Sectoral numbers show that recent US money growth has been focused on the household and financial sectors, with business holdings falling.

A recent post noted that US six-month narrow money momentum fell back in September / October, casting doubt on post-election economic optimism. Sectoral money trends revealed in the Fed’s Q3 financial accounts give further grounds for caution.

Chart 1 compares the six-month rate of change of the monthly broad measure calculated here – M2+, which adds large time deposits at commercial banks and institutional money funds to the official M2 series – with the two-quarter change in a domestic money aggregate derived from the financial accounts. The series are closely correlated with end-Q3 readings similar.

Chart 1

An advantage of the financial accounts data set is that it allows a breakdown of broad / narrow money between the household, non-financial business and financial sectors. Broad money growth in the two quarters to end-Q3 was driven by households and financial firms, with business money falling – chart 2. The narrow money decomposition (not shown) mirrors this pattern.

Chart 2

Business money trends have exhibited a stronger and more consistent relationship with future economic activity than household / financial sector developments historically. Changes in business liquidity can influence decisions about investment and hiring, with employment consequences feeding through to household incomes and money holdings.

The approach here, therefore, is to interpret the signal from a given level of aggregate money growth as more positive – or less negative – when the business component is outperforming (and vice versa).

Chart 3 shows that real business money – on both broad and narrow definitions – is falling on a year-ago basis, suggesting that a slowdown in investment will continue in 2025.

Chart 3

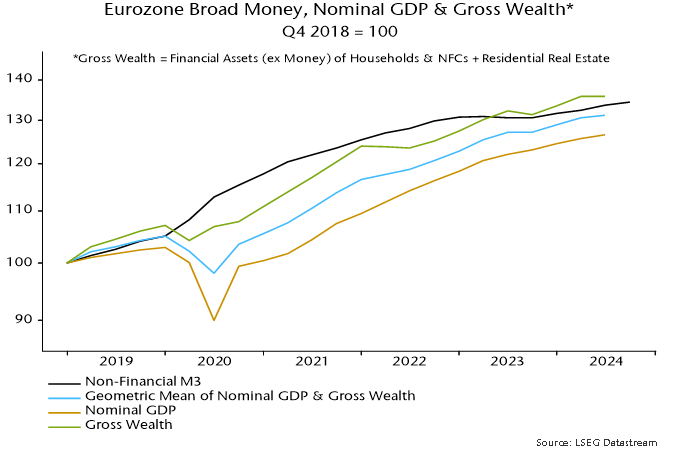

The Q3 financial accounts numbers also support an earlier proposition here that asset prices and nominal GDP have – in combination – moved above levels implied by the current broad money stock, i.e. there is no longer an “excess” money tailwind for the economy and markets.

To recap, the “quantity theory of wealth” is a suggested modification of the traditional quantity theory recognising that (broad) money demand depends on wealth as well as income and proposing equal elasticities. Nominal income is replaced on the right-hand side of the equation of exchange MV = PY by a geometric mean of income and wealth.

Using Q4 2014 as a base, the measure of gross wealth used here – the market value of public equities, debt securities (excluding Fed holdings) and the housing stock – had risen by 107% as of end-Q3 versus a 64% increase in nominal GDP. Implied growth of 84% in the geometric average compares with an increase of 80% in broad money over the same period – chart 4.

Chart 4

Equity / house price gains, debt issuance / QT and expected respectable nominal GDP expansion suggest that the overshoot will have widened in Q4.

Source: Statista 2024

Source: Statista 2024

Le Groupe financier Connor, Clark & Lunn (Groupe financier CC&L) est heureux d’annoncer que Jean-Philippe Lemay se joint à son équipe de direction le 6 janvier 2025.

Le Groupe financier Connor, Clark & Lunn (Groupe financier CC&L) est heureux d’annoncer que Jean-Philippe Lemay se joint à son équipe de direction le 6 janvier 2025.