Money Moves Markets

Navigating a coming turn in the stockbuilding cycle

May 23, 2023 by Simon Ward

The stockbuilding cycle is on course to bottom soon and upturns have historically been associated with a procyclical shift in market behaviour. Several considerations, however, argue for caution about positioning for such a shift now.

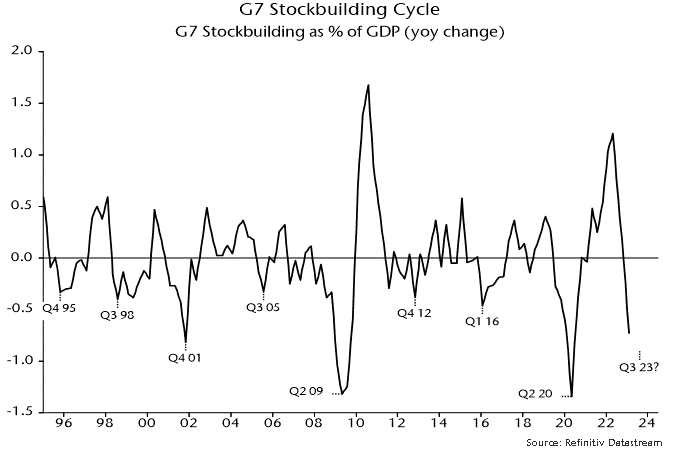

The key indicator used to monitor the cycle here is the annual change in G7 stockbuilding expressed as a percentage of GDP, shown in chart 1. Lows were reached every 3 1/3 years on average, which matches the 40-month periodicity reported by the “discoverer” of the cycle, Joseph Kitchin, in 1923.

Chart 1

The stockbuilding cycle is a key driver of industrial fluctuations: the correlation coefficient of the above series and contemporaneous G7 annual industrial output growth over 1965-2019 was 0.75.

The last cycle low was in Q2 2020 so the next could occur in H2 2023, based on the average cycle length. Partial Q1 information – an estimate is included in chart 1 – indicates that the downswing is well advanced, consistent with the cycle entering a window for a low.

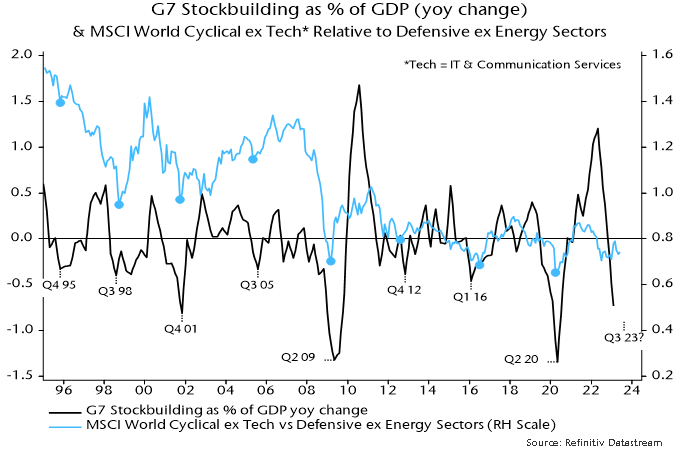

Cycle lows often mark a change in the market environment from risk-off / defensive to risk-on / cyclical, e.g. the price relative of cyclical equity market sectors versus defensive sectors has bottomed around the same time as the cycle historically – chart 2.

Chart 2

So should investors start adding cyclical exposure? There are several reasons for caution.

First, stockbuilding has fallen sharply but only to a “normal” level by historical standards. Further weakness seems likely given the extent of overaccumulation in 2021-23.

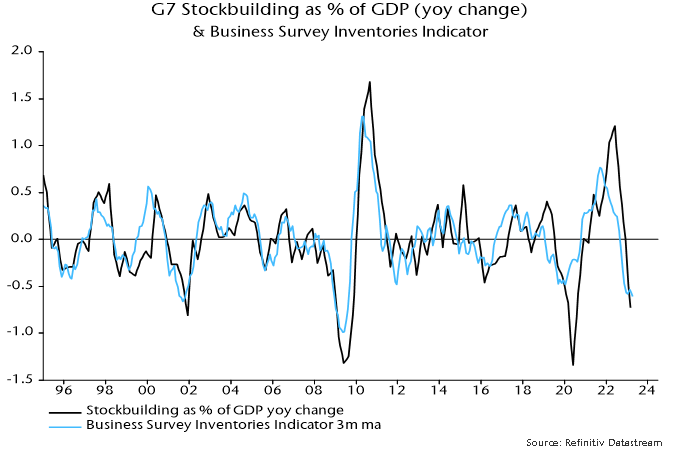

Second, a monthly inventories indicator derived from business surveys, which is more timely and usually leads by several months, has yet to signal a turning point – chart 3.

Chart 3

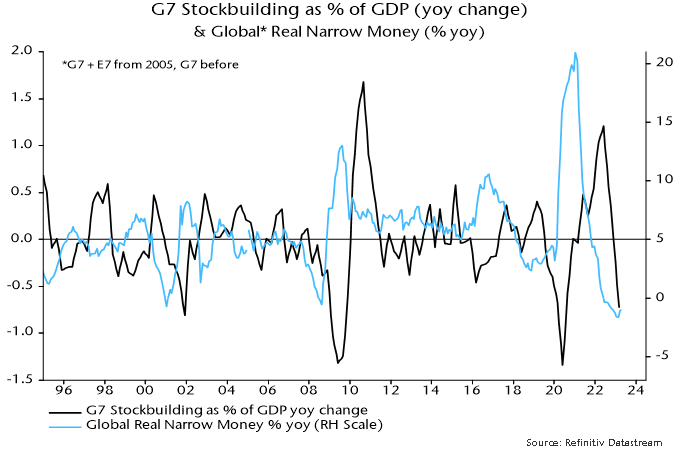

Third, and most importantly, stockbuilding cycle recoveries historically were preceded by a pick-up in real narrow money momentum, which remains very weak – chart 4.

Chart 4

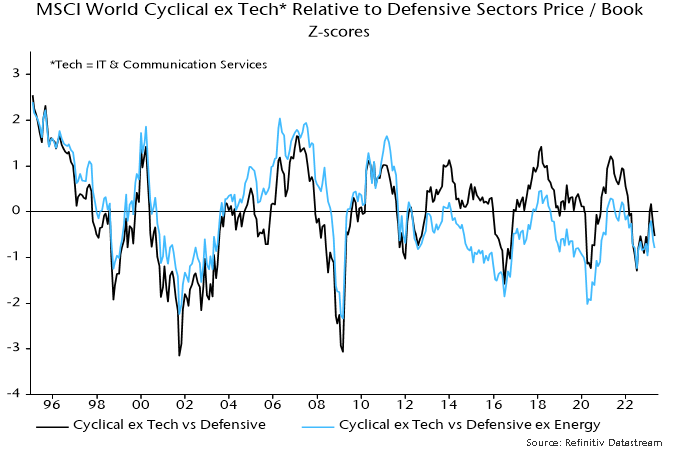

The price to book relative of non-tech cyclical sectors versus defensive sectors is below its long-run average but the divergence is smaller than at most recent stockbuilding cycle lows – chart 5.

Chart 5

There is a risk of another bout of market weakness / cyclical underperformance as the stockbuilding cycle moves into a trough. The judgement here is that a revival in real money momentum is necessary to signal that a cycle low will be followed by a sufficiently solid recovery to boost cyclical assets.