In 2013, the investment world was introduced to the term FANG by CNBC’s Mad Money host. Of course, we all know the tech giants represented by this acronym: Facebook, Amazon, Netflix, and Google.

Almost a decade later, the term FANG is back in the news. But this time around, the almighty tech companies have been dethroned by four of the most traditional, old school industries in the world. We’re talking about Fuel, Agriculture, Natural Resources, and Gold.

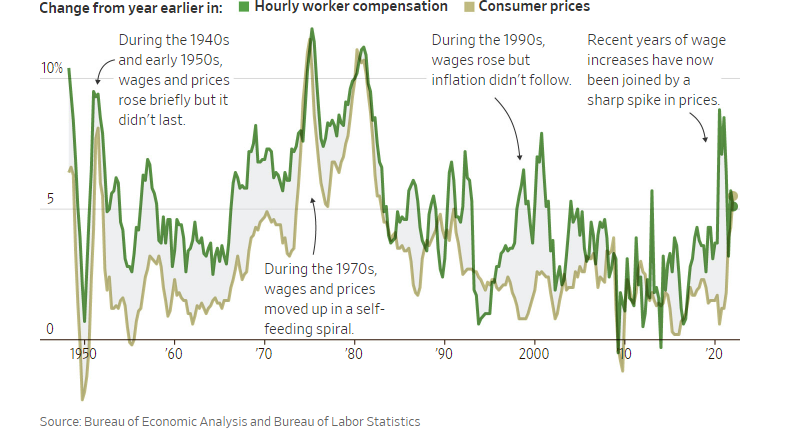

Historically every time this group took the lead in the last century (1939, 1972, 2000), we have seen inflation skyrocket for years to come, leading to political unrest around the world and major corrections in financial markets. We are set to see history repeat itself once again.

In today’s weekly we focus on agriculture, which is heading into a super cycle.

Time and time again, the agriculture industry has weathered economic uncertainty. No wonder it’s one of the oldest, most reliable asset classes. It is also one of the best inflation hedges as food prices are closely linked to inflationary trends.

How big is the agriculture industry?

American farms alone contributed $124 billion in United States (U.S.) gross domestic product in 2020. Farmland is still an unknown asset for many, and the largest farmland owner in the U.S. is not even a farmer. It’s Bill Gates, who currently owns 242,000 acres of land. Isn’t it ironic that one of the world’s biggest tech company founders sees more value in dirt? Clearly this is an indicator that land is about to get a lot more valuable.

Globally, agriculture is a large and growing industry worth over $10 trillion in 2020. It is expected to increase to $12 trillion in the coming years.

The drivers for this growth are simple:

- an ever-expanding global population,

- urbanization, and

- transition towards regenerative sustainable farming.

Russia/Ukraine impact on global Agriculture

The war in Ukraine has delivered a shock to global energy markets. Now the planet is facing a deeper crisis: a shortage of food. Since the invasion last month, wheat, barley and fertilizers have seen prices increase over 20 percent.

With a cultivation of about 32 million hectares of land, Russia and Ukraine supply a quarter of the world’s wheat and half of its sunflower products.

Ukraine is known as the “breadbasket of Europe” thanks to its perfect climate and ideal geology for agriculture. Over 70 percent of the landscape consists of fertile plains with deep rich soils. Ukraine has warm summers, cold winters, and plenty of rain, providing excellent conditions for plant growth, and disease and pest prevention.

An unstable Ukraine = Another Arab Spring?

Ukraine is the world’s fifth-largest producer of corn (maize), and the eighth-largest producer of wheat. Approximately 12% of Ukrainian corn is sold to Egypt. It accounts for 80% of Lebanon’s and 25% of Egypt’s wheat imports, and is a leading supplier for countries like Somalia, Syria and Libya. It should come as no surprise that the current conflict will push up commodity prices even further.

Most Middle East countries use the Black Sea for trade. However, due to the war in Ukraine agriculture supplies (and all other products) have to travel a different route – which given current fuel prices will only increase the freight cost. Supply shortage and an expensive freight will further compound price inflation in the Middle East.

When we look back to 2009/10, food prices were one of the main triggers of the Arab Spring uprisings in the Middle East. Back then, social unrest started in Tunisia, which saw its authoritarian government fall in less than two weeks. Then the crisis hit countries like Egypt, Yemen, Libya, Syria, and Saudi Arabia. In the chart below we can see that food prices have already exceeded levels last seen in 2011. We could be looking at another round of instability in the middle east.

Portfolio impact

Our portfolio is extremely well positioned to benefit from both high inflation and opportunities in the fast growing agriculture industry.

When it comes to inflation, smaller companies generally outperform their larger peers. From January 1979 to July 1983, the Russell 2000 Index outperformed the S&P 500 Index by 81% (see chart below). During this time, inflation rose to as high as 13% and the economy suffered a double-dip recession in 1980 and 1981-82, before staging an extremely strong recovery in 1983 with growth rates as high as 8.5%.

In the agriculture industry, we own the following names which we believe will grow faster than the industry and deliver superior earnings.

Limoneira (LMNR)

Founded in Ventura County, California in 1893, Limoneira is one of the largest growers and marketers of lemons in the U.S. It is also the largest grower of avocados in the U.S. Besides the steadily growing agribusiness, Limoneira’s strategy is to unlock the value of over 10,000 acres of agricultural land, real estate development opportunities and water rights mainly in Southern California.

Titan Machinery (TITN)

Titan Machinery is the largest Case New Holland dealer in the U.S. with 75 stores, mainly in the Midwest, and some in Eastern Europe. According to the U.S. Department of Agriculture (USDA), net farm income is 26% higher than the 10-year average. Farm income is forecasted to reach its highest level since 2013. This bodes well for equipment upgrade cycles in general. Also, drought in South America is causing a shortage of soybeans and corn. U.S. farmers are now focusing on these crops and should see higher incomes well into 2023.

Lindsay Corporation (LNN)

Based in Omaha, from its humble beginnings as a small operation in rural American Midwest, Lindsay has become a global leader in irrigation and infrastructure. Their irrigation and water management solution should see strong take rates by farmers.

Farmland Partners (FPI)

Farmland Partners is a real estate company that owns approximately 160,000 acres of high-quality farmland in 17 states. Their land is being farmed by over 100 tenants who grow 26 major commercial crops. Farmland should benefit not only from increased rent, but also some profit share agreements on certain properties.

Bucher Industries AG (BUCN)

Bucher is an internationally operating Swiss engineering group. Bucher’s divisions are focused on specialized agricultural machinery, municipal vehicles, hydraulic components, manufacturing equipment for the glass container industry, as well as equipment for processing of beverages.

Sakata Seed (1377)

Based in Yokohama, Sakata is a leading seed company in Japan. Sakata ranks in the top three for vegetable and flower seeds in Japan, and number six in the world. They have a product lineup of 1700 flower varieties of 100 species and 400 vegetable varieties (mainly broccoli, cabbage, carrot).

Meanwhile, Global Alpha is back on the road again. In less than a month, we will be visiting holdings like Limoneira and Farmland Partners to evaluate their operations and performance. We have also begun visiting trade shows and have recently returned from the 43rd Annual Institutional Investors Raymond James conference in Orlando. We look forward to keeping you posted on new trends, opportunities, and ways we are generating alpha for our clients.