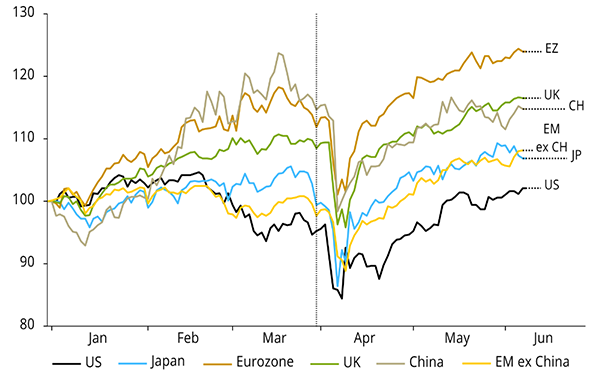

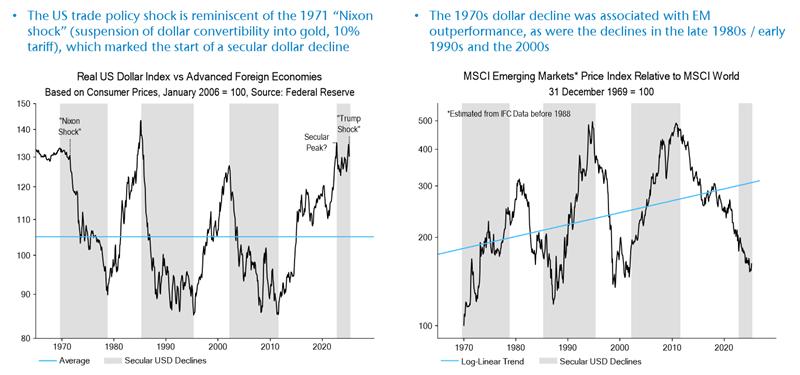

We called for a brighter outlook for EM equities over a year ago on the prospect of a USD bear market. This is now starting to play out, led by a liquidity-driven bull market in China.

Over the last three years to the end of the quarter, EM equities have compounded at an annualised rate of 19%.

Our markets remain under-owned and boast cheap valuations relative to US stocks. Easing financial conditions should support a recovery in earnings growth.

We are also believers that you can have too much of a good thing, and that emerging markets are a host to a number of attractive structural thematics outside of the AI fervour that are unique to our investment universe.

The rally this year has been focused on the large cap names. To illustrate, the MSCI EM Small Cap Index has returned 16.67% against 28.16% for the large cap index for the year to date.

This is also reflected in the underperformance of smaller and less liquid markets such as ASEAN. As the bull market matures, we expect liquidity to creep out to markets such as Malaysia, which have been abandoned by foreign investors despite having exciting structural investment opportunities. We know from past experience that when investor flows do return, the upside can be dramatic.

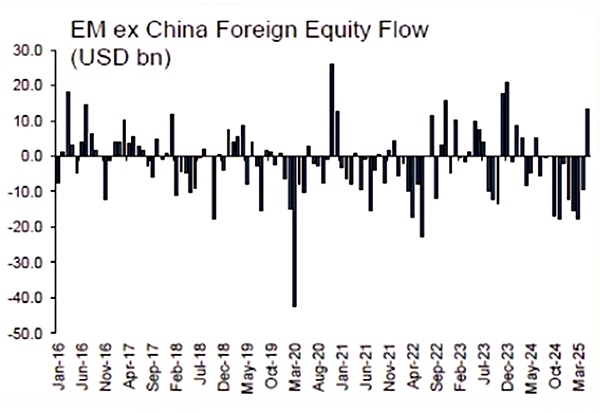

Returns across emerging markets have so far been driven by local allocators, with foreign investors largely sitting on the sidelines – although interactions with attendees on our usual conference circuit suggest that this could be about to change.

Korea Value-Up deep dive: SK Square

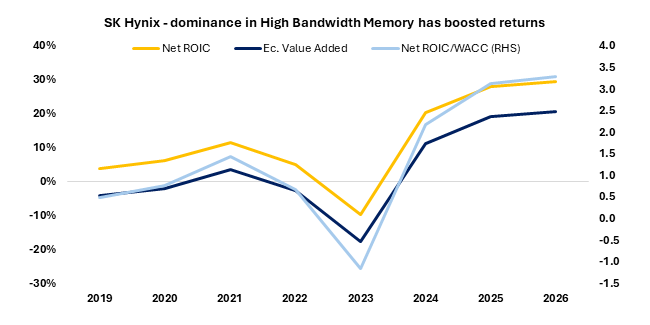

Corporate Value-Up catalyst alongside tailwind from SK Hynix’s dominance in high bandwidth memory

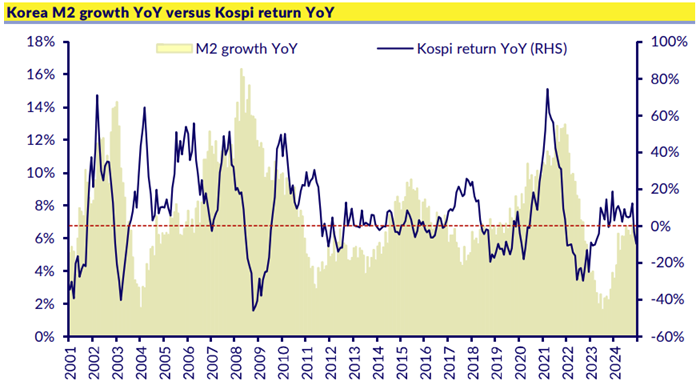

South Korean equities have surged by over 57% this year to the end of September. The fuel is a combination of exposure to AI infrastructure mania through the country’s tech giants such as SK Hynix and Samsung rallying, ultra cheap valuations and the prospect of a broader market re-rating courtesy of the Value-Up corporate reform drive that is now underway.

Below we provide a deep dive into recent portfolio addition SK Square, which we think is emblematic of the broader upside potential in Korean equities if the government sticks to its reform ambitions.

Overview

South Korea is home to some of the world’s most innovative companies, and yet it is also arguably one of the cheapest equity markets. The dichotomy is down to a poor history of corporate governance in the country, with the economy dominated by vast family-controlled chaebol conglomerates.

These families have historically been more focused on preserving their business empires than looking out for the interests of minority shareholders. However, following in the footsteps of Japan’s stock exchange reforms, South Korea has launched Value-Up to narrow the “Korea discount” and attract foreign capital.

We think SK Square epitomises the sort of opportunity where Value-Up could be a significant catalyst for re-rating. Spun off from SK Telecom in 2021, the holding company’s investment portfolio includes business across semiconductors (SK Hynix), ICT ventures and digital platforms.

Source: SK Square 2025

Focus on the discount to NAV for this holding company – the discount has widened to 55% following a recent correction. This was an opportunity to buy. Management has levers to pull to narrow the NAV discount via more share buybacks, NAV enhancement and dividend payouts.

SK Square is the best in class among the holding companies and is leading peers in efforts to enhance shareholder value. Management quality is high and the board has a majority of independent directors. They were the first holdco to unveil their Value-Up program and appear to be executing the plan well.

The company is already practising cumulative voting rights – this favours minority shareholders who can pool votes to secure board seats (only 6% of companies in South Korea practice cumulative voting).

The disposal of non-core assets will enable SK Square to focus its energy on its best assets in the IT and Communications sectors.

A brief history of the chaebols

Born out of the interplay of historical, economic and governmental forces following WWI and the Korean War, these family-owned conglomerates filled a significant institutional void post Korea’s liberation from Japanese occupation in 1945.

Chaebols were formed out of the sale of assets previously owned by Japan’s government and firms, which accounted for 30% of the Korean economy. These assets were often sold to families and high-ranking officials at a deep discount, with prices based on outdated book values amidst high inflation. Early chaebols like Hanwha, Doosan, Samsung, SK and Hyundai used these assets as the foundation for growth.

The Korean government played a decisive role in shaping the economy since 1961. Under President Chung Hee Park, economic development became a top priority for legitimacy. The government launched a series of five-year development plans which were based on nationalising banks and channelling foreign loans in capital-intensive heavy industries and chemical industries. It allowed chaebols to acquire or establish non-bank financials to provide capital to their affiliates.

Korea experienced chronic capital shortages throughout its development period, particularly after the Korean war. The chaebols could create value by internalizing resource allocation and replacing poorly performing institutions. The absence of supporting industries meant that chaebols often had to vertically integrate to secure necessary parts and raw materials.

While the chaebols were effective vehicles for kickstarting growth, a host of structural issues emerged.

Vertically integrated suppliers, with captive customers, meant the chaebols lacked incentives to be efficient.

Cross-subsidisation across affiliate businesses led to yet more inefficiencies and wasteful allocation of capital.

Internal subsidies via nonbank financial subsidiaries funded unprofitable ventures bypassing traditional banks. This was identified as one of the causes for the Asian Financial Crisis.

Centralised family control over numerous group affiliates even though their direct equity ownership is often a small percentage. This control allows for decisions that serve personal interests at the expense of minority shareholders.

Cross-shareholding – affiliates within a chaebol group own shares in each other, which inflates the apparent ownership stakes and provides a mechanism for the founding family to control the entire group with minimal actual capital investment.

High debt-equity ratios. Chaebols have historically preferred debt over equity financing to avoid diluting the controlling stakes of their founding families.

Unchecked power of chairmen. Chairmen held absolute power over strategic decisions, leading missteps such as ill-conceived diversification strategies e.g., Samsung’s entry into the auto industry.

Ineffective boards. Typically dominated by executive officers and outside directors with close ties to dominant shareholders. They often serve to provide ex-post factor approval rather than independent oversight.

Value-Up aims to tackle these issues, and it is more than just political rhetoric.

The program is supported by both of South Korea’s major political parties in the DPK and PPP. Real reform is underway, including revisions to the Commercial Act mandating director loyalty to shareholders (instead of to “the company”), electronic shareholder meetings for large firms and cumulative voting rights to empower minority investors.

Corporate governance reform – Japan vs. Korea

| South Korea | Japan | |

|---|---|---|

| Mandatory vs. voluntary | Voluntary | Mandatory |

| Incentives | Carrots and sticks | Named and shamed |

| Targeting companies with price to book ratio <1 | Financial Services Commission believes PBR helps assess whether or not the issue arises from a low ROE due to a high cost production structure and decrease in market demand. | The company has not achieved profitability that exceeds its cost of capital, or investors are not seeing its growth potential. |

| Framework | A Value-Up ETF Index has been created. Value-Up adherents to be rewarded with inclusion.

Potentially, a special tax regime will be set up for companies increasing dividends. |

Companies complying with the new corporate governance rules were publicly named by TSE in early 2024. |

History of SK Square

Founded in November 2021 via a spin-off of SK Telecom, SK Square intended to focus on ICT investments and become a more growth-and-tech-focussed holding company.

The downturn in portfolio company and DRAM giant SK Hynix in 2023 forced SK Square management to sharpen its focus on the underlying portfolio, much of which was loss making.

SK Group chairman Chey does not have a direct stake in SK Square and the independent board of directors makes it more exposed to shareholder activism. It was the subject of shareholder activism in 2023–2024, led by a London hedge fund (1% shareholding), pushing for the business to release an industry-leading value-up plan which was eventually announced in November 2024.

Company overview

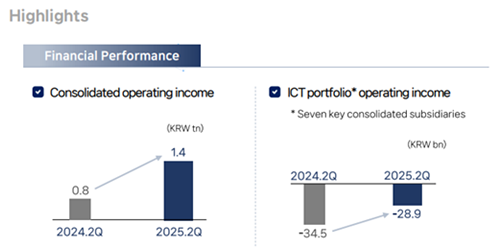

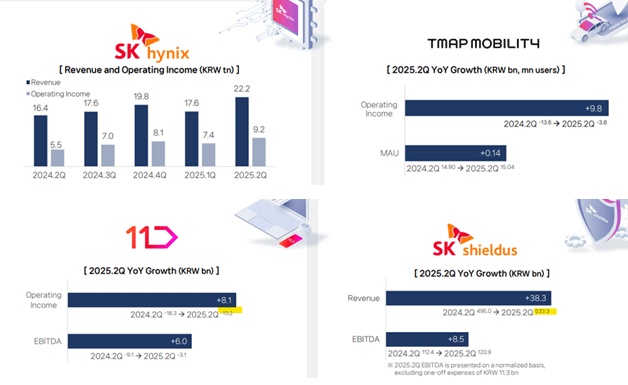

- Operating income (Q2 2025) of 1.4tn won, of which SK Hynix contributed to 1.84tn (20% stake). The ICT portfolio is generating negative operating income of 28.9tn won.

Source: SK Square company presentation Q2 2025

- SK Hynix is 88% of SK Square NAV.

- Other than SK Hynix, SK Shieldus (2% NAV) and TMAP Mobility (1%) are the only ventures making meaningful profits.

- Management said that they will divest 20 or more ventures this year, and the rest in the next couple of years.

Source: SK Square company presentation Q2 2025

SK Square’s NAV discount is beginning to narrow. A recent market correction has given us an opportunity to buy the stock.

- NAV to market cap discount has narrowed significantly from 74% in 2022 to 66% at Q3 2024 since the announcement of its value-up program.

- The discount narrowed to a low of 47% in June, before the KOSPI and SK Square correction.

- While SK Hynix corrected by c.15% from its July peak, SK Square’s share price fell by c.37% from its June peak, with the NAV discount widening to c.55% at the time we initiated our position.

| NAV Discount | 28/08/25 |

|---|---|

| NAV | 44,198 |

| Market cap | 19,828 |

| -55% | |

Catalysts

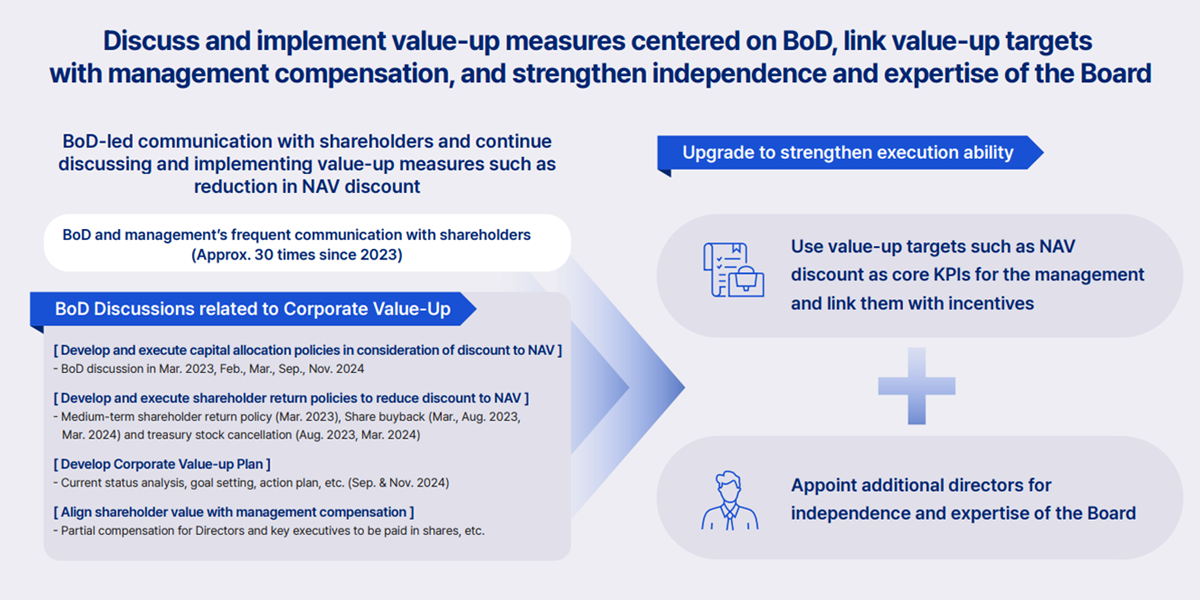

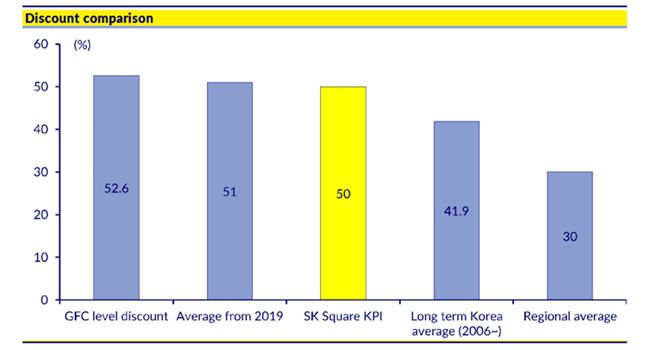

There are strong KPI incentives in place for management if the NAV discount gets to 50%, ROE> Cost of equity at 13-14% and over 1x PB by 2027.

Source: SK Square company presentation Q2 2025

The NAV discount has been narrowed by:

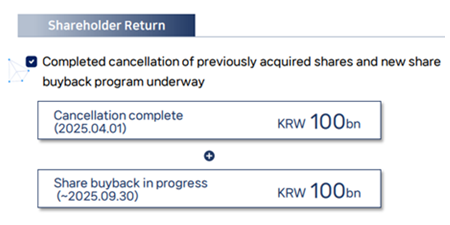

1) Aggressive share buybacks (c.9% of total outstanding). Critically, all shares bought back are to be cancelled. At the March AGM, another batch of buyback of 100bn won was announced on top of the 300bn and 200bn buybacks in 2023 and 2024.

Source: SK Square company presentation Q2 2025

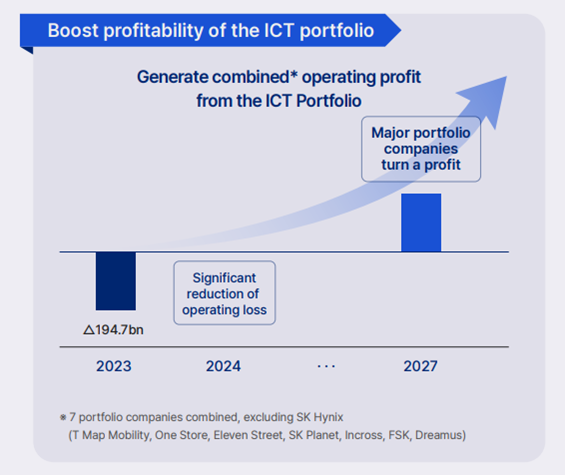

2) Non-core divestments by reducing the number of entities from 43 to 20 this year. They are hoping to de-risk the portfolio, boost cash flows and shareholder returns.

Source: SK Square company presentation Q2 2025

3) Payout of at least 50% of recurring portfolio dividend income to investors.

Source: SK Square company presentation Q2 2025

Our base case is for NAV discount to narrow to 40% over medium term, the historic average of holdco discounts in South Korea.

Source: CLSA, DART

Narrowing the discount to this level implies significant upside in the stock.

In addition, dividends from SK Hynix will amount to 3tn won by 2027, which can be deployed.

They have sold an SK Shieldus (Cybersecurity) stake to a PE fund and the cash received in Q3 2025 (510bn won) could be deployed to further boost shareholder returns.

For the remaining unlisted companies, management is yet to outline plans for further asset sales. More clarity here would boost the stock.

Additional tailwinds may come from the next batch of share buybacks to be announced in Q4. The pace and magnitude will be key. SK Hynix coming back in focus as an AI play is an added tailwind.

Risks

- The board of directors may not go as far as investors expect to sustainably narrow the NAV discount from 75% in 2022 to 50%.

- Disappointment over the cadence and magnitude of share buybacks.

- Chairman Myung is trying to turn some portfolio companies around to be EBITDA positive, but the labour union is in the way. (We are still seeing some progress i.e., portfolio company TMAP turned an operating profit in Q2 2025).

- The pace of divestments could be slower than anticipated, as assets require proper packaging to sell them at a good valuation.

- Volatility in the stock adding to beta to the portfolio.

- An SK Hynix downcycle and share price downturn will trigger a bigger correction in SK Square.

Summary

Overall, SK Square is just one example of how South Korea’s Value-Up program can act as a catalyst for managers to sharpen up capital allocation and sweat their assets harder. Much will depend on the government’s willingness to pressure corporates to continue value-enhancing efforts through further legislative and regulatory reform. The momentum is positive, and if sustained could lead to a full market re-rating.

Source: NS Partners and LSEG (May 2025)

Source: NS Partners and LSEG (May 2025) Source: LSEG Datastream

Source: LSEG Datastream