L’argent, le moteur des marchés

Chinese money update: lacklustre outlook

14 novembre 2025 par Simon Ward

Chinese October money / credit numbers were mixed, suggesting a continuation of sluggish economic growth.

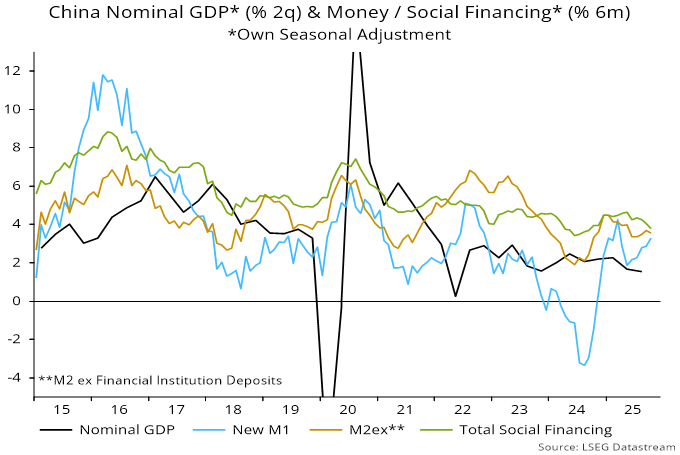

On the positive side, six-month growth of narrow money M1 extended its recent recovery, reaching its highest since March – see chart 1. (A fall in the year-on-year measure reflected an unfavourable base effect.)

Chart 1

Broad credit slowed further, however, while growth of broad money – on the preferred definition here excluding deposits of financial institutions – fell back.

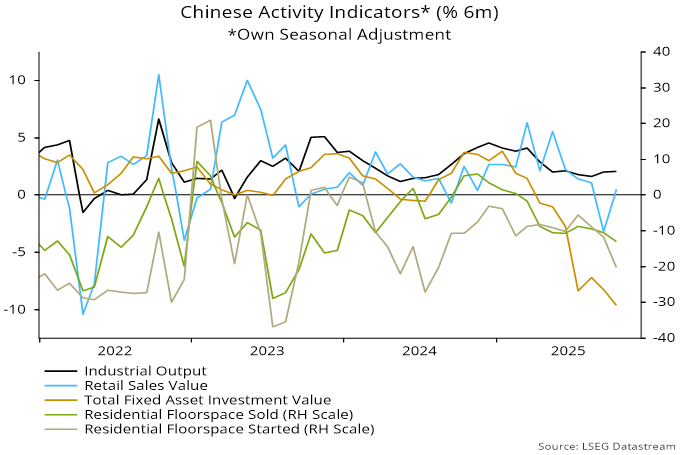

Concern about downside economic risks is supported by October activity numbers, showing faster rates of contraction of fixed asset investment and housing sales / starts – chart 2.

Chart 2

The weakness of the fixed asset investment data is difficult to square with Q3 GDP results showing an investment contribution of 0.9 pp to annual growth of 4.8%. The national accounts number includes stockbuilding but there is no indication from other evidence – admittedly limited – of a rapid build-up of inventories.

Industrial output growth continues to hold up while retail sales recovered after September weakness.

The authorities announced modest additional stimulus measures in September / October – new investment financing and an increase in local government bond issuance, each of RMB500 bn – and probably need to see greater weakness in the data before considering further action.

A positive gap between money growth and nominal GDP expansion may continue to offer support to equities, given low bond yields and still-negative property trends.

From a global perspective, lacklustre Chinese news presents no challenge to the forecast here of a loss of industrial momentum into early 2026 – see previous post.