Commentaires

Flows before pros?

10 novembre 2025

Considering the importance of structural liquidity in emerging market investing

We argue that a narrow focus on company fundamentals leaves investors increasingly exposed to powerful external forces like structural and cyclical liquidity shifts.

These forces influence capital availability, investor behaviour and asset pricing, often overriding fundamentals in the short to medium term.

Below, we run through two EM-specific examples of how we think about structural liquidity, along with a brief comment on market structure globally.

China’s National Team steps in as foreign investors hit eject

The “China is un-investable” doldrums from early 2021 to the beginning of 2024 saw the MSCI China Index drop from a peak to trough by over 50% in USD terms. Haphazard regulatory clampdowns on the technology and education sectors, a collapsing property market, and Sino-US tensions saw foreign investors run for the exits.

At the peak of the revulsion, we saw many liquid and high-quality companies being dumped, seemingly irrespective of fundamentals. For us, this was a painful experience with many of our favourite names caught up in the stampede. It was also a valuable lesson about the impact of what we call structural liquidity in markets and its power to create extended and sharp periods of disequilibrium where prices appear completely detached from fundamentals.

In our process, we define structural liquidity as the long-term, underlying availability of capital within a financial system or market. Unlike short-term liquidity (which can fluctuate daily), structural liquidity is shaped by:

- The depth and breadth of financial institutions

- The regulatory environment

- The savings rate and capital formation

- The presence of long-term investors (e.g., pension funds, sovereign wealth funds and other state-linked allocators)

- Factors outside of a given country – i.e. pressures on foreign allocators to shift exposure

Our clients are very familiar with our work analysing monetary cycles, with the aim of anticipating economic and market environments over the next year or so. This is a powerful tool for understanding the prevailing investment backdrop and how we expect it to evolve.

Structural liquidity gets less coverage, but understanding this factor can be just as impactful for performance, especially at extremes. Analysing the evolving composition of a country’s financial markets can provide insights into how changes in liquidity flows may be felt across asset classes.

Through the China doldrums, structural liquidity was working against us. Foreign investors were more heavily weighted to higher-quality companies, aligned with our stock picking bias. As these investors yanked funds from the market, we saw favoured names get cut down regardless of the fact that many of these business were fundamentally well positioned to weather China’s weak economy and geopolitical turbulence.

At the same time, state allocators in China (the “National Team”) were instructed to support the market. The reflex for these institutions was to buy ETFs loaded up with state owned enterprises (SOEs). This created an odd dynamic where more economically sensitive, highly indebted and relatively poorly governed companies (including distressed banks and property companies) were dramatically outperforming quality companies in an economic slump.

Investor flows and their composition had a huge impact on returns through much of the 2022–2024 period. In hindsight, the optimal strategy to navigate the volatility would have been to reduce the risk budget for “foreign favourites” while increasing the weighting to select SOEs which fit our stock picking framework. Unfortunately, we were slow to pick up the trend and by the time we had a firm grasp of the situation, valuations of our favourite businesses were starting to look incredibly cheap while already robust fundamentals appeared to be strengthening.

We reviewed China exposure in depth and exited a few positions that were exposed to persistently weak consumer sentiment. We also travelled in China extensively to meet with dozens of companies as soon as the country reopened from the pandemic. This helped to accelerate idea generation and generate more competition for capital within our China exposure. The rest was behavioural, with our iterative process of testing and re-testing stock theses and country views underpinning our conviction to stick with a number of out-of-favour companies.

The slump in quality stocks came to an end as Chinese authorities announced monetary and fiscal loosening in September 2024 to stimulate the economy. This was followed by the Deepseek shock in January 2025, which shone a light on Chinese innovation in AI which was progressing rapidly and at a fraction of the cost in the United States. Suddenly, domestic allocators were rushing into Chinese consumer tech stocks leading China’s AI development. Improving liquidity supported a broadening out of the rally, boosting other innovative companies such as battery leader CATL, drug development company Wuxi Biologics and Hong Kong financials such as Futu Holdings.

Structural liquidity is playing an important role in providing fuel for the rally. With China’s weak housing markets and longer-term bond yields recently moving up from record lows, equities have been the default beneficiary of improving monetary trends which has fuelled a liquidity-driven bull market this year.

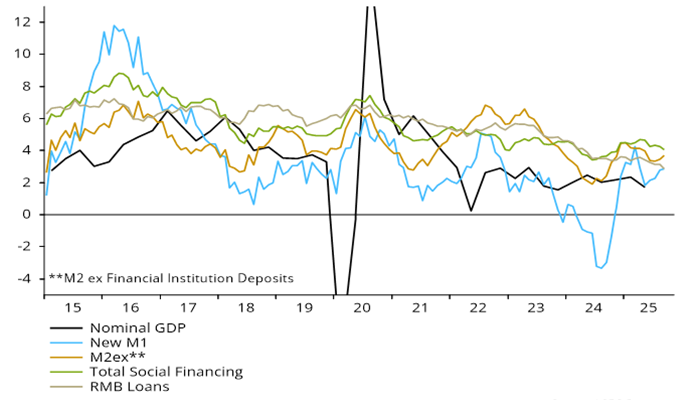

China nominal GDP* (% 2q) & money / social financing* (% 6m)

*Own seasonal adjustment

Source: NS Partners and LSEG.

So far it has been domestic money within China participating in the rally, with foreign investors yet to return. Global investors will likely want to see Sino-US tensions cool further following the October APEC summit between Trump and Xi where a temporary truce was announced.

China equities flows: domestic vs. foreign investors

Source: EPFR

While it is pleasing to see our investment style come back into favour, we aren’t falling in love with this rally. Any downturn in liquidity would be a signal to reduce exposure. In addition, while our companies have broadly reported well, much of the wider rally this year has come from re-rating.

Source: Jeffries, October 2025

We are wary of chasing momentum in the China AI thematic without support from fundamentals. This is a fragile trade and vulnerable to a stall in money growth in our view.

Beware relying on mean reversion tables in India

India offers a different perspective on the importance of structural liquidity. Indian equities outperformed for years leading into 2025, and yet most EM investors were underweight the market citing rich valuations.

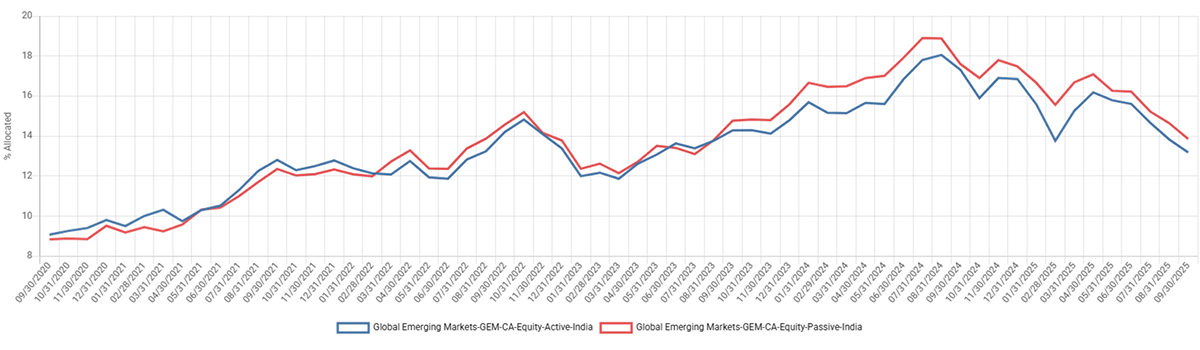

GEMs active vs. passive country allocations

Source: EPFR

While we were certainly mindful of India’s valuation premium to wider EM, the rise of domestic mutual funds driving flows into equities as Indian workers contribute to their pension accounts is a major structural change. We have seen this before in places like Chile or Australia, and once this trend picks up steam it can be dangerous to rely too heavily on your mean reversion tables!

While we did shift to an underweight in India at the end of 2024, the move was modest and largely based on a view that a deluge of IPOs coming to market was soaking up too much liquidity. This factor, combined with high valuations, supported our view that the market looked to be due a period of consolidation after several years of strong gains.

Model GEM portfolio: India strategy macro ratings and weightings

| India | Rating | Exposure | Share of risk | Relative weight |

|---|---|---|---|---|

| October 2025 | 3 | 13% | 16.9% | -2.5% |

| June 2025 | 3 | 17% | 22% | -1.1% |

| December 2024 | 4 | 19% | 20% | -0.5% |

| June 2024 | 3 | 21% | 30% | +1.9% |

| December 2023 | 2 | 19% | 19.7% | +2.6% |

| June 2023 | 1 | 17% | 14.4% | +2.2% |

Source: NS Partners

More recently however, agressive central bank rate cuts have fuelled a pick-up in cyclical liquidity, and while it is a near-term headwind, the flurry of IPOs will deepen the market and produce a more vibrant opportunity set. At the company level, earnings growth is set to lead EM for the next few years. While we are happy to wait for the market to come back to us for now, we see no reason to dismantle our India exposure with such a strong structural backdrop and will be ready to add back when the opportunity arises.

Passive dominance and market fragility

Thinking more broadly, we have been reading some eye-opening analysis from market strategist and investor Michael Green on the impact of rising passive dominance in markets. I won’t rehash the whole thesis in detail, but in a nutshell, Green argues that passive investing has fundamentally reshaped market dynamics by inflating valuations of the largest stocks and undermining traditional price discovery.

As index funds allocate capital based on market cap rather than fundamentals, they create a self-reinforcing cycle where rising prices attract more flows, further distorting valuations. This mechanism favours size and trend over intrinsic value and ignores quality companies outside major indices.

Markets become increasingly inelastic as passive share grows and the share of active and valuation-driven investment falls. The outcome is that liquidity no longer scales with market cap. This makes large stocks more vulnerable to outsized price impacts from passive flows.

Therefore, the largest beneficiaries of a constant inflows to passive vehicles could suffer sharp reversals should those flows reverse, exposing the market to volatility and mispricing.

Finally, Green highlights what he sees as an absurdity, being the construction of rigid rule-based investment strategies meant to operate in markets, which are complex adaptive systems. The dominance of this approach to investment is distorting markets and capital allocation which will have negative real-world impacts in magnifying the power of megacap firms and stifling innovation and creative destruction.

Having always considered the impact of structural liquidity in our markets as a part of our process, Green’s work resonates with our team. In our view, it will be crucial going forward for active investors to have an awareness of how rising passive dominance will create distortions in markets and identify the risks and opportunities that will flow from them.