This summer, markets have looked calm. Bond yields have been range-bound, interest rate and equity market volatility collapsed, credit spreads tightened and stock markets are again reaching their all-time highs. For many investors, it has felt like the tariff-induced storm had finally passed. But calm waters can be misleading. Beneath the surface, powerful undercurrents are shaping the outlook.

Bond markets are behaving as though disinflation is a sure thing and that rate cuts are guaranteed. Yet upstream pressures are bubbling again – producer prices, tariffs and unit labour costs all hint at inflation that may not go quietly. The risk lies not in what we see today, but in what the market may be ignoring.

Rates are trapped in a box

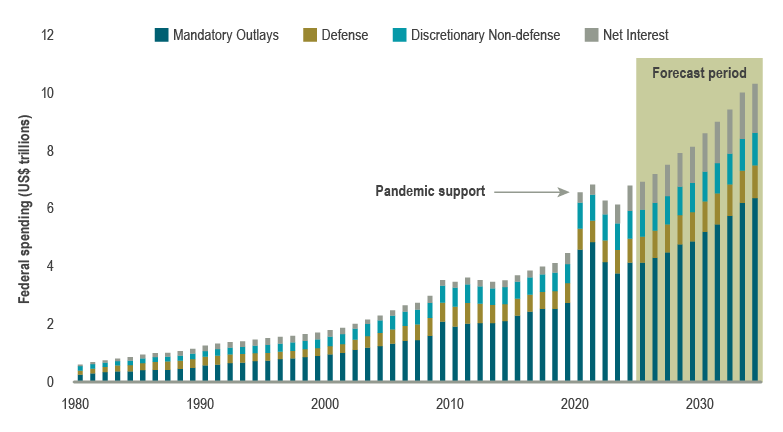

Interest rates are caught in a tug-of-war. On one side, politics, fiscal strategy and the general state of the US economy all limit how high yields can go. That is, the US Treasury’s preference for short-term bill issuance (rather than long-term bonds), the ever-present risk of financial repression tools like yield curve control (a monetary policy tool that targets interest rates at specific points of the yield curve) and the fragility of housing and consumer demand (where even modestly higher yields could tip them into deeper weakness) all act as a ceiling. On the other side, yields are also unlikely to decline significantly. Rising fiscal spending (see Chart 1) and persistent government deficits have led to a continuous supply of bonds, while elevated term premia (the extra compensation investors demand for holding a longer-term bond) keep longer maturities resistant to downward movement. Additionally, producer price indices are rising once again, and labour costs remain elevated. Together, these forces explain why yields can swing within a range but are unlikely to break out decisively in either direction.

Chart 1: US spending set to soar

Source: US Congressional Budget Office, Macrobond

Recent statements from the US Federal Reserve (Fed) have reflected a cautiously dovish stance, supportive of easier monetary policy. During the Jackson Hole Economic Symposium in late August, Fed Chair Powell indicated a dovish position in the near term regarding employment, while reaffirming the Fed’s commitment to the 2% inflation target. Market participants interpreted these remarks as a signal for potential rate cuts. In reality, while rate reductions are indeed anticipated as soon as September, unless there is a significant deterioration in labour market data, the inflation threshold will keep the easing path confined.

Calm at the wrong time

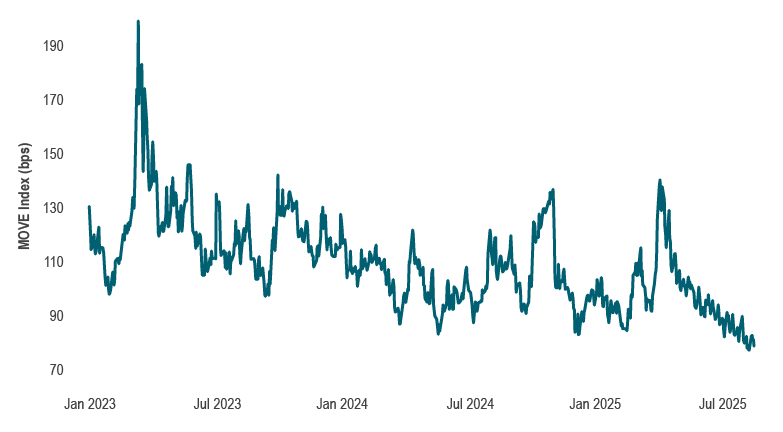

Markets are treating today’s calm as though it was permanent. Yet, underlying pressures tell a different story. Core producer prices are up 3.7% over last year, nearing the upper end of the range since 2022. The wages and salaries component of the employment cost index at 3.6% y/y remains well above its 25-year average. Direct tariff impacts on consumers have so far been muted by businesses working off previous inventory accumulation. Most recently, the independence of the US central bank appears to be under question, which has historically been associated with higher long-term inflation. Meanwhile, the MOVE index, which tracks bond market volatility, sits near cycle lows (see Chart 2), indicating a classic sign of complacency. History shows that moments of calm often precede periods of turbulence. If inflation re-emerges, today’s quiet will prove fragile.

Chart 2: Collapsing bond market volatility since April

Source: ICE BofAML, Macrobond

The great disconnect: payrolls vs. profits

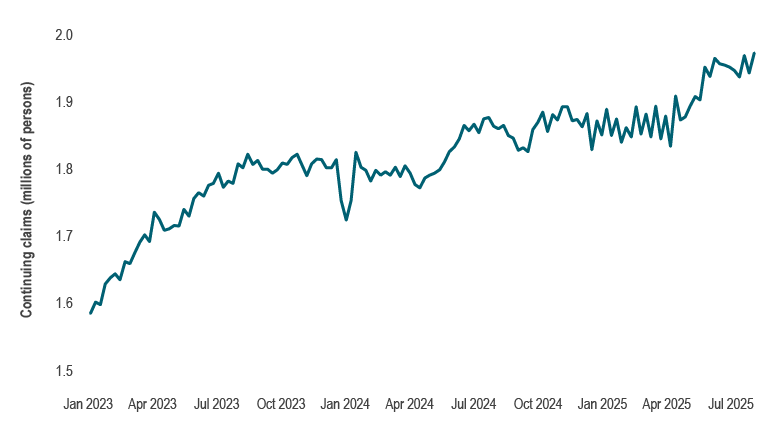

The most striking disconnect is between the labour market and corporate earnings. Employment growth is slowing, with downward revisions a consistent theme. In the US, job growth has slowed dramatically, averaging just 35K per month over May–July, the weakest stretch since the pandemic. Meanwhile, continuing jobless claims are on the rise (see Chart 3). Firms are maintaining a “no hire, no fire” stance, meaning that they are holding onto staff but are reluctant to add new employees. Despite that, corporate America is reporting resilient results. Margins, revenues and earnings in the most recent corporate earnings season have come in stronger than expected. Productivity gains, leaner operations and early adoption of AI may be helping. However, we believe this gap is unsustainable. If the labour market weakens further, demand will eventually soften and profits will be at risk. This question of whether earnings can remain resilient while the jobs picture fades will determine the next leg of market direction.

Chart 3: Rising continuing claims suggest difficulty finding jobs

Source: US Department of Labor, Macrobond

Capital markets

Economic momentum softened through the summer, but equity markets weathered the weak July jobs report and tariff uncertainty well. In August, both the S&P 500 and S&P/TSX Composite reached record highs, with the VIX falling to its lowest level since March. Year to date, US equities are up in the high single-digits, while Canadian, European and emerging markets have posted stronger double-digit gains.

Other asset classes have experienced less favourable performance. WTI crude oil’s June rebound quickly reversed, and crude prices remain negative year to date. The US dollar index maintained stability through the summer but remains negative on a year-to-date basis.

Bond yields continue to stay within established boundaries due to fluctuating market narratives and consistent policies from central banks. Indeed, both the Fed (4.25–4.50%) and the Bank of Canada (2.75%) held policy rates steady during the summer. Canadian corporate spreads tightened to pre-crisis levels in June and July before widening modestly in mid-August alongside a surge in issuance. The FTSE Canada Universe Bond Index is negative thus far in the third quarter and only slightly positive for the year to date.

Portfolio strategy

For investors, the current environment requires a selective approach.

Balanced portfolios have moved back to market weight in equities, reflecting decreased recession probabilities toward the end of the second quarter. Recent data has indicated a gradual economic softening instead of a significant downturn, which has reduced the degree of downside risk. At the same time, equities are being kept afloat by strong earnings. That disconnect still warrants some caution, but the adjustment acknowledges that downside risks are not as acute as earlier in the year. In fundamental equity portfolios, the emphasis is on quality. High-quality businesses with durable earnings growth remain core holdings. As the likelihood of a deep downturn has diminished, exposure to traditional defensive areas of the market has been pared back and selective positions in quality cyclical companies have been added where valuations are attractive.

In fixed income portfolios, the strategy remains cautious. With rates expected to stay range-bound, duration is managed tactically. The shape of the yield curve matters more than the outright level. Short-term rates will be anchored by monetary policy, while longer-term rates will be pressured by fiscal supply, leading to steeper yield curves. In credit, fundamentals are still supportive but credit spreads are too tight to offer much reward, warranting a neutral position.

Connor, Clark & Lunn Private Capital Ltd. (CC&L Private Capital) is pleased to announce that Cameron Smith is joining its leadership team as a Managing Director, Sales Management effective September 2, 2025.

Connor, Clark & Lunn Private Capital Ltd. (CC&L Private Capital) is pleased to announce that Cameron Smith is joining its leadership team as a Managing Director, Sales Management effective September 2, 2025.