform in a more positive investment environment. This includes companies within the financial sector as well as the travel and leisure industry. Within bond portfolios we are overweight credit, inflation-protected debt and have lower sensitivity in the portfolio to changes in yield. Although our overall positioning in portfolios reflects a positive outlook we remained well diversified.

From the desk of Jeff Guise, Managing Director, Chief Investment Officer, CC&L Private Capital.

This post is for information only and is not intended as investment advice. The views expressed are those of the author at the time of publication and are subject to change at any time.