Jeff Wigle discusses Banyan’s 12-year partnership with Purity Life and the world of private equity on the Purity Pulse podcast.

Jeff Wigle discusses Banyan’s 12-year partnership with Purity Life and the world of private equity on the Purity Pulse podcast.

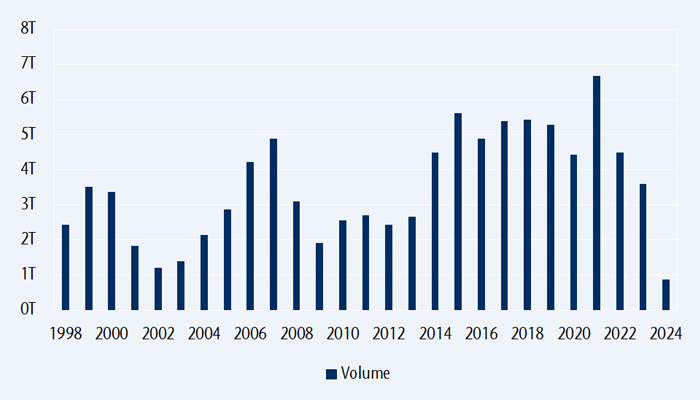

The fluctuation in mergers and acquisitions (M&A) activity in 2021 followed a typical cyclical pattern, echoing broader economic trends. The initial surge in M&A was propelled by low interest rates and a swift reopening from the COVID-19 pandemic that encouraged companies to pursue strategic acquisitions. This led to the highest M&A volumes since 2007.

However, several factors dampened the momentum in 2022-23. Aggressive interest rate hikes, rising inflation, geopolitical tensions such as the war in Europe, and an overall economic slowdown contributed to a decline in M&A activity. Additionally, decreasing confidence among C-suite executives and a wider bid-ask spread between buyers and sellers further reduced dealmaking.

As a result, total M&A volumes dropped by 18% to approximately $3 trillion in 2023, according to data from Dealogic. This marked the lowest level of M&A activity since 2013 when deal volumes were at $2.8 trillion, indicative of the challenges and uncertainties faced by global dealmakers amidst shifting economic conditions and geopolitical risks.

All of this changed when the Federal government started hinting about lowering interest rates in 2024. This week, we look at how this trend stands to benefit our portfolio.

Global M&A volumes

Source: Bloomberg

Despite ongoing macroeconomic and geopolitical uncertainties, signs are pointing to a potential turnaround for dealmaking in 2024. Three key factors support this optimism:

Global non-financial listed companies hold $5.6 trillion in cash, while private market investors possess $2.5 trillion in dry powder, providing substantial resources for dealmaking. Additionally, depressed small cap valuations along with structural factors such as advancements in AI, the transition to clean energy, innovation in life sciences, reshoring initiatives and geographic diversification are further driving demand for M&A.

The dismal performance of 2023, marked by the lowest completed M&A volumes in a decade relative to nominal US GDP, underscore the potential for a rebound in deal activity in 2024. So, how big can it get?

Based on Dealogic’s data, global M&A volume has averaged around $5.5 trillion per year since 2014. With corporations potentially aiming to catch up on the $2 trillion shortfall from the last two years, M&A volumes for 2024 could range from $5.5 trillion to about $9.5 trillion. Actual figures will depend on various factors such as economic conditions, geopolitical stability and corporate strategies.

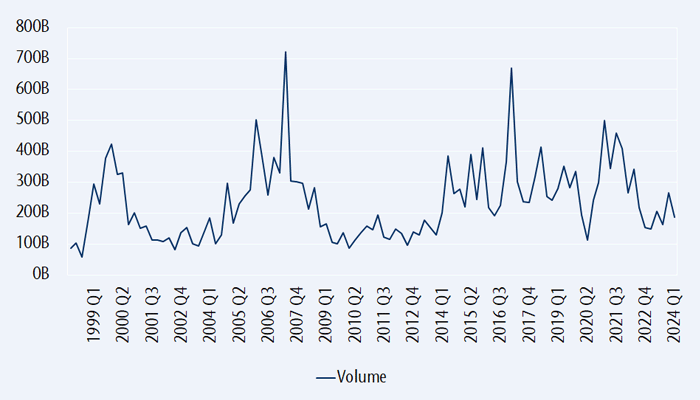

The underlying drivers are especially visible in markets like Europe that have seen a drought in M&A activity.

Western Europe M&A volumes

Source: Bloomberg

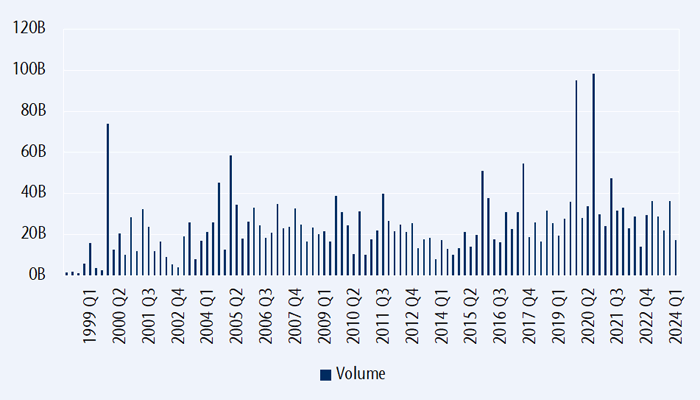

Looking at Japan, the structural shift towards greater corporate efficiency and activity is notable and expected to drive further M&A activity in the market. Despite the challenges faced by global markets, Japan has managed to maintain positive M&A volumes, demonstrating a resilience and proactive approach among Japanese companies.

Rising costs, stricter governance rules and mounting shareholder pressure are compelling companies in Japan to explore strategic options, including M&A. This trend is part of a broader effort to enhance corporate performance and unlock shareholder value.

Moreover, the potential wave of management buyout (MBO) activity in Japan is bolstered by recent reforms in the Tokyo Stock Exchange and guidelines by the Ministry of Economy, Trade and Industry (METI) for corporate takeovers. These reforms and guidelines are meant to promote shareholder earnings and increasing corporate value, aligning with the goals of enhancing efficiency and profitability.

For Japanese companies, especially those with lower capital efficiency, MBOs present an attractive way to streamline operations, improve governance and maximize shareholder returns. As a result, we can anticipate more M&A and MBO activity in Japan as companies adapt to evolving market dynamics and regulatory environments.

Japan M&A volumes

Source: Bloomberg

Many other markets like Australia, India, Korea and ASEAN are also expecting heightened M&A activity this year.

The accelerating M&A environment can be positive for smaller companies as their larger counterparts are willing to pay to acquire agile and innovative companies that can provide positive long-term growth perspectives. Furthermore, big companies seem to be diversifying by acquisition type. Larger, maturing companies can lack the same innovation capabilities as small companies to adjust, create and develop faster due to their nimble structure.

Another way to capitalize on this trend is by investing in a M&A advisory firm. These companies provide advice on corporate mergers, acquisitions and divestitures as well as debt and equity financing, acting as intermediaries in business sale transactions for either the selling company or the buyer.

We have profited from the M&A theme via Rothschild & Co., a France-based merger and acquisition boutique firm that has generated solid returns for our clients. Also, we recently initiated a position in Evercore, a name we have owned in the past and decided to repurchase because it is poised to outperform its competitors in the M&A space.

Founded in 1995, Evercore is an independent investment bank and asset manager, ranking #1 among independent firms and #4 among all M&A boutiques, including well-known players like Goldman Sachs. The company has a strong and liquid balance sheet, making it an excellent example of an investment that should benefit from the exciting uptick in M&A activity.

Michael Mormile, former Citadel portfolio manager, along with Jonathan Hartofilis and Richard Li, are partnering with Connor, Clark & Lunn Financial Group Ltd. (CC&L Financial Group) to jointly launch FortWood Capital (FortWood), a new emerging markets credit investment manager. In connection with the launch, CC&L Financial Group will provide seed capital along with investment from other clients.

FortWood seeks to capitalize on opportunities presented by structural inefficiencies in global emerging markets credit through a diverse portfolio of debt instruments. Michael Mormile explains, “Our approach combines thorough macroeconomic and fundamental analysis with a rigorous risk management framework to effectively manage the complexities of the emerging markets credit landscape and turn inherent market volatility into portfolio strength.”

FortWood’s absolute return and active long-only emerging markets strategies target corporate and sovereign external currency debt. These strategies are designed for clients looking to capture the attractive yields and value discrepancies found in under-researched markets.

“Partnering with Michael, Jonathan and Richard to expand into emerging markets credit is an exciting development for us. The FortWood team’s expertise in these regions and markets provides clients with the opportunity for additional diversification complementary to our existing offerings, along with potentially higher returns,” says Warren Stoddart, CC&L Financial Group’s CEO.

“By joining forces with CC&L Financial Group, we gain not only institutional operational support and global distribution but also a shared culture of excellence that will undoubtedly enhance our ability to focus on what we do best and achieve outstanding results for our clients,” says Michael Mormile.

This partnership, rooted in a strong team and shared principles, positions FortWood and CC&L Financial Group to exploit a growing asset class and new opportunities to deliver better client outcomes.

FortWood Capital specializes in actively managed emerging markets credit strategies. Leveraging its investment expertise and a robust risk management framework, FortWood navigates complex markets and challenging environments to uncover value. Headquartered in Greenwich, Connecticut, FortWood is a part of CC&L Financial Group. For more information, please visit fortwoodcapital.com.

CC&L Financial Group is an independent, employee-owned, multi-boutique asset management firm that partners with investment professionals to build and grow successful asset management businesses. CC&L Financial Group offers through its affiliates a wide array of traditional and alternative investment management products and solutions to institutional, high-net-worth and retail clients. With offices in the US, the UK, India, and across Canada, CC&L Financial Group has over 40 years of history and its affiliates collectively manage approximately US$90 billion in assets. For more information, please visit cclgroup.com.

Rebecca Jan

[email protected]

USA

Eric Hasenauer

[email protected]

Europe & EMEA

Carlos Stelin

[email protected]

Canada

Brent Wilkins

[email protected]

The quarterly commentary in mid-2023 noted that the cycle and monetary analyses were giving conflicting signals. The stockbuilding cycle appeared to be tracing out a low, a development usually associated with stronger performance of equities and other cyclical assets. However, greater weight was accorded to continued weakness in global real narrow money momentum, which suggested downside risk to economic activity and insufficient liquidity to support market gains.

The cycle signal has so far proved the correct one, with cyclical assets rallying strongly over the past five months. Monetary conditions have been more permissive than expected, probably reflecting continued deployment of “excess” money balances left over from the 2020-21 monetary surge, as well as unusual US deficit-financing operations.

What now? Valuations of some cyclical assets appear already to discount a solid and sustained economic upswing. Global real narrow money momentum has recovered slightly but remains negative, while the level of money balances may now be below “equilibrium”. Until money growth normalises, the risk is that an initial stockbuilding cycle recovery will prove disappointingly weak or even fail, with a retest of the 2023 low. A monetary revival, meanwhile, may have been pushed back by major central banks’ caution in reversing 2022-23 policy restriction, although an easing trend is under way in EM.

Commentaries in 2022 argued that the stockbuilding cycle was likely to bottom in 2023, probably in H2, based on the cycle’s 3.33-year average length and the prior low having occurred in Q2 2020. The possibility of an earlier trough was considered, on the view that the current cycle could be shorter than average to compensate for a longer prior cycle (4.25 years).

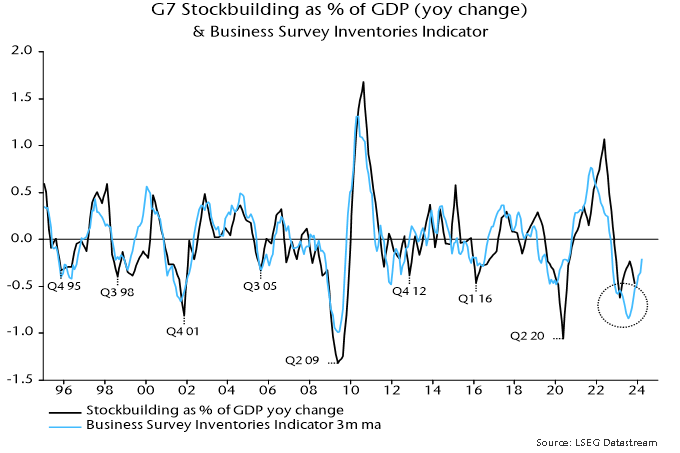

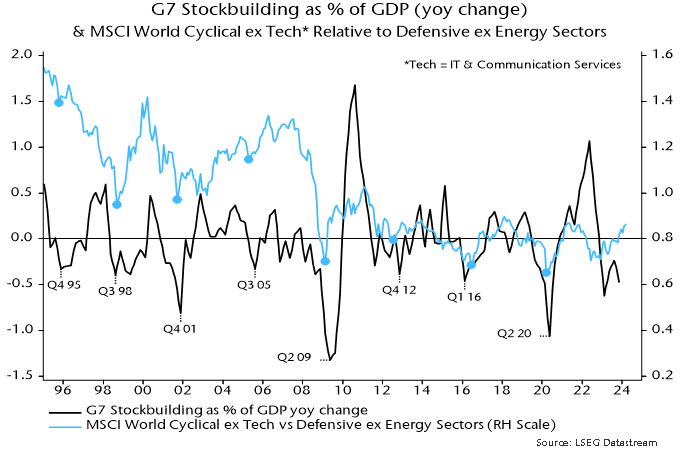

The key indicator used to monitor the cycle – the annual change in the stockbuilding share of G7 GDP – appears to have reached a major low in Q1 2023. A secondary indicator based on business surveys confirmed this trough in July – see chart 1.

Chart 1

Stockbuilding cycle lows historically were usually associated with nearby major or minor lows in cyclical asset prices. Chart 2 shows the relationship with the relative performance of equity market cyclical sectors, excluding IT and communication services. A cyclical rally gathered pace from April 2023, consistent with a H1 cycle trough.

Chart 2

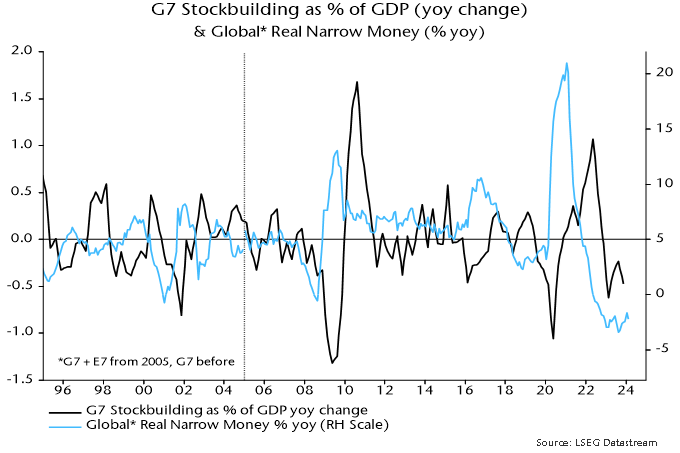

Why was a scenario anticipated in 2022 sadly underplayed in commentaries last year? The difficulty was that stockbuilding cycle lows historically were preceded by an upturn in global real narrow money momentum – chart 3. A marginal recovery in annual momentum occurred between February and June last year but a relapse to a lower low ensued. With no monetary improvement, and major central banks continuing to tighten into H2, it seemed unlikely that economic news and fund flows would support outperformance of cyclical assets.

Chart 3

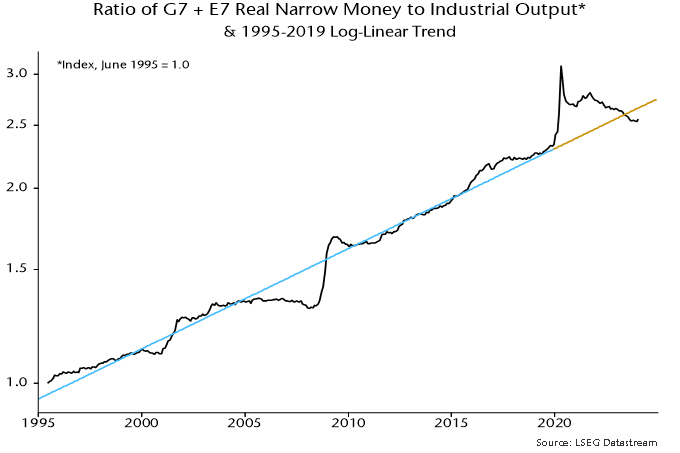

One explanation for the disconnect is that real money momentum, while a reliable indicator historically, failed to capture the availability of money to support activity and markets because of an overhang of “excess” balances created by earlier monetary strength. The ratio of the stock of global real narrow money to industrial output at end-2022 was still 4% above its steeply rising pre-pandemic trend – chart 4.

Chart 4

The strength of US equities may also have partly reflected the US Treasury’s decision, following the suspension of the debt ceiling in June, to “overfund” the federal deficit via issuance of bills, which were purchased mainly by money-creating institutions. This had the effect of more than offsetting the monetary drag from the Fed’s QT, while low coupon issuance created space in investors’ portfolios for additional purchases of credit and equities.

Support from these influences should be at or close to an end. The ratio of global real narrow money to industrial output returned to its March 2020 level in mid-2023, moving sideways since and now 4% below the pre-pandemic trend – chart 4. The Treasury’s financing plans, meanwhile, envisage a reduction in the bill float in Q2, raising the possibility of renewed monetary US weakness unless the Fed swiftly tapers QT.

Global real narrow money momentum has firmed again since Q3 2023 but remains negative, in both annual and six-month terms. A revival could, in theory, continue even if major central banks delay policy easing: rising economic confidence could be reflected in a switch out of time deposits and money funds into demand / overnight deposits, while EM money trends may improve further in response to recent policy easing. More likely, a normalisation of money growth will require a significant reversal of 2022-23 DM policy rate hikes.

Without a further rise in real money momentum, the initial stockbuilding cycle recovery may prove disappointingly limp or even fizzle altogether, revisiting the H1 2023 low. Such a scenario would pose a major risk to some cyclical assets now apparently discounting solid / sustained economic growth, such as the DM cyclical equities sector basket – chart 5.

Chart 5

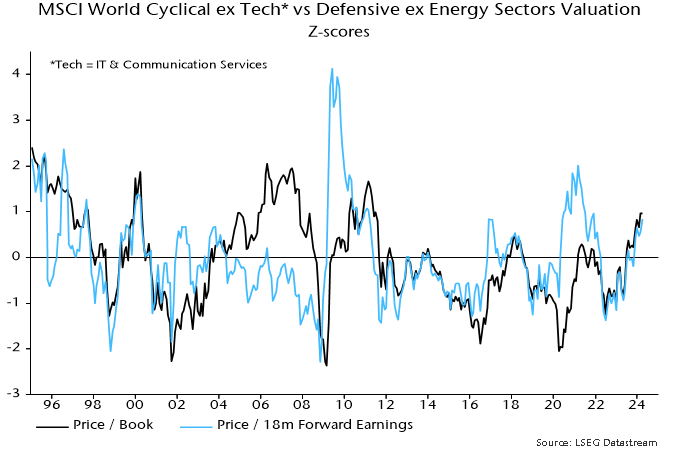

How could investors sharing the latter concern and favouring a defensive bias hedge against the possibility that a stockbuilding cycle upswing unfolds normally, implying economic acceleration into 2025? Some cyclical assets have lagged, including industrial commodity prices, the DM materials sector and EM cyclical sectors, which – unlike in DM – are at a low valuation versus defensive sectors relative to history.

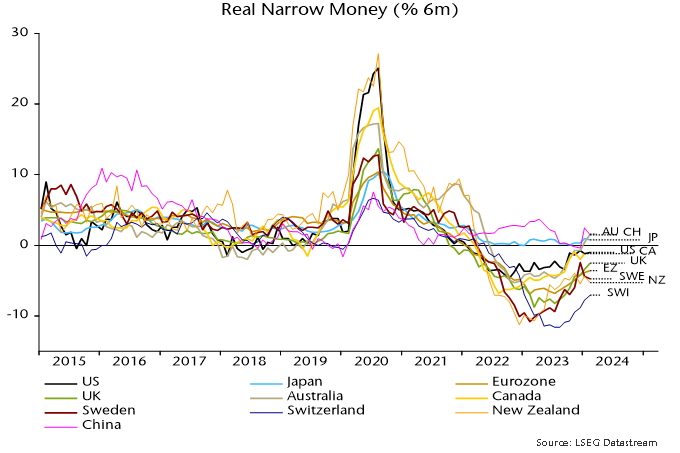

Chart 6 shows six-month real narrow money momentum in major countries. The US remains above Europe but the gap has narrowed, while, as argued above, the US recovery could go into reverse into Q2. The UK, meanwhile, has crossed above the Eurozone, suggesting improving relative economic prospects following GDP underperformance in the year to Q4.

Chart 6

China was a significant contributor to the recent rise in global real narrow money momentum, following record PBoC lending to banks in Q4. Such lending, however, contracted in January / February and a decline in term money rates has stalled, raising concern that the recovery in money growth will falter.

Other notable features include a pick-up in Australia, continued relative weakness in Switzerland and a relapse in Sweden. The suggestion is that the Australian economy will outperform, delaying rate cuts; by contrast, the Swiss National Bank has already embarked on easing, with the Riksbank expected to follow in Q2.

G7 inflation has continued to moderate in line with a simplistic monetarist forecast based on the profile of broad money growth two years earlier. A note in November 2022 suggested that annual consumer price inflation (GDP-weighted average), then at 7.8%, would fall below 3% by December 2023. The latest reading, for February, was 2.9%.

US annual core inflation on the Fed’s favoured PCE measure was 2.8% in February or 2.2% excluding lagging rents. Market concerns about inflation remaining “stubborn” are based on a rebound in shorter-term momentum measures but this has been mainly due to an outsized January gain, possibly reflecting residual seasonality (which could also explain unexpected weakness in late 2023), i.e. these measures are likely to fall back sharply as the January effect drops out.

G7 annual broad money growth continued to decline into April 2023, suggesting that the primary inflation trend will remain down into H1 2025. The reduction to date, however, was accelerated by post-pandemic normalisation of supply chains and weakness in commodity prices – the former effect is over and commodity prices usually rise during stockbuilding cycle upswings. The baseline view here remains that inflation rates will return to target by H2 2024 with significant risk of a subsequent undershoot and no sustained rebound before H2 2025.