Commentary

China’s fragile recovery: authorities keep options open

May 18, 2023

Summary

- EM equities were weak through April as the global economic backdrop continues to deteriorate.

- Negative global excess money continues to feed a slowdown globally, along with falling inflation.

- The global liquidity backdrop should become less negative as yields peak and industrial output begins to bottom. This should increasingly favour quality growth, tech and defensive (excluding energy) names.

- China’s economy continues to buck the trend, enjoying a modest reopening bounce. However, this recovery may not be enough to offset weakness elsewhere in the world.

- Chinese equities were down through the month and are flat for the year. Leading names in China this year have typically been SOEs boosted by government reform initiatives, banks and some energy names. Our favoured quality growth names have underperformed despite benefiting from the reopening and continue to trade at compelling valuations.

- General elections in Thailand approach, with pro-democratic opposition parties poised to oust the military-linked conservative coalition.

- Turkey is also set to hold presidential and parliamentary elections in May. President Erdogan is likely to face a stiff test from opposition coalition leader Kemal Kilicdaroglu, who has pledged to restore economic orthodoxy to address a deepening economic crisis. Political risk is high, with a return to Erdogan likely to court a currency crisis and add further pressure to the country’s strained banking system.

Mixed signals from China’s reopening

The modest recovery in consumer spending and industrial activity this year has fallen short of investor expectations, with Chinese equities flat for the year. We agree recovery signals have been mixed, which aligns with our previous commentary flagging that authorities in China have been content with a gradual pick up as opposed to the V-shape boom that we saw in the West. Beijing is clearly wary of pouring excessive fiscal and monetary stimulus on the recovery lest it spark an outbreak of inflation.

The government has done little other than offer rhetorical support for business. The Politburo met in late April, with President Xi noting weak economic momentum and subdued demand. Policymakers kept their options open with respect to fiscal and monetary support, pledging a “forceful and effective” approach while reiterating that curbing speculation in property and taming local government debt remained high priorities. Following on from the two sessions last month where new Premier Li Qiang touted the party’s support of business, the Politburo provided another forum to pledge to restore business confidence through the “[elimination of] any legal, regulatory or hidden barriers preventing the fair competition and common development of enterprises of all ownership forms.”

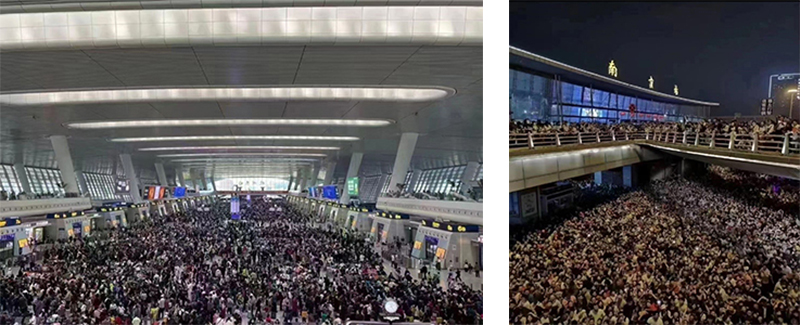

While the policy restraint may frustrate some China bulls, data from China’s Labour Day holiday at the end of April into early May suggests that Chinese consumers are back travelling and dining with a vengeance.

- China Daily reported that on Friday, April 28, the day before the holiday started, train tickets departing Shanghai Hongqiao station to destinations nationwide were sold out.

- Over the first three days of the holiday, approximately 160 million people travelled by air, road or waterway, an increase of over 162% versus the same period in 2022 (China Daily).

- More than 240 million people were estimated to have travelled over the full five-day break, double the pre-COVID level in 2019 (Jefferies).

- Domestic flights during the period are over 4x above 2022 levels (Jefferies).

- Sales growth over the holiday period across catering, apparel, jewellery and tobacco were up 21.4%, 20.9%, 17.4% and 16.8%, respectively, versus 2022 (Jefferies).

NS Partners analyst Michael Zhang is currently travelling in China and sent us some photos of what he calls “revenge travel” over the holiday break.

The trend is positive but fragile – consumers are getting out but overall spending is still relatively weak – and monetary data remains supportive with additional scope for further easing should deflation risk emerge and external headwinds build.

Chile’s president looks to cash in on battery boom through lithium nationalisation

Chile’s government announced that it would seek to capitalise on the global battery boom by nationalising its lithium industry. The stocks of the two main Chilean lithium players, SQM and Albemarle, were hit by the news, with some investors fearing a repeat of the nationalisation of Chilean copper mines in 1971 by the socialist Allende government, where assets were seized from foreign miners without negotiation. The move was a disaster, as foreign engineers and investors left Chile, and just as a global recession in 1973 was about to precipitate a collapse in copper prices. Allende was ultimately ousted in a CIA-backed coup, and replaced by right-wing despot Augusto Pinochet.

This proposal illustrates the importance of factoring political risk and institutional quality into our process. While Boric risks kicking an own goal here, our analysis makes us relatively sanguine about prospects for the Chilean miners SQM and Albemarle, as the president must ultimately pass the law through a centre-right leaning Congress. The legislature is a key check on the ambitions of the president, illustrated by the rejection of a tax reform proposal in March and failure to implement a progressive constitutional reform in a plebiscite last year, with opposition led by right-wing congressional figures.

If the nationalisation plans were to pass through Congress, the government has committed to honouring existing contracts (SQM’s runs to 2030 and Albemarle’s to 2043), while encouraging the miners to negotiate state participation before expiry. It is likely that the miners will engage in and drag out negotiations on state participation as much as possible, while they generate supernormal profits at these elevated lithium prices.

While the market reaction on the news was an overshoot, we were not tempted to add to our exposure. Lithium price strength will ultimately incentivise significant new supply to come online across South America and Australia in the coming years. Additionally, we are happy to maintain an underweight to commodities broadly, based on our outlook that weak global liquidity will feed an economic hard landing that drags on commodities.