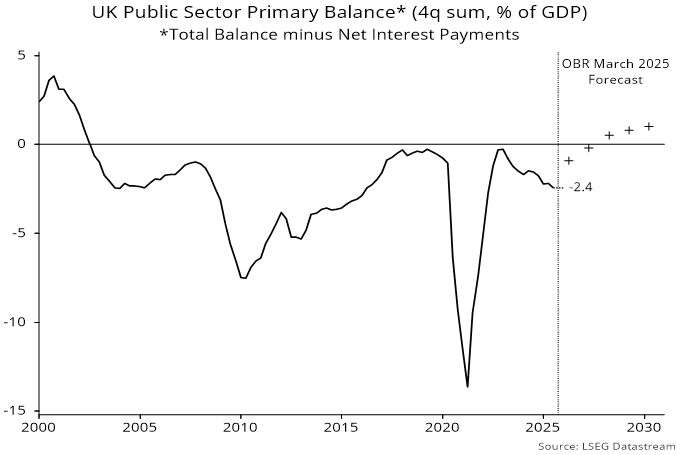

The UK primary fiscal balance is in sizeable deficit, while the effective interest rate on debt is above a trend level of nominal GDP growth consistent with the 2% inflation target. These conditions, if sustained, imply an explosive path for the debt to GDP ratio.

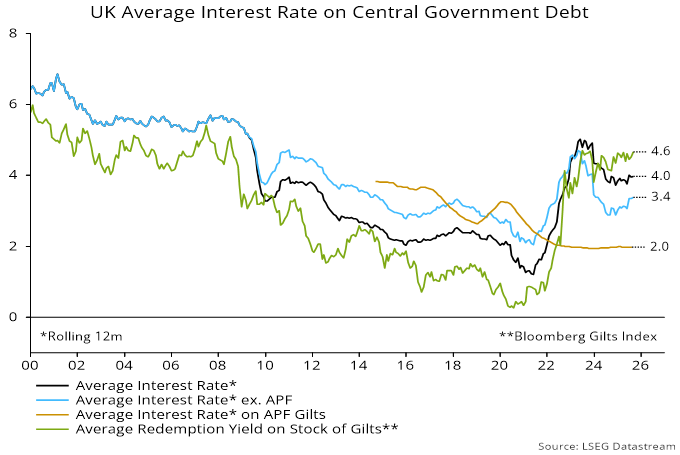

Central government interest payments in the 12 months to August were equivalent to 3.4% of the gross debt stock, according to the latest public finances release.

The Bank of England’s Asset Purchase Facility (APF), however, still owned about a fifth of the debt at the end of the period, so received a significant portion of these payments.

The Bank bought its gilts at much higher prices, so is earning an average interest rate of only 2.0% on the purchase cost of its holdings.

It financed its purchases by creating bank reserves on which it pays Bank rate, currently 4.0%.

Accounting for this carry cost of QE, which the Treasury is obliged to cover, the effective interest rate on government debt over the last 12 months was 4.0%.

This is unexceptional by historical standards but well above an average of 2.7% over 2010-19, when QE was delivering an interest gain – see chart 1.

Chart 1

Achievement of the 2% inflation target over the medium term implies nominal GDP growth of no more than about 3.5% pa, assuming trend economic expansion of about 1.5% pa. An effective interest rate above this level requires the government to run a primary surplus to avoid a trend rise in debt to GDP.

The OBR projected a significant decline in the primary deficit in 2025-26 but the 12-month rolling gap has continued to widen – chart 2. A worse starting position, policy retreats and expected changes to the OBR’s economic assumptions cast strong doubt on the previous forecast of a medium-term return to surplus.

Chart 2

The effective interest rate is subject to conflicting influences and may remain above trend nominal GDP growth. Cuts in Bank rate and QT are reducing the APF net interest loss. On the other hand, the current redemption yield on the stock of gilts, of 4.6%, is well above the interest yield of 3.4% on the stock of debt. Unless the yield curve shifts down, the interest yield will trend higher as existing gilts mature and are refinanced.

The Chancellor’s fiscal rules place emphasis on the current budget but the primary balance is key for stabilising the debt to GDP ratio. Budget measures need to deliver an early return to a primary surplus to calm fears of a fiscal doom loop.